Deadly Impact: Hormuz Strait Blockade Sparks Shortage of Plastic Raw Materials, Threatening Shutdowns at Japanese and Korean Chemical Plants

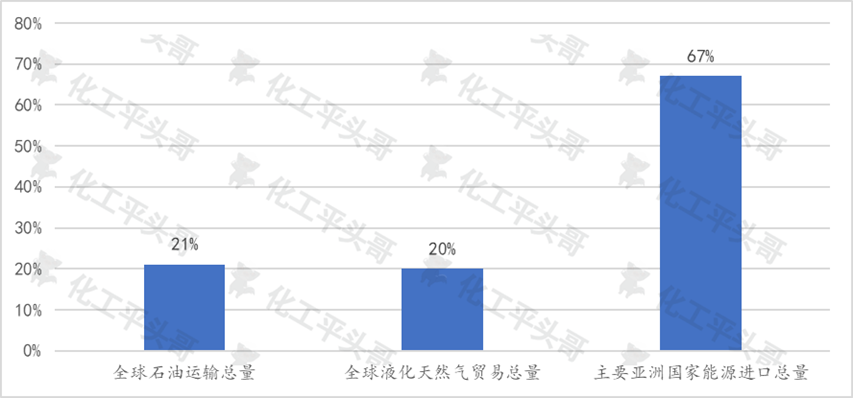

According to Wind data, as the "throat" of global energy transportation, the Strait of Hormuz handles about one-fifth of the world's crude oil trade, and its accessibility directly affects the stability of the global energy and manufacturing supply chains.

The image shows the Strait of Hormuz.

As the U.S.-Israel-Iran conflict continues to escalate, Iran’s closure of the Strait has not only exacerbated a global crude oil supply shortage but also triggered comprehensive, profound ripple effects across the plastics and chemical industry—impacting raw material supply, production capacity utilization, price volatility, and industrial structure realignment—posing an unprecedented challenge to the global plastics and chemical industry.

The share of global total oil and gas products passing through the Strait of Hormuz

Image source: Chemical Industry Pingtouge Data source: Wind

Critical Raw Material Shortage: Naphtha Shortage Directly Hits the Foundation of the Plastics Industry

The core raw material chain of the plasticization industry highly depends on refined products from crude oil. Among these, naphtha serves as the main raw material for key chemical intermediates such as ethylene and propylene, acting as a critical link connecting crude oil to plastic products. Ethylene, through polymerization reactions, can produce fundamental plastics such as polyethylene (PE) and polyvinyl chloride (PVC), which are core outputs of the plasticization industry, widely used in packaging, construction materials, automotive and other end-user sectors. The recent blockade of the Strait of Hormuz has directly cut off the global major naphtha supply routes, with the most direct impact on the plasticization industries in Japan and South Korea.

Wind data shows that about 80% of oil tankers from Japan and South Korea must pass through the Strait of Hormuz, with over 95% of Japan's Middle Eastern crude oil and more than 70% of South Korea's imported crude oil relying on this route. Due to the high dependence of the Japanese and South Korean petrochemical industries on naphtha refined from Middle Eastern crude oil, the blockade of the strait directly leads to a tight supply of naphtha for both countries.

A large number of ships are trapped in the Strait of Hormuz. Photo credit: AFP

Among these, Japan’s naphtha stockpile is sufficient for only about 20 days—far below its 250-day crude oil reserve—making the risk of raw material shortages imminent.

According to a Nikkei Asia report on March 7, Japanese major petrochemical company Idemitsu Kosan has warned its partners that it may be forced to suspend ethylene production if the Strait of Hormuz remains blocked. The company's plants in Tokuyama, Yamaguchi Prefecture (with an annual capacity of 620,000 tons) and Chiba, Chiba Prefecture (with an annual capacity of 370,000 tons) may be the first to halt operations. The combined capacity of these two plants accounts for about 16% of Japan's total ethylene production.

The scene of the Idemitsu Kosan factory located in Chiba Prefecture. Image source: Nikkei Asia

Maruzen Petrochemical, a subsidiary of Japan's Cosmo Energy Holdings, has facilities in Chiba Prefecture. A company representative said, "We do not expect production to be affected until March, and we are looking into ways to ensure a stable supply."

Data from the Japan Petrochemical Industry Association shows that there are currently 12 ethylene production plants in Japan, with a total annual capacity of about 6.16 million tons. If the supply continues to be tight, more companies will be forced to reduce or even halt production, leading to a contraction in the capacity of downstream plastic raw materials such as PE and PVC.

South Korea's petrochemical industry is also facing severe challenges, with major petrochemical companies such as LG Chem and Lotte Chemical already reporting losses, primarily due to soaring production costs caused by naphtha supply shortages. Additionally, Japanese refineries, long optimized for Middle Eastern crude oil, find it difficult to switch crude sources in the short term, further exacerbating naphtha supply tightness and forcing the petrochemical industries in both Japan and South Korea into a cycle of capacity contraction.

Severe price fluctuations: Continuous transmission of cost pressures in the plasticization industry chain

The blockade of the Strait of Hormuz has triggered a surge in crude oil prices, which has continuously propagated through the raw material supply chain to the entire plastics and chemical industry, causing sharp fluctuations in global plastics and chemical product prices and continuously squeezing corporate profit margins. According to a research report by China International Capital Corporation (CICC), if trade through the Strait of Hormuz remains disrupted until the second quarter of 2026, the Brent crude oil price benchmark could rise to over USD 120 per barrel. The sharp increase in crude oil prices directly drives up prices of key raw materials such as naphtha and ethylene.

In the Japanese and Korean markets, the prices of plastic-related products have fluctuated significantly. Japanese companies such as Resonac and Mitsubishi Gas Chemical have increased the prices of CCL and other chemical products by over 30%, while the prices of air separation gases and others have risen by more than 10%; in Korea, due to soaring costs and pressure on demand, the price spread of major chemical products like ethylene has fallen below the break-even point, exacerbating losses for companies, and the prices of plastic-related products such as TDI have risen in tandem with plant maintenance.

The Chinese plasticizer industry has also been affected. Although the self-sufficiency rate of major chemical products in China has rapidly increased in recent years, and emergency strategies are relatively adequate, as an important participant in the global plasticizer industry, it is still difficult to completely avoid the transmission effects from international markets.

Data shows that China's methanol imports rely on the Middle East for 30%-35%, and methanol is an essential auxiliary raw material in the plasticizer industry. Meanwhile, over 50% of sulfur imports for phosphorus fertilizer production come from the Middle East (56.20% in 2025). Due to the strait blockade, the prices of these raw materials have surged, compressing the profit margins of domestic refining companies. The costs of downstream industries such as plastics and synthetic fibers have also risen, with small and medium-sized plastic and chemical enterprises facing significant pressure.

In addition, the surge in shipping costs has further intensified the price pressure on plastic products. According to the Economic Daily, to avoid risks, global shipping giants such as Hapag-Lloyd, CMA CGM, and Maersk have completely suspended the passage of ships through the Strait of Hormuz. Some ships have been forced to reroute via the Cape of Good Hope, increasing the voyage by 40%, with a significant rise in freight and war risk insurance premiums. This has further increased the import and export costs of plastic raw materials and finished products, amplifying the price volatility.

Industry Restructuring: The Plastics Industry Faces Adjustments and Opportunities

The blockade of the Strait of Hormuz not only brings short-term shortages of raw materials and price fluctuations, but also drives a profound restructuring of the global plastic industry. For Japan and South Korea's plastic industries, the long-term reliance on Middle Eastern raw materials has faced severe challenges, forcing the industry to accelerate its transformation.

According to the industry analysis by Touda, the Japanese chemical industry may strengthen its monopoly in key areas such as semiconductor materials, while increasing imports of oil from Australia and Russia, reducing reliance on the Middle East. The South Korean chemical industry will be forced to cut back on large-scale plastic raw material production capacity, shifting toward high-end sectors such as high-performance polymers and battery materials, while promoting the adaptation of refining facilities to non-Middle Eastern crude oil to alleviate raw material challenges.

This transformation will directly impact the global plastics industry's competitive landscape, creating new development opportunities for China's plastics sector.

In the long term, China, taking advantage of its diversified raw material imports, can fill the gap left by the capacity reduction of major plastic raw materials in Japan and South Korea, expand the plastic market share in Asia, and alleviate the competitive pressure on traditional plastic products domestically.

Meanwhile, the export restrictions on high-end plastic materials from Japan and South Korea will drive the acceleration of domestic substitution of photoresists and high-end polyimides in China, promoting the upgrading of China's plastic industry toward high-end sectors.

It is worth noting that China's plasticizing industry also needs to address potential risks. According to the 21st Century Business Herald, China's methanol imports in 2025 will amount to 14.4054 million tons, with 69.9% of the methanol coming from the Middle East. Although the methanol directly imported from Iran only accounts for 5.7%, disruptions in the overall supply from the Middle East would still have a significant impact on the domestic methanol market.

Moreover, domestic plastic and chemical enterprises still need to closely address the inflationary transmission pressure caused by rising oil prices and the risks of global supply chain volatility.

Emergency Response and Long-term Insights: The Plastics Industry Needs to Strengthen Supply Chain Security Defenses

Faced with the crisis of the Strait of Hormuz being blocked, global plasticization-related companies have started to take emergency measures.

Japan's Mitsubishi Chemical is evaluating how long its naphtha inventory will last and considering purchasing raw materials from other regions; Cosmo Energy Holdings' Maruzen Petrochemical is seeking a stable supply solution.

Meanwhile, Indonesia's largest chemical company, Chandra Asri Pacific, and Singapore-based ethylene producer PCS have declared force majeure to avoid liability for breach of contract due to supply disruptions.

This crisis has also sounded the alarm for the global plastic industry: the vulnerability of the supply chain is far greater than imagined, and over-reliance on a single raw material source and a single shipping route makes it extremely susceptible to the impact of geopolitical conflicts.

For Chinese plasticization companies, on one hand, they need to further optimize the structure of raw material imports, expand diversified import channels, and reduce reliance on Middle Eastern raw materials; on the other hand, they should increase R&D investment, enhance the independent production capacity of high-end plastic materials, accelerate the process of domestic substitution, and reduce reliance on imported high-end products.

The narrow Strait of Hormuz is rattling the global petrochemical industry. From naphtha shortages causing production cutbacks and price volatility exerting cost pressures, to profound restructuring of industry dynamics, this chain reaction triggered by geopolitical conflict is subjecting the global petrochemical sector to an unprecedented test.

For China's plastics industry, this presents both a challenge and an opportunity—only by strengthening supply chain security and accelerating industrial transformation and upgrading can it gain the upper hand in the shifting global industrial landscape and achieve high-quality development. The global plastics industry must also seize this opportunity to reconstruct a more resilient and diversified supply chain system to address potential risks and challenges in the future.

Source: Translate the above content into English, output the translation directly, without any explanation.Nikkei Asia, AFPWind, olefins and high-end downstream sectors, Chemical Pingtouge, and other publicly available online sources.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

A Look at the Material Suppliers Behind SpaceX

-

Government's Triple Action, Enterprises' Three Arrows in Five Days, Semiconductor Reshuffle! What Signal Does Japan's Chemical Industry Release?

-

Fire breaks out at jiangsu meiside!

-

Name change without tax change: POM Anti-Dumping Duty Rate Inheritance Implemented

-

Ethylene: Production Capacity Accelerates Expansion, Global Industry Landscape Is Being Reshaped