US-Iran "Islamabad Memorandum" Takes Effect! Geopolitical Premium Cleared, PET Bottle Flakes Break 8000 Yuan Mark

In the early morning of June 15, 2026, the Iranian Foreign Ministry officially announced that after months of protracted negotiations, the United States and Iran have finalized the complete text of a memorandum of understanding. This document, referred to as the "Islamabad Memorandum," is scheduled to be signed by the three parties in Geneva, Switzerland, on June 19, with Pakistan serving as the coordinating witness. The Strait of Hormuz, which has been under substantial flow restrictions for three and a half months, is set to reopen with a clear timeline. The energy and polyester supply chain markets are consequently experiencing significant fluctuations.

I. Core Framework of the Agreement: 60-day transition period, cross-Strait navigation, easing of sanctions.

The agreement was jointly confirmed by the United States, Iran, and Pakistan. On June 14 local time, U.S. President Donald Trump was the first to “officially announce” the news on social media, saying that “the U.S.-Iran agreement is now complete” and that “the Strait of Hormuz will reopen, and oil tankers can start their engines.” In the early hours of the following day, Iran’s Supreme National Security Council and Deputy Foreign Minister Gharibabadi successively confirmed that the agreement had been reached. Pakistani Prime Minister Shehbaz Sharif also officially announced that, after intensive consultations, the United States and Iran had reached a peace agreement.

According to the detailed contents of the 14-point memorandum disclosed by Iran’s Mehr News Agency, the core provisions include:

Global permanent ceasefireAll fronts immediately cease military actions, including the Lebanon front.

Strait of Hormuz ReopenedResume navigation within 30 days in accordance with Iran’s arrangements, with Trump emphasizing that “no transit fees are required”;

Lift the maritime blockadeThe United States will fully lift its maritime blockade of Iranian ports within 30 days;

Oil sanctions suspendedThe U.S. has suspended sanctions on the sale of Iranian oil, petrochemical products, and their derivatives, allowing Iran to fully utilize the related financial income.

60-day transition negotiation periodThe two sides will engage in 60 days of negotiations, focusing on the nuclear issue and the comprehensive lifting of sanctions.

Asset unfreezingDuring the negotiations, $24 billion of Iran’s frozen assets shall be unfrozen, with half of that amount to be made available to Iran before the negotiations begin.

Reconstruction PlanThe United States and its allies must propose an Iran reconstruction plan totaling at least $300 billion.

The memorandum also clearly stipulates that Iran’s missile program and its support for resistance groups in the region are excluded from the agenda of the final agreement. The launch of the final agreement is subject to preconditions: half of the frozen assets must first be unfrozen, oil sanctions suspended, and the maritime blockade lifted.

Looking back over the entire negotiation process, since the United States and Israel launched military strikes against Iran on February 28 the two sides endured 106 days of conflict and "fighting while negotiating." The negotiations came close to collapsing four times — on May 18–19 Trump announced that he had originally planned to carry out a major military strike against Iran, and it was only postponed thanks to the mediation of the leaders of Qatar, Saudi Arabia, and the United Arab Emirates. The conclusion of this memorandum was thus hard-won.

II. Market Immediate Reaction: Crude Oil Plummets, PET Bottle Chips Fall Below 8000 Yuan.

After the news was released, the capital market responded quickly. On the morning of June 15, international crude oil saw its largest intraday drop expand to 7%, with an overall decline of over 4%. As of 15:48 on June 15, ICE Brent crude fell by 5.32%, trading at $82.68 per barrel, the lowest level in nearly three months; WTI crude dropped by 6.07%, trading at $79.73 per barrel, falling below the key $80 per barrel mark. According to data from Wenhua Finance, the WTI crude oil futures main contract hit a low of $80 per barrel, the lowest since April 17 of this year.

The core driver of this round of decline remains geopolitics: U.S.-Iran negotiations have further advanced, with both sides stating that the memorandum text has been finalized. Market expectations for a ceasefire, the reopening of the Strait of Hormuz, and the resumption of oil passage have risen markedly. Gold, silver, U.S. stock futures, cryptocurrencies, and other assets have all strengthened in tandem, while safe-haven funds have flowed out of the oil market en masse.

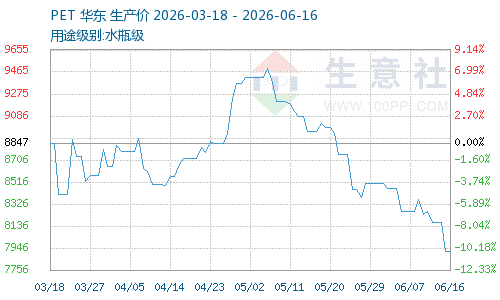

The impact transmitted to China’s domestic polyester industry chain, with the collapse on the cost side quickly materializing. In the futures market, the main PET bottle chip contract plunged by more than 5% in early trading. According to price data from SunSirs, the PET benchmark price on June 15 was RMB 8,170.00/ton, down 3.91% from the beginning of the month (RMB 8,502.50/ton). In the spot market, mainstream negotiated prices for PET bottle chips in East China were also sharply lowered, with spot prices breaking directly below the RMB 8,000/ton threshold. In terms of specific corporate quotations, Jiangsu Sanfangxiang quoted PET at RMB 7,830/ton, while Zhejiang Wankai quoted PET at RMB 7,950/ton, both down sharply from the previous trading day; Far Eastern Industries Shanghai, China Resources Zhuhai, China Resources Jiangyin and other companies all cut their bottle chip quotations to RMB 8,000/ton, with single-day declines reaching RMB 350–400/ton. On June 16, the SunSirs PET benchmark price fell further to RMB 7,915.00/ton, down 6.91% cumulatively from the beginning of the month.

Three, the underlying logic of price decline: clearing of geopolitical premiums and reversal of supply gap expectations.

First, the Middle East geopolitical risk premium was rapidly unwound.The core support that had previously sustained international oil prices and raised the costs of polyester raw materials—the geopolitical premium from the Middle East conflict—has rapidly dissipated with the establishment of a peace agreement. The market is no longer willing to pay an additional risk premium for disruptions in strait shipping or oil transportation, leading to a return to the fundamentals of supply and demand in oil pricing. Some analyses suggest that even if the Strait of Hormuz resumes navigation in the short term, it will take at least six months to physically restore Middle Eastern oil supply to pre-conflict levels. However, market pricing has never been based on "current physical supply," but rather on "future expectations"—once expectations shift, prices will respond accordingly.

Secondly, the logic of PX and PTA raw material shortages has been completely undermined.Long-term tracking data from SunSirs show that before the agreement was implemented, operating rates at Asian PX plants had long hovered at 64%–65%, a multi-year low. The market has widely been concerned that disruptions to Middle Eastern crude oil and aromatics transportation could trigger feedstock supply interruptions, which has become the core driver behind continued inventory drawdowns and firm prices for PX and PTA. As navigation through the Strait of Hormuz resumes, the Middle East crude oil and aromatics supply chain is expected to be restored in an orderly manner within the coming weeks, fully reversing the market’s long-held expectations of a hard structural shortfall in feedstock supply. Once the current round of concentrated PTA maintenance is over, producers’ willingness to restart will rise sharply; in the medium to long term, the feedstock supply gap will continue to narrow, and cost support for PET bottle-grade chips will keep weakening.

IV. Fundamentals of bottle chip supply and demand weakened simultaneously, with both domestic and external pressures amplifying the decline.

The decline in crude oil prices is merely an external trigger for the price drop; the fundamental reason for the sustained weakening of the market lies in the shift of the PET bottle chip supply and demand pattern from tight to loose.

Supply side: capacity is steadily being released, and inventory continues to accumulate.The overall capacity utilization rate of PET bottle flakes in the country has rebounded from a low of 71% to 71.9%. Multiple production units that were previously shut down for maintenance have gradually restarted, and the new capacity of 200,000 tons from Shaoxing Tiansheng is continuously being released. According to data from Business Society, the usable days of finished product inventory at bottle flake factories have risen from an extremely low level at the end of April to over 9 days, indicating a gradual emergence of supply pressure. In the long term, the pace of capacity expansion for domestic bottle flakes is relatively fast, with total capacity reaching 21.53 million tons by 2026, leading to existing overcapacity pressure. With the implementation of the Yimei Agreement and the alleviation of logistics bottlenecks for raw materials in the Middle East, along with the end of the concentrated maintenance period for production units in June and July, the operating rate of domestic bottle flakes is likely to further rise above 75%, resulting in a continued increase in supply.

Demand side: The traditional peak season has underperformed expectations, and downstream restocking momentum remains insufficient.Although the soft drink industry still has rigid procurement demand, previously high raw material prices have squeezed corporate profits, and downstream manufacturers generally purchase only as needed, with no large-scale concentrated restocking. Overall market demand is showing a “peak season that fails to peak” pattern, and polyester demand is highly likely to reach a phased turning point in the second half of June. In addition, following the easing of tensions between Iran and the United States and the resulting improvement in the circulation of overseas cargoes, the price competitiveness and sustainability of domestic bottle-grade PET export orders are facing challenges, putting both domestic and external demand under pressure simultaneously.

Overall, weakening international crude oil prices acted as an external downward force, while loose supply and demand within the industry served as an internal drag. Under the resonance of these dual bearish factors, PET bottle chip prices fell by 320 yuan in a single day, a decline significantly greater than that of upstream PX and PTA raw materials.

V. Outlook: RMB 8,000 has shifted from support to resistance, and the price center of gravity continues to move downward

Based on the spot price trends from the business community, supply and demand data in the industry chain, and changes in geopolitical policies, the PET bottle chip market can be roughly divided into two phases.

Short term (1–2 weeks): Sentiment-driven weak fluctuations, with a range of RMB 7,800–8,000/tonne.The negative sentiment brought about by the peace agreement will be fully released, making it difficult for crude oil to experience a significant rebound in the short term. If the agreement is executed smoothly, risk-averse funds will flow back to precious metals, putting pressure on crude oil and continuing its weak trend. In the corresponding PET bottle chip spot market, the 8,000 yuan level has completely shifted from a previous strong support to a key resistance level, and the market is likely to operate weakly in the range of 7,800-8,000 yuan/ton. Business Society's spot quotes may continue to hover at the lower end of this range.

Medium term (1–2 months): Fundamentals are repriced, and three key variables determine the downside.Market pricing logic will shift away from geopolitical conflicts and return to the supply-demand fundamentals of the polyester value chain. The key factors to watch in the subsequent market trend are threefold: the actual pace of recovery in the Middle East aromatics and crude oil supply chains; the pace of industry restart and production resumption after the completion of PTA maintenance; and whether downstream sectors will see a concentrated restocking window as the traditional peak season for beverages comes to an end.

Moreover, uncertainty remains within the agreement itself. This memorandum offers Iran “conditional, phased, reversible, and temporary breathing space,” rather than dismantling the sanctions regime targeting Iran. Tough issues such as control over the Strait of Hormuz, Iran’s nuclear program, and regional proxies still require prudent resolution by both sides and even multiple parties. If negotiations break down during the 60-day transition period, the geopolitical premium could return—but before that, the market will re-anchor a reasonable price range based on real supply and demand.

The signing of the Imei Peace Agreement marks the official end of the "geopolitical premium bull market" that has supported the energy and polyester markets for months. Currently, the PET bottle chip market is facing a dual negative environment with continuously loosening cost support and a shift from tight to loose industry supply and demand. Data from the Business Society's spot monitoring indicates that the 8,000 yuan mark has been effectively breached. The market will move away from geopolitical speculation and re-anchor to a reasonable price range based on real supply and demand, with short-term downward pressure still present.

Editor: Winnie

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

A Look at the Material Suppliers Behind SpaceX

-

Government's Triple Action, Enterprises' Three Arrows in Five Days, Semiconductor Reshuffle! What Signal Does Japan's Chemical Industry Release?

-

Next-generation motors of new energy vehicles: Single-Round Thousand Horsepower, Replacing Brakes, How Powerful Are They?

-

Shutdowns And Production Cuts! Widespread Price Quotes Suspended, Chemical Products May Still Be Easier To Rise Than Fall In June-July!

-

Japan Plans To Sell Lithography Giant JSR! Fujifilm And Mitsubishi Chemical Interested In Taking Over, How Much Time Window Is Left For China?