Plastic Product Exports Decrease, Polyolefins Remain Weak

Introduction:In October 2025, international oil prices fell, leading to a simultaneous decline in polyolefin prices, which closed the domestic import arbitrage window and reduced raw material imports. The export growth rate of plastic products remained low, with a noticeable decrease in exports to the United States due to tariff policies. In November, prices are expected to continue fluctuating at the bottom, influenced by the pressure of strong supply and weak demand.

According to customs statistics, in October 2025, the total value of China's imports and exports was USD 520.63 billion, representing a month-on-month decrease of 8.1% and a year-on-year decrease of 0.3%. Specifically, exports amounted to USD 305.35 billion, down 1.1% year-on-year and 7.0% month-on-month; imports were USD 215.28 billion, up 1% year-on-year but down 9.5% month-on-month, resulting in a trade surplus of USD 90.07 billion, compared to the previous value of USD 90.45 billion. The export growth rate for the first ten months of 2025 was 5.3%. In 2024, the annual export growth rate was 5.9%, with an import growth rate of 1.1% and a trade surplus of USD 992.16 billion. In October, the growth rates of both imports and exports in China showed a significant slowdown. On the export side, besides the high base effect and fewer working days, the continued negative growth in exports to the United States and the slowdown in the growth rate of exports to Africa from a high level were also significant drag factors. On the import side, the decline was mainly driven by quantity factors, compounded by weak domestic production and consumption demand, with substantial decreases in the imports of key commodities such as steel, unwrought copper and copper products, and mechanical and electrical products. Looking ahead within the year, as Sino-US trade frictions marginally ease and the global manufacturing climate picks up, exports are expected to stabilize and rebound; however, the high base effect and price factors will continue to constrain the annual export growth rate to some extent.

In terms of polyolefin-related products, in October 2025, the import volume of primary shaped plastic raw materials decreased along with a drop in prices. The export value of plastic products decreased year-on-year. In October, international oil prices fell, and polyolefin prices declined accordingly. The domestic import arbitrage window closed, leading to a reduction in raw material imports. The export of plastic products maintained a low growth rate, with a significant decrease in exports to the United States due to the impact of U.S. tariff policies. In November, the situation is expected to remain under pressure from strong supply and weak demand, with prices continuing to fluctuate at low levels.

The cumulative year-on-year growth rate of China's exports to the United States continues to decline.

Data Source: General Administration of Customs of China, Jinlianchuang

In terms of U.S. dollars, the total value of China's exports still maintained a year-on-year positive growth rate. However, the total value of exports to the United States managed to maintain positive growth in the first three months, decreased year-on-year from April to June, and the rate of decline continued to expand thereafter. This indicates that Trump's tariff policy has indeed had a real impact on China's exports to the United States. In the first ten months, the total value of China's exports increased by 5.3% year-on-year, while the total value of exports to the United States decreased by 17.1% year-on-year, with the decline continuing to widen. The impact of U.S. tariff policy is significant.

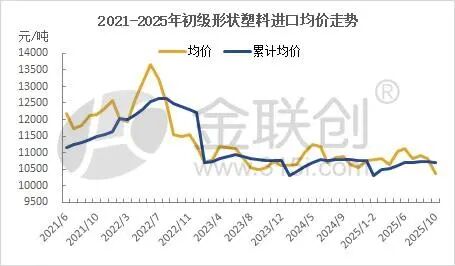

Imports of primary-shaped plastics decrease in volume and price.

Data source: General Administration of Customs of China, JLC Network Technology.

In October 2025, the import quantity of primary shape plastic raw materials was 2.05 million tons, an increase of 14.7% compared to the same period last year; the import value was 21.27 billion yuan, a decrease of 16.8% year-on-year. From January to October 2025, the import quantity of primary shape plastic raw materials was 22.12 million tons, a decrease of 7.6% year-on-year; the import value was 236.83 billion yuan, a decrease of 8.2%. From January to December 2024, the import quantity of primary shape plastic raw materials was 28.981 million tons, a decrease of 2.1% compared to the same period in 2023; the import value was 311.67 billion yuan, a decrease of 2.0%. From a cost-support perspective, international crude oil prices have been on a downward trend since mid-January, leading to a simultaneous drop in domestic polyolefin prices. Consequently, the domestic import arbitrage window has closed, resulting in reduced import of raw materials. In October and November, international oil prices continued to decline, and the international PE costs continued to decrease. By November, the PE linear import arbitrage window had opened, while the PP import arbitrage window remained closed.

Data Source: General Administration of Customs of China, JLC Network Technology Co., Ltd.

From the perspective of the monthly average price of imported primary-shaped plastic raw materials, after reaching a new high in June 2022, the monthly average price began to decline, maintaining a continuous downward trend thereafter. As shown in the figure, the cumulative average price from January to December 2023 continued to decline. In 2024, prices generally maintained a fluctuating downward trend with slight amplitude. In the first two months of 2025, the cumulative average price significantly declined due to the continuous drop in international crude oil prices. The average price slightly increased in March, declined again in April, improved in May, continued to rise in June, and showed a notable decrease in July. In August, the average price slightly increased, declined again in September, and accelerated downward in October. It is expected that the average price will continue to decline in November.

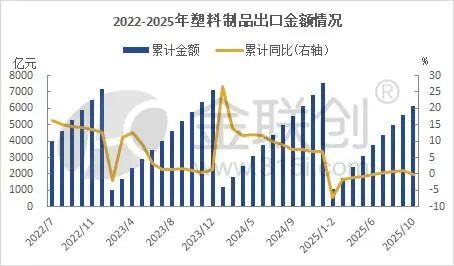

The export value of plastic products decreased year-on-year.

Data Source: General Administration of Customs of China, JLC.

In October 2025, the export value of plastic products was 55.04 billion yuan, a year-on-year decrease of 9.5%. From January to October 2025, the export value of plastic products was 614.55 billion yuan, a year-on-year decrease of 0.9%. In U.S. dollar terms, from January to October, the export value of plastic products decreased by 1% year-on-year. In the first ten months of this year, the total value of China's goods trade exports reached 308.471 billion U.S. dollars, a year-on-year increase of 5.3%, with the export growth of plastic products lagging behind the overall export growth of goods. In U.S. dollar terms, during the first ten months, the export value growth rates for automobiles, home appliances, and integrated circuits remained high, with year-on-year increases of 13.4%, -3.4%, and 23.7% respectively. The export quantities also maintained high growth rates, with year-on-year increases of 23.3%, -0.3%, and 19.2% respectively.

The polyolefin market is bottoming out amid weak fundamentals.

In the first 10 months, exports to the U.S. declined by 17.1% year-on-year, with the decrease expanding by 0.2 percentage points compared to the first 9 months. Imports from the U.S. decreased by 11.9% year-on-year, with the decrease expanding by 0.3 percentage points compared to the first 9 months. Although the suspension of additional tariffs between China and the U.S. has been extended by 90 days, under the current high tariff level of nearly 41.3%, the downward pressure on China's exports to the U.S. continues to increase, while the import momentum remains weak.

In the domestic polyolefin market, the first half of 2025 will see a concentrated release of expanded production capacity, with the growth rate of supply far exceeding that of demand, maintaining a situation of strong supply and weak demand. Polyolefin prices remain constrained by the reality of a weak fundamental outlook. In June, geopolitical factors gradually faded away, returning to a weakened fundamental situation. In July, influenced by the domestic macro "anti-involution" effect, prices rebounded somewhat. In August, without clear positive guidance, prices trended weakly downwards. In September, the downward weakness continued to explore the bottom, and in October, the weak downward trend persisted. It is expected that in November, prices will continue to seek a bottom before fluctuating.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

Zf asia-pacific innovation day: Multiple Cutting-Edge Technologies Launch, Leading Intelligent Electric Mobility

-

Fire at Sinopec Quanzhou Petrochemical Company: 7 Injured

-

Mexico officially imposes tariffs on 1,400 chinese products, with rates up to 50%

-

List Released! Mexico Announces 50% Tariff On 1,371 China Product Categories

-

Argentina Terminates Anti-Dumping Duties on Chinese PVC Profiles! Kingfa Technology & Siemens Sign Digital and Low-Carbon Cooperation Agreement