Major Surge Prepared?! Over 3 Million Tons Of Ethylene Glycol Facilities To Halt Production!

According to market reports, two ethylene glycol units in Iran with a combined annual production capacity of 3.3 million tons have been shut down, and the restart time for these units has not yet been determined.

In addition, Iran has plans to shut down four ethylene glycol units with a combined annual production capacity of 7.25 million tons in late November or early December. However, the subsequent implementation remains to be seen.

Industry insiders indicate that the production halt is primarily due to the implementation of Iran's gas restriction policy. Currently, there is a shortage of natural gas supply within Iran, and natural gas is a critical energy source for ethylene glycol production. The insufficient energy supply has forced the shutdown of two units, each with a production capacity of 1.65 million tons. One of these units is also experiencing technical issues.

In the market, the 3.3 million tons of ethylene glycol represents about 8% of the global annual production. Currently, downstream demand remains stable, and the emergence of a supply gap will alleviate market inventory pressure, providing significant benefits to spot prices and pushing them higher in the short term.

In the futures market, although the main contract for ethylene glycol 2601 had been on a downward trend, the recent supply disruption is likely to reverse market sentiment and support a rebound in futures prices. Additionally, the uncertainty regarding the restart time of production facilities may further increase price premiums.

Impact on the domestic market

Iran's production halt may lead to a contraction in the supply of imports to the Chinese market, and inventories may continue to decline.

Nearly half of Iran's ethylene glycol production is exported to China, with an average monthly supply of about 80,000 to 100,000 tons, accounting for 10% to 15% of China's ethylene glycol imports.

The shutdown of these two main production units will directly reduce China's ethylene glycol import sources. Currently, domestic ethylene glycol port inventories are at a low level, and the contraction in imports is likely to further decrease inventories, making the supply-side tension increasingly apparent in the short term.

On one hand, the price level has gained support and rebounded, leading to a reversal in futures sentiment. The emergence of a supply gap will significantly benefit domestic ethylene glycol spot prices, reversing the previous weak trend.

In the futures market, the previous main contract for ethylene glycol 2601 was in a downward trend. This shutdown event may reverse market sentiment and help the futures price rebound. Additionally, the uncertainty of the restart time for the facility could further create premium space for prices.

On the other hand, the impact of the industrial chain will affect upstream and downstream enterprises.

For downstream industries, the domestic polyester industry is the main consumer of ethylene glycol. If prices rise, it will increase the raw material procurement costs for polyester companies, and some small and medium-sized polyester companies may adjust their production plans to control costs.

In addition, for domestic coal-based and oil-based ethylene glycol enterprises, cost support is strengthening, and the profits of coal-based ethylene glycol are expected to expand. However, due to the limitations of operating conditions, it is difficult to quickly increase production capacity to fill the import gap. Meanwhile, some methanol facilities in Iran have also halted operations due to gas supply restrictions, which may disrupt the raw material supply for domestic MTO ethylene glycol production and potentially further reduce the domestic ethylene glycol supply.

Analysis of Ethylene Glycol Imports

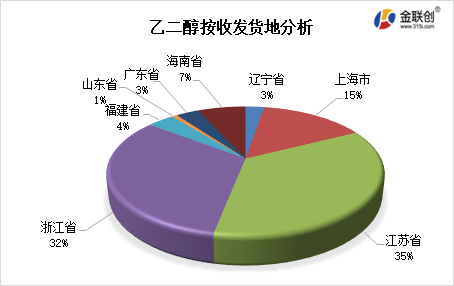

According to the latest customs statistics, in October, the main provinces for ethylene glycol imports in China were still Jiangsu and Zhejiang, with Jiangsu Province importing 230.5 thousand tons, accounting for 35%, and Zhejiang Province importing 209.7 thousand tons, accounting for 32%. Polyester operating rates in October hovered around 88.65%, up 1.45% from the average operating rate of the previous month. Jiangsu, as a major province for polyester production capacity, houses several large-scale polyester facilities, while Zhejiang relies on industrial bases such as Ningbo and Shaoxing, maintaining strong demand for ethylene glycol. Throughout the month, polyester operations continued to maintain high levels, particularly in bottle-grade PET, where Zhuhai Huarun's 1.1 million tons/year bottle-grade PET unit restarted after the typhoon at the end of September, boosting overall operating rates in October. Fiber-grade PET saw some companies increase their operating loads due to the necessity of autumn and winter orders. Polyester filament yarn operations were generally at high levels during the month, driven by the commissioning of Tongkun Fujian Henghai, the resumption of Fujian Jingwei, and load increases at Tongkun Anhui Youshun, Jiangsu Shenjiu, and Wuxi Huaya. However, within the entire industry chain, only polyester staple fiber operations declined, with Fujian Shanli's 200 thousand tons unit undergoing maintenance and resuming operation at the end of October.

Data source: Customs

In October, the import price of ethylene glycol fluctuated slightly. In the short term, high operating rates in the downstream polyester industry may continue to support the demand for ethylene glycol. Special attention should be paid to the release of new bottle-grade PET capacities and the marginal increase from the commissioning of new filament facilities. However, the supply side is highly dependent on a few regions such as Saudi Arabia, and there remain uncertainties.

The recent changes in foreign ethylene glycol plants have led to a contraction in import volumes, resulting in an anticipated increase in ethylene glycol prices.

Source: JLC, WELINK Chemical, etc.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Breakthrough! 13.6-million-ton new giant emerges as world’s fourth-largest polyolefin producer, reshaping industry landscape

-

Massive Loss of $960 Million! Wansheng Co., Ltd. Sees Rising Revenue But Declining Profits—Why Did the Phosphorus-Based Flame Retardant Leader Falter?

-

BASF's $8.7 Billion Zhanjiang Site Fully Operational, Covestro, SABIC, Arkema and Other Plastics Giants Double Down on China

-

Domestic PBE Breakthrough, Polyolefin Modification Industry to Break the Impasse

-

Deadly Impact: Hormuz Strait Blockade Sparks Shortage of Plastic Raw Materials, Threatening Shutdowns at Japanese and Korean Chemical Plants