[pe daily review] oil prices plunge amid weak supply and demand, polyethylene prices fall across the board

I. Today's Summary

Expectations of a U.S.-Iran reconciliation have risen, easing geopolitical risks. International oil prices fell sharply, with both Brent and WTI dropping more than 3%, significantly weakening cost support for PE feedstock.

Domestic PE is experiencing a weak adjustment across the board, with HDPE leading the decline, and LLDPE and LDPE following suit. The overall market focus is shifting downward, and transactions are maintaining a weak demand based on necessity.

3. Futures prices have pulled back sharply, widening the spot-futures basis; industry production schedules have been adjusted slightly, with overall supply remaining ample, oil-based production continuing to incur losses, and coal-based production margins staying relatively high.

4. Market pessimism has eased marginally, but off-season demand remains weak, and the short-term market is expected to continue a weak consolidation trend.

II. Spot Market Overview

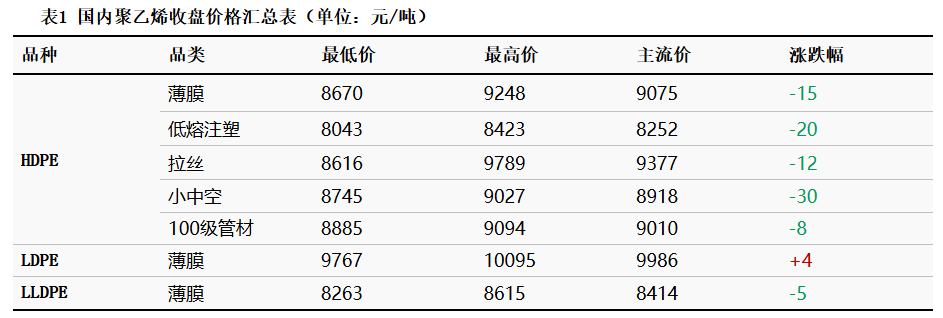

Today, the domestic polyethylene market declined overall, with mainstream prices falling by 20–120 yuan/ton during the day. On the cost side, prices continued to soften under the drag of a sharp drop in crude oil. Downstream demand remained in the traditional off-season, with end users cautious in replenishment and limited new orders. Trading activity was sluggish, and most holders offered concessions to facilitate transactions, with actual deals mainly concluded at the low end for rigid demand.

By grade, HDPE prices generally declined across specifications, with the overall range falling by RMB 46-151/ton. Small blow molding, film, and injection molding grades showed particularly weak performance; mainstream LLDPE prices were cut by RMB 88/ton; and LDPE prices were lowered by RMB 90/ton. Only high-pressure film grades showed slight resilience, indicating a structurally divergent market.

3. Spot-Futures Basis

The main LLDPE futures contract weakened sharply intraday, closing at RMB 7,646/tonne, down RMB 287/tonne on the day. The weakness in futures weighed on spot market sentiment, widening the futures-spot basis to RMB 334/tonne, up RMB 136/tonne from last week. Spot prices remained relatively stronger than futures, but overall market upside momentum was insufficient.

IV. Production Dynamics

Today, the PE industry’s production scheduling structure saw a slight adjustment. Linear film accounted for the highest share of scheduled production, while scheduled production of HDPE pipe and blow molding increased, keeping supply relatively ample. Scheduled production of HDPE film and LDPE film declined, and the proportion of units shut down edged up, partially offsetting the supply increase.

The profit side shows a clear divergence. Currently, oil-based PE is deeply in loss, with a per-ton loss of RMB 582; coal-based production enjoys a pronounced cost advantage, with per-ton profits exceeding RMB 1,000, and producers are relatively active in shipping. Weekly data indicate that industry operating rates and output are expected to rise, inventories continue to decline, and the overall supply-demand pattern remains loose.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

A Look at the Material Suppliers Behind SpaceX

-

Government's Triple Action, Enterprises' Three Arrows in Five Days, Semiconductor Reshuffle! What Signal Does Japan's Chemical Industry Release?

-

Fire breaks out at jiangsu meiside!

-

Ethylene: Production Capacity Accelerates Expansion, Global Industry Landscape Is Being Reshaped

-

Name change without tax change: POM Anti-Dumping Duty Rate Inheritance Implemented