How Far Can Polyethylene "Rise" in April After March Surge

Data Source: JLC

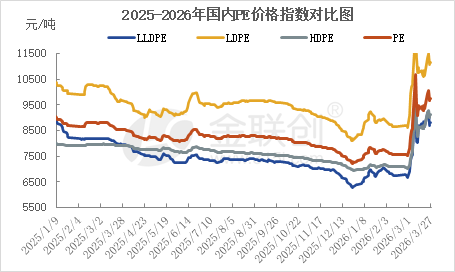

In March 2026, domestic PE prices in China surged after an initial pullback, rising significantly overall. Following the U.S.-Israeli military strike against Iran on February 28, the Strait of Hormuz—the world’s critical energy chokepoint—was effectively closed. Robust cost support coupled with expectations of reduced Middle Eastern supply triggered a sharp rally in the PE market, with LDPE leading the gains. However, on March 10, as geopolitical tensions eased and the risk premium associated with the U.S.-Iran conflict rapidly unwound, prices plunged swiftly, partially reversing the earlier gains. Thereafter, market sentiment swung violently amid recurring news developments—including the U.S.-Iran conflict, the status of the Strait of Hormuz, and Sinopec’s announced production cuts. As of March 27, the domestic PE price index stood at 9,759, up 2,250 from the end of the previous month; the LLDPE index reached 8,815, up 2,148 month-on-month; the LDPE price index hit 11,139, up 2,519 month-on-month; and the HDPE price index stood at 9,105, up 2,087 month-on-month.

In April 2026, the market will continue to fluctuate based on the actual passage situation in the Strait of Hormuz, crude oil prices, the extent of load reduction by domestic oil-based enterprises, and the real strength of downstream resumption orders. In April, there will be an increase in the maintenance of domestic facilities. Due to crude oil supply issues, most oil-based production enterprises will reduce their loads by 10%-30%. The reduction in Middle Eastern supplies will lead to a decrease in incoming shipments, and the widening of the price gap between domestic and international markets may further open up the export window, potentially alleviating some of the pressure on the domestic supply chain. There is an expectation of further tightening of the domestic supply. However, high-priced inventories from the earlier period still need to be digested. From a demand perspective, the peak season for ground film demand will end in late April. Given the significant fluctuations in domestic raw material prices, the market sentiment is expected to be cautious, with a focus on purchasing as needed. Both downstream buyers and intermediaries show a clear resistance to high prices, mostly buying as they use, with a low willingness to stockpile. In summary, the market in April will present a picture of tightening supply, with cost support, but possibly weak demand. The market is expected to experience significant volatility within a range, with linear prices between 8,500-10,000 yuan/ton. A price breakout to the upside would require an unexpected driver, such as an escalation of the conflict in the Middle East leading to a new high in oil prices, or an increase in the load reduction by domestic petrochemical companies. A significant price drop, on the other hand, would require an unexpected plunge in oil prices or a demand that is below expectations. It is recommended to closely monitor the actual passage situation in the Strait of Hormuz, crude oil prices, the extent of load reduction by domestic oil-based enterprises, and the real strength of downstream resumption orders.

The oil war premium caused by the Middle East conflict will not be digested in the short term. Domestic oil-based enterprises reducing production will not be completed in the short term. Meanwhile, the opening of domestic export windows makes it unlikely for market prices to return to the low levels before the war. After the sharp rise in March, market participants' sentiment has become more rational. Downstream and middlemen are no longer easily chasing price increases. Additionally, with increased new capacity in China during the second half of the year, it is unlikely for price levels to break through and set new highs above the March peak.

Domestic policy provides a floor for market conditions, with April entering a period of intensive policy implementation following the Two Sessions. The 2026 economic growth target is set at 4.5%-5%, with a deficit ratio of 4%, and 11.89 trillion yuan in new government bonds, indicating a policy orientation of being "more proactive and effective." Monetary policy will continue to be "moderately loose," with the central bank clearly stating that it will use a combination of tools such as lowering reserve requirement ratios and interest rates. For the polyethylene industry, the most critical policy signal is the first inclusion of "anti-rat race" in the government work report, which will curb the disorderly expansion of low-end general materials. At the same time, the "dual new" policies are entering the implementation phase, providing demand support for key downstream sectors such as home appliances, automobiles, and packaging. Overall, in April, the domestic macro environment will provide a bottom support for polyethylene, but upward elasticity still needs to wait for substantial improvement in demand.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

Deadly Impact: Hormuz Strait Blockade Sparks Shortage of Plastic Raw Materials, Threatening Shutdowns at Japanese and Korean Chemical Plants

-

BASF's $8.7 Billion Zhanjiang Site Fully Operational, Covestro, SABIC, Arkema and Other Plastics Giants Double Down on China

-

LG Chem Shuts Down Yeosu Unit 2, Sparking Chain Shutdowns Across South Korea’s Petrochemical Industry

-

Massive Loss of $960 Million! Wansheng Co., Ltd. Sees Rising Revenue But Declining Profits—Why Did the Phosphorus-Based Flame Retardant Leader Falter?

-

SABIC Declares Force Majeure on Styrene Monomer and Methanol Production; Middle East Chemical Operations Halted