[today's plastics market] general materials narrowly decrease, engineering materials partially fluctuate, pa6 contrary rise up to 300

Summary: On July 31, the prices and forecasts for general-purpose and engineering plastics markets were summarized. General-purpose plastics overall experienced a slight decline; the PP market loosened slightly with some prices dropping by 10-30; PE showed minor fluctuations with changes ranging from a 1 to 7 increase or decrease; PVC oscillated and retreated, falling by 30-70; PS prices decreased to boost sales, dropping by 20-30; ABS remained mostly stable with slight fluctuations, declining by 50-100. Engineering plastics saw localized adjustments; PET prices declined, dropping by 40-50 in some cases; PA6 held firm with increases ranging from 50 to 300; PC, POM, PBT, PMMA, and PA66 remained stable and consolidated.

General Material

PE: Market sentiment weakens, with the price center slightly shifting downward.

1. Today's Summary

OPEC+ may continue to significantly increase production in September, leading traders to take profits, and resulting in a decline in international oil prices. NYMEX crude oil futures for the September contract fell by $0.74 to $69.26 per barrel, a month-on-month decrease of 1.06%; ICE Brent crude futures for the September contract fell by $0.71 to $72.53 per barrel, a month-on-month decrease of 0.97%.

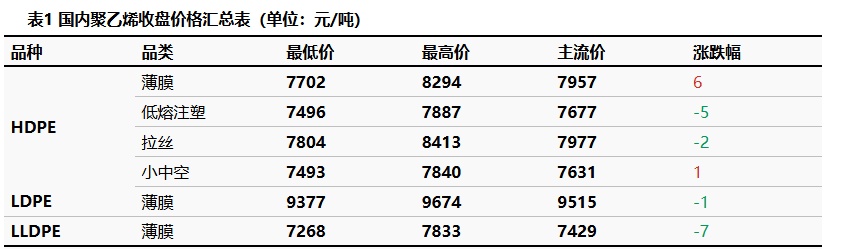

②. The HDPE market price changed by -5 to -6 yuan/ton, the LDPE market price by -1 yuan/ton, and the LLDPE market price by -7 yuan/ton.

2. Spot Overview

Macroeconomic news has been gradually digested, with no further boosts, and cost-side support has weakened. The spot market supply is relatively ample, leading to minor price concessions to facilitate transactions, resulting in a downward shift in price focus and continued weak trading activity. Currently, the market is mainly driven by macro sentiment, with a relatively strong mentality. However, from a fundamental perspective, there has been no significant change in supply, and pressure remains, while demand is recovering slowly and is unlikely to generate effective upward momentum. Therefore, a slight consolidation is expected to be the main trend. The HDPE market price fluctuated by -5 to 6 yuan/ton, the LDPE market price by -1 yuan/ton, and the LLDPE market price by -7 yuan/ton.

3. Price Prediction

Short term Within the period, the rebound in off-season demand was limited, downstream purchasing volume was small, maintaining just the necessary demand, the impact of news gradually faded, and the market sentiment turned weak. Therefore Polyethylene market priceOscillating downward Mainly.

PVC: Insufficient supply and demand expectations, PVC fluctuated and pulled back during the session.

1. Today's Summary

① Domestic PVC manufacturers have reduced ex-factory prices by 30-120 yuan/ton.

The number of maintenance enterprises has rapidly decreased in the short term, and the market supply is expected to increase quickly.

The Politburo meeting reiterated its determination to "combat involution": promoting capacity management in several key industries, with the Producer Price Index (PPI) expected to recover in the second half of the year.

2 Spot Market Overview

Based on the Changzhou market in East China, today the spot cash warehouse pick-up price for acetylene-based PVC type 5 in East China is 4,920 yuan/ton, down 30 yuan/ton compared to the previous trading day. 。

The domestic PVC spot market price focus fluctuated lower. In the absence of policy or macro expectations for support, market prices returned to fundamentals. During the week, upstream PVC supply steadily increased, while demand improvement was limited. Industry inventory continued to accumulate for over five weeks, putting pressure on spot prices. In East China, the carbide method type five spot cash delivery was at 4,820-5,000 yuan/ton, while the ethylene method was stagnant at 4,950-5,200 yuan/ton.

3、Price forecast

From a fundamental perspective, next week the maintenance efforts of domestic PVC producers will ease, with the scale of new maintenance lower than the scale of restarts and new capacity additions, leading to a continuous increase in production. Domestic demand remains in the off-season, and new export orders are limited due to weak off-season demand and the impact of policies in India. Industry inventory is expected to continue accumulating, putting downward pressure on spot prices. Considering there is no short-term policy stimulus, the spot market is expected to fluctuate and decline. It is forecasted that the cash price for the five-type calcium carbide-based PVC in East China will be in the range of 4,750-4,900 yuan/ton.

PS: Raw material prices slightly weaken, market lowers prices to clear inventory.

1 Today's Summary

Today, the GPPS in East China stabilized at 7,830 RMB/ton.

On Friday, the East China styrene market fell by 25 to close at 7,350 yuan/ton, South China fell by 20 to close at 7,415 yuan/ton, and Shandong fell by 15 to close at 7,190 yuan/ton.

2 Spot Overview

Table 1 Domestic PS Price Summary (Unit: RMB/ton)

|

Market |

Specifications |

Today's Price |

Change in Value |

Percentage Change |

|

Ningbo |

East China GPPS - Green Anqingfeng |

7830 |

0 |

0% |

|

Yuyao |

East China HIPS - Saibao Long |

8680 |

-20 |

-0.23% |

|

Shantou |

South China GPPS - Renxin |

7550 |

-30 |

-0.4% |

|

Shantou |

South China HIPS-Starshine |

8470 |

0 |

0% |

According to Longzhong Information, the East China GPPS price remained stable at 7,830 yuan/ton today.The upstream styrene market shows a weak trend with moderate cost support. Industry supply has slightly recovered, while downstream demand remains sluggish. Market transactions are average, with price reductions being the main strategy for sales.

3 Price Prediction

The raw material styrene is oscillating at a low level, with moderate cost support. Industry output has slightly recovered from a low level, and downstream demand is primarily driven by rigid demand purchases. In the short term, the PS market is expected to remain weak and consolidate. It is anticipated that the price of styrene monomer in the East China market will range between 7,800 and 8,700 yuan per ton.

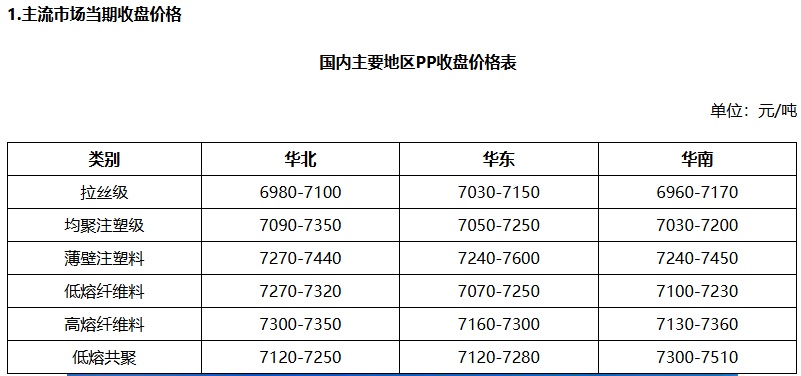

PP: The domestic PP market slightly softened.

1 Today's Summary

The domestic PP market showed slight weakening today, with prices falling by 10-30 yuan/ton. The PP futures fluctuated weakly, suppressing the spot market sentiment. Traders mainly focused on active selling, with quotations easing by 10-30 yuan/ton. Downstream purchasing intentions remain low, with actual transactions mainly centered on negotiations. In some regions, low-priced deals were relatively acceptable.

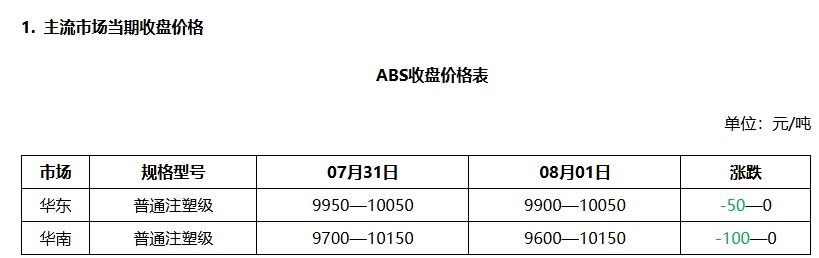

ABS: The ABS market showed steady and slight movements today.

1 Today's Summary

Today, the ABS market remained generally stable with minor fluctuations. Styrene futures fluctuated and declined during the day, leading to more cautious sentiment among market participants. Some traders were inclined to increase sales volume, but actual operations followed market trends. Overall, downstream replenishment was limited, and some sellers faced pressure to move inventory.

The mainstream price of domestic materials is 9,150-10,400 RMB/ton, with prices for general injection molding grade in East China and South China at 9,900-10,050 RMB/ton and 9,600-10,150 RMB/ton, respectively.

Engineering materials

PC: The market is quiet and weak.

1 Today's Summary

Thursday International Crude Oil Decline , ICE Brent crude oil futures September contract at 72.53 USD/barrel, down 0.71 USD/barrel.

②、 The closing price of raw material bisphenol A in the East China market is 8,000. Yuan/ton, stable compared to the previous period.

As the weekend approaches, there have been no new ex-factory price adjustments from domestic PC manufacturers.

2 Current Spot Overview

The domestic PC market in China operated with weak consolidation today. By the afternoon close, the mainstream negotiation reference for low-end injection molding grades in East China was 10,250-13,750 yuan/ton, while mid-to-high-end grades were discussed at 14,500-15,300 yuan/ton. The mainstream focus remained roughly stable compared to yesterday, with individual prices slightly lower by 50 yuan/ton. As the weekend approaches, there are no new factory pricing adjustments from domestic PC manufacturers, and the overall industry sales situation remains weak. Looking at the spot market, East and South China are primarily experiencing a stalemate. Although current PC prices have essentially hit historical lows, and upstream raw materials have been continuously rising recently, the market sentiment remains uninspired. The intense supply-demand contradiction in the industry persists, with many stockholders maintaining a wait-and-see attitude and continuing to be bearish. The downstream buying demand remains unchanged, and trading remains sluggish.

3 Price Forecast

Approaching the weekend, domestic PC news is relatively quiet, with factories showing no new price adjustment updates. The limited increase in raw material bisphenol A offers little boost to PC market sentiment, leading to a predominantly weak and low-level consolidation. Looking ahead to next week, strong supply and demand pressures will continue to be the main factors driving the PC market direction. It is expected that the domestic PC market will maintain a sluggish trend, with attention focused on the latest factory price adjustment updates early in the week.

PET: Polyester Bottle Chip Market Prices Decline

1 Today's Summary

① Factory quotes decreased by 40-100. (Unit: Yuan/Ton)

②. Today, the domestic polyester bottle chip capacity utilization rate is 70.89%.

2 Spot Market Overview

Table 1: Summary of Domestic Polyester Bottle Chip Prices (Unit: Yuan/Ton)

|

Market |

Specification |

7 31st of the month |

August 1st |

Change in value |

Change Percentage |

|

East China |

Aquarius-class |

5990 |

5950 |

-40 |

-0.67% |

|

South China |

Aquarius-class |

6050 |

6000 |

-50 |

-0.83% |

|

North China |

Aquarius-class |

5960 |

5920 |

-40 |

-0.67% |

Based on the East China region, today's spot price for polyester bottle-grade flakes settled at 5,950, down 40 from the previous working day, in line with the morning expectations.

Crude oil and raw materials declined, polyester bottle chip factory prices were reduced by 40-100, with transactions for August-September sources at 5970-6000. Downstream and traders took advantage of low prices to replenish stocks. The market focus subsequently declined, it is heard. August supply traded at 5890-6000 or futures contract 2509 with a discount of 20 to a premium of 60, September supply traded at 5890-5960, with significantly improved trading activity. (Unit: yuan/ton)

3. Price Prediction

On the supply side, there are currently no facilities restarting, and the supply remains stable. On the demand side, downstream maintains just-in-time replenishment, with the replenishment pace keeping to a strategy of restocking when prices are low. The spot market is relatively well-supplied, and under the pressure of raw material costs, the polyester bottle chip market may remain sluggish. It is expected that next week the spot price for polyester bottle chip water bottle grade in the East China market will be 5900-6000 yuan/ton. Attention should be paid to changes in raw materials.

PBT: Raw materials both decline, PBT market operates sluggishly.

1 Today's Summary

The PBT manufacturer's quotation remains stable.

② There are fewer PBT unit maintenance activities this week.

③ The PBT output for this period was 22,600 tons, a decrease of 500 tons from the previous period, representing a drop of 2.16%. The capacity utilization rate was 53.14%, down 1.32% from the previous period. This week, the average gross profit of domestic PBT is -548 RMB/ton, a decrease of 44 RMB/ton compared to the previous week. 。

2 Spot Market Overview

Table 1 Domestic PBT Price Summary (Unit: Yuan/Ton)

|

Market |

Specification |

2025/07/31 |

2025/08/01 |

Change in Value |

Change Percentage |

|

East China |

Medium-low viscosity pure resin |

7800-8300 |

7800-8300 |

0/ 0 |

0%/ 0% |

|

Key upstream |

|||||

|

East China |

PTA |

4826 |

4740 |

-86 |

-1.78% |

|

East China |

BDO (Sprinkling water) |

8100-8200 |

8000-8200 |

-100 / 0 |

-1.23% / 0% |

|

Data source: Longzhong Information |

|||||

Based on the East China region, today's mainstream price for low to medium viscosity PBT resin is between 7,800 and 8,300 yuan per ton, remaining stable compared to the previous working day.Today, the PBT market is weak and cautious, the PTA market is under pressure and declining, and the BDO market continues to explore lower levels. The raw material side continues to weaken, the PBT market remains weak and cautious, with an increasing willingness to trade at low prices, and the market sentiment is predominantly weak. According to Longzhong Information, the price of medium- and low-viscosity pure PBT resin in the East China market is 7,800-8,300 yuan/ton.

3 Price prediction

The PBT market is expected to experience weak fluctuations. On the raw material side, multiple domestic PTA facilities are undergoing maintenance, leading to a significant reduction in supply. However, the demand side is underperforming, with average production and sales activities in polyester companies, coupled with weakening trends in raw materials, resulting in the PTA spot market maintaining a weak pattern in the short term. For BDO, supply and demand pressures persist for next week, and there is a strong cautious bearish sentiment among industry players. Downstream businesses are following up as needed, and holders are maintaining a selling mindset, causing the market focus to shift towards the low-to-mid-end range. The continuous weakening of support from the raw material side adversely affects the PBT market sentiment, and there may be an increase in supply-side discount selling operations. Consequently, the market focus is expected to exhibit weak fluctuations. Therefore, Longzhong anticipates that next week the price of low-viscosity PBT resin in the East China market will be in the range of 7,700-8,200 yuan/ton.

PMMA: The PMMA market operates steadily with a lukewarm tone.

1 Today's Summary

①、 Today, the PMMA particle market remains stable.

② The utilization rate of domestic PMMA particles remains at 64% today.

2 Spot Overview

As of today, PMMA particles in the East China region closed at 13,000 yuan/ton, stable compared to the previous working day, in line with the morning forecast. Intraday, MMA feedstock prices saw a narrow increase, but cost support remained limited. Downstream buying interest was not high, and trading sentiment showed no improvement. Holders offered prices in line with the market, while participants maintained a strong wait-and-see attitude. Actual transaction prices fluctuated within a range, with low prices heard in the market.

3 Price prediction

The upward momentum on the raw material side is limited, and the market is mainly characterized by a wait-and-see attitude and stalemate. Downstream end-users are only maintaining procurement based on rigid demand. The current market price has fallen close to the bottom price; hold the inventory. Low willingness to underreport commercial value. The on-site real trade transaction needs to be conducted. The downward range of PMMA will narrow in the short term.

POM: Fundamental support, market fluctuates and moves higher

1. Today's Summary

① Domestic material manufacturers currently have no inventory pressure.

②. There are frequent price-supporting actions in the market.

2 Spot Market Overview

Table 1 Summary of Domestic POM Prices (Unit: Yuan/Ton)

|

market |

Specification |

July 31 |

August 1st |

Change in Value |

Change in Price Range |

|

Yuyao |

Yuntianhua M90 |

11000 |

11000 |

0 |

0.00% |

|

Dongguan |

Yuntianhua M90 |

10000 |

10000 |

0 |

0.00% |

|

North China |

Yuntianhua M90 |

11000 |

11000 |

0 |

0.00% |

|

Data Source: Longzhong Information |

|||||

In the Yuyao area as a benchmark, today's Yuntianhua M90 is priced at 11,000 yuan/ton, with the price remaining stable compared to the previous period.Today, the POM market experienced mixed fluctuations. The fundamentals provided strong support, leading to an increase in the ex-factory prices of domestic materials. The mainstream quotations remained relatively firm, with some grades rising slightly by around 100 yuan/ton. Imported materials continued to decline, with some dropping by 200-300 yuan/ton. By the end of the trading session, the tax-inclusive price of domestic POM in the Yuyao market ranged from 8,100 to 11,200 yuan/ton, while the cash price of POM in the Dongguan market ranged from 7,300 to 10,400 yuan/ton.

3. Price Forecast

This week, various manufacturers have collectively released their inventories, and the ex-factory prices of some domestic materials have been collectively raised. This has generally boosted traders' confidence, and the market trend is relatively firm. Some offers may continue to rise. End-users tend to buy when prices are rising and hold off when they are falling, with some engaging in replenishment as needed. However, given the insufficient operating rates of downstream factories, purchasing follow-up is relatively limited. Longzhong expects that the domestic POM market will run relatively strong in the short term.

PA6: The raw material market remains strong; the PA6 market is rising.

1 Today's Summary

Sinopec high-end caprolactam settlement price for July 2025 is 9,060 RMB/ton (liquid premium grade, six-month acceptance self-pickup), down 660 RMB/ton compared to the June settlement price.

Sinopec has increased the price of pure benzene by 100 RMB/ton at its refineries in East and South China, implementing a new price of 6,050 RMB/ton, effective from July 29.

2 Spot Overview

Table 1 Summary of Domestic Polyamide 6 Prices (unit: RMB/ton)

|

Market |

Specification |

7 31st of the month |

August 1st |

Change in Value |

Payment Terms |

|

Polyamide 6 regular spinning chips |

Factory Price (Standard) |

9100-9400 |

9150-9550 |

+50/+150 |

Cash Ex-factory |

|

Ex-factory price (high-end) |

9300-9800 |

9400-10000 |

+100/+200 |

Cash factory delivery |

|

|

East China Market (General) |

9300-9600 |

9350-9750 |

+50/+150 |

Delivered to East China |

|

|

East China Market (High-end) |

9300-9800 |

9400-10000 |

+100/+200 |

East China Self-Pickup |

|

|

Polyamide 6 high-speed spinning chips |

East China Spot (Ordinary) |

9200-9400 |

9300-9500 |

+100/+100 |

FOB (Free on Board) |

|

East China Spot (Premium) |

9600-9900 |

9800-10200 |

+200/+300 |

Acceptance received |

|

|

Key upstream |

|||||

|

Caprolactam |

East China |

8975 |

8975 |

0 |

Accepted and Delivered |

|

Data source: Longzhong Information |

|||||

Today, the market price of polyamide 6 has increased. The supply of raw material caprolactam has decreased locally, and market prices remain strong. With losses in slice profits and high cost pressures, polymerization enterprises have followed suit by raising slice prices. However, downstream sentiment is gradually becoming cautious, and overall market transactions are moderate. In East China, regular spinning PA6 is priced at 9350-9750 CNY/ton for cash and short delivery, while high-speed spinning spot is at 9800-10200 CNY/ton for acceptance delivery. In Chaohu, the cash pick-up price is 8700-8800 CNY/ton.

3 Price prediction

From the cost perspective, the caprolactam market is experiencing significant cost and supply pressure, which may lead to a continued firm market trend, and pressure on slice costs still exists. From the supply and demand perspective, the operating rate of domestic polymerization enterprises is slowly increasing, with plans for new capacity to be introduced, indicating ample supply. However, downstream sentiment is becoming cautious, and it is expected that the PA6 market will see slight adjustments in the near future.

PA66: Fundamentals remain stable, market consolidates and operates steadily.

1 Today's Summary

①, 7/31: OPEC+ may continue to increase production significantly in September, leading to profit-taking by traders and a drop in international oil prices. NYMEX crude oil futures for the September contract fell by $0.74 to $69.26 per barrel, a decrease of 1.06% compared to the previous period; ICE Brent crude futures for the September contract fell by $0.71 to $72.53 per barrel, a decrease of 0.97% compared to the previous period. China's INE crude oil futures main contract 2509 rose by 8.2 to 532 yuan per barrel, but fell by 3.8 to 528.2 yuan per barrel in the night session.

Today, the domestic PA66 operating rate is 60%, with a daily output of about 2,300 tons. Under cost and demand pressure, the operating rate of domestic PA66 polymerization enterprises remains stable. However, downstream demand is average, and the supply of PA66 in the domestic market is sufficient.

2 Spot Overview

Table 1: Summary of Domestic PA66 Prices (Unit: RMB/ton)

|

Market |

Specifications |

7 Month 31 Day |

August 1 |

Change in Value |

Change in Price Percentage |

|

East China |

EPR27 |

15600 |

15600 |

0 |

0% |

|

Key Upstream |

|||||

|

East China |

Adipic acid |

7100 |

7125 |

+25 |

+0.35% |

|

Data source: Longzhong Information |

|||||

Based on the Yuyao market in the East China region, today's EPR27 market price is referenced at 15,500-15,700 RMB/ton, stable compared to yesterday's price. 。 The raw material adipic acid has been rising with fluctuations, keeping cost pressures high. Downstream buyers are mainly purchasing as needed, market supply is ample, and the market is operating in a consolidating manner.

3 Price Prediction

The pressure on costs remains unabated, downstream purchasing is on-demand, and the market supply is ample. It is expected that the domestic PA66 market will stabilize in the short term.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift