[Today’s Plastic Market] Downward Trend Difficult to Change! PP, PE, PVC, PET Narrowly Decline, PC Drops Up to 150

Abstract: Summary of prices and forecasts for general-purpose and engineering plastics on October 14.General MaterialIn terms of the above content,The upstream inventory pressure still exists.PP, PE, and PVC are weak and declining; ABS market is filled with bearish factors, with some dropping by 30-100; EVA continues to decline, with some dropping by 50-100.。Engineering materialsIn terms of aspects, PC is weak and fluctuating, with some falling by 50-150; PET is slightly declining by 30-40; PA6 is operating weakly, with some falling by 100; PBT, POM, PMMA, and PA66 are observing and running stably.

General materials

PE: Abundant supply, transaction prices decline.

1. Today's Summary

①. The U.S. rhetoric on imposing tariffs has softened, combined with the ongoing Russia-Ukraine conflict still posing potential supply risks, leading to an increase in international oil prices. NYMEX crude oil futures for the November contract rose by $0.59/barrel to $59.49, a week-on-week increase of +1.00%; ICE Brent crude futures for the December contract rose by $0.59/barrel to $63.32, a week-on-week increase of +0.94%.

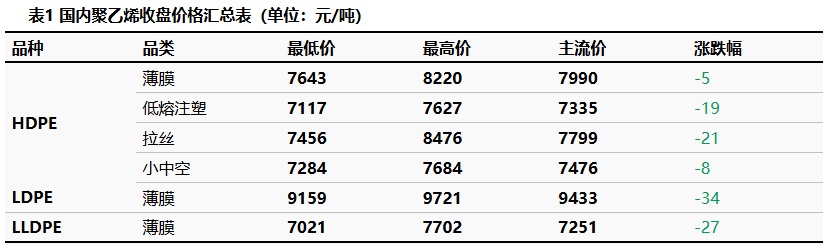

The price fluctuation range for the HDPE market is -21 to 5 yuan/ton, the LDPE market price is -34 yuan/ton, and the LLDPE market price is -27 yuan/ton.

2. Spot Overview

The current polyethylene market is well-supplied, and downstream factories mainly purchase on demand. Traders, in order to alleviate inventory pressure, tend to sell at a discount, which leads to a decline in actual transaction prices. Although seasonal demand, such as agricultural film, provides some support to the market, the overall supply pressure remains significant with the continuous release of new production capacity, and the speed of destocking in society is slower than expected. The HDPE market price fluctuation range is -21 to -5 yuan/ton, LDPE market price is -34 yuan/ton, LLDPE market price is -27 yuan/ton.

3. Price Prediction

The current polyethylene market is experiencing significant supply pressure. After the holiday, domestic facilities that were previously undergoing maintenance are gradually restarting, and there are plans to release new production capacity. Additionally, imported resources are arriving relatively concentrated, collectively exacerbating the pressure on the supply side. In terms of demand, downstream factories are generally cautious in their purchasing behavior, mainly restocking as needed, providing limited support to the market. Considering both supply and demand factors, it is expected that the polyethylene market prices will show a weak consolidation trend tomorrow, with fluctuations likely in the range of 10-50 yuan/ton.

PP: Upstream Inventory Pressure Persists, Polypropylene Market Weakens and Declines

1. Today's Summary

①, Sinopec East China Shandong warehouse PP slightly decreased, Lanzhou Petrochemical 9018 reduced by 100 to set at 7,350 yuan/ton. Sinopec South China PP Guangxi Petrochemical L5E89 increased by 20 yuan/ton to set at 6,700 yuan/ton, L5D98C decreased by 50 yuan/ton to set at 6,850 yuan/ton, Dushanzi K8003 decreased by 100 to set at 7,450 yuan/ton.

②. Today, the domestic polypropylene shutdown impact has increased by 2.13% compared to last week, reaching 18.31%. Jineng Chemical's second phase 450,000 tons/year facility, Yulong Petrochemical's third line 400,000 tons/year, and fifth line 300,000 tons/year facilities are shut down, with an expected reduction in daily supply of 3,450 tons. The daily production proportion of yarn-grade has decreased by 3.22% compared to last week, falling to 23.24%. This is mainly due to the Shijiazhuang 200,000 tons/year facility switching to injection molding, Jingmen Petrochemical's 120,000 tons/year facility switching to fiber, and Yulong Petrochemical's first line 400,000 tons/year facility switching to transparent grade, with an expected reduction in yarn-grade production of 2,160 tons per day.

③、(20251003-1009) The supply-demand balance has shifted from a tight balance before the festival to a surplus.This will exert some pressure on market sentiment. After the holiday, as factories resume operations, the supply-demand balance in the next period will be somewhat supported by the growth in demand from most downstream sectors.

2. Spot Overview

Using the East China region as a benchmark, today's polypropylene raffia closed at 6,620 yuan/ton, a decrease of 40 yuan/ton compared to yesterday. The nationwide average price of raffia is stable compared to yesterday, in line with the morning forecast.

Futures fluctuated lower today, with morning market offers falling by 20-50 yuan/ton. International trade barriers are rising again, leading to cautious sentiment in the market. Limited follow-up from the demand side is putting downward pressure on the market, prompting merchants to carefully mitigate risks and offer discounts to sell. As of midday, the mainstream price for East China wire was between 6,550-6,700 yuan/ton.

3. Price Prediction

Currently, downstream factories have limited new orders, slow improvement in production, and general enthusiasm for raw material procurement. Coupled with renewed international trade barriers affecting market sentiment, upstream inventories accumulated during the holidays, leading to significant inventory pressure across the supply chain. It is expected that tomorrow... Polypropylene Market Fluctuating around the 6500-6700 yuan range, with a focus on changes in demand and supply.

PVC: Low Price Transactions, Supply and Demand Remain Weak

1. Today's Summary

①. The ex-factory prices of domestic PVC production enterprises have been partially reduced by 30-50 yuan/ton.

② Some units of Junzheng, Tianye, Lutai, and Xinfeng are under maintenance.

The Ministry of Transport announced that starting from October 14, a special port fee will be charged for American vessels.

2. Spot Overview

Based on the East China Changzhou market, the cash price for acetylene-based Type V in East China today is 4,580 yuan/ton, down 30 yuan/ton compared to the previous trading day.

The domestic PVC spot market is experiencing a weak and fluctuating trend, with spot prices continuing to decline by 10-30 yuan/ton. The one-price transactions in the spot market are stagnant, and intraday prices are influenced by the drop in bulk commodities, seeking lower transactions. End-users maintain low-price procurement. In the short term, the supply-demand pattern is not significantly improving, and the market trend increasingly affects the transaction focus. In East China, the cash price for calcium carbide-based PVC is between 4550-4680 yuan/ton, while for ethylene-based PVC it is between 4750-4950 yuan/ton.

3. Price Prediction

Domestic PVC supply has weakened slightly due to maintenance, but new capacity continues to drive production at a high level. Domestic demand remains stable, with downstream buyers stocking up at low prices. Foreign trade exports are performing moderately, resulting in an overall stalemate in the market supply and demand. Cost support is relatively weak, and there is insufficient bottom support. Recently, the market has been heavily influenced by the futures market, with expectations of a rebound in the prices of black and related bulk commodities helping to stabilize the market in a weak position. The expected price range for East China acetylene-based PVC is between 4600-4700 yuan/ton.

ABS: The market is filled with negative sentiment, and today traders are offering discounts to sell off inventory.

1 Today's summary:

1. Today, the prices in the East China market have decreased; the prices in the South China market have also decreased, and market transactions are maintaining basic demand.

The monthly production of ABS in October increased compared to the previous month.

2 Spot Overview:

Based on the regions of Yuyao and Dongguan, prices in the East China market are declining, and prices in the South China market are also falling. Today's market trading is sluggish, with many bearish factors present, and traders are not optimistic. Raw material prices continue to decline today, and it is expected that the domestic ABS market prices will continue a downward trend tomorrow.

3 Price Prediction:

Based on the regions of Yuyao and Dongguan, prices in the East China market are declining, while prices in the South China market are experiencing localized downturns. Today, market prices have fallen, while supply remains high. There are many negative factors in the market, leading to poor market sentiment. Raw material prices are declining, and it is expected that tomorrow ABS prices will continue to experience localized downward trends.

EVA: The market continues its weak downward trend, making transactions difficult.

1 Today's Summary

This week, the EVA petrochemical ex-factory price has been steadily adjusted downward.

② This week's EVA petrochemical plants: Gulei Petrochemical will start a shutdown for maintenance this afternoon, expected to last for 5 days. Except for the long-stopped Yanshan Petrochemical plant, all other plants are operating steadily. The 300,000 tons/year plant of South Korea's Hanwha-GS Energy began production on September 25.

2. Spot Overview

Today, the domestic EVA market continues to be weak. In a declining market, downstream factories are primarily focused on depleting their inventories. New orders from foam factories are weak, and the willingness for just-in-time purchasing is lacking. Pressure on sellers to offload goods has increased, making transactions difficult. The focus of real transactions continues to decline. Mainstream price: Soft material reference 10,600-11,100 RMB/ton, hard material reference 10,600-11,200 RMB/ton. 。

3 Price prediction

In the short term, the supply side is experiencing price loosening, making it even more difficult to build market confidence. The demand for photovoltaic procurement is slowing down, and new orders from downstream foaming terminals are not performing well. The peak season is not seeing sufficient demand follow-up, and the absorption of market spot resources is slow. Businesses are facing increased resistance in sales, and market prices may continue to be under downward pressure. It is expected that in the short term... The domestic EVA market shows a weak trend. 。

Engineering Materials

PC: The market is weak and fluctuating with adjustments.

1 Today's Summary

Monday International crude oil Rise , ICE Brent Crude Futures December contract at 63.32, up 0.59 USD/barrel.

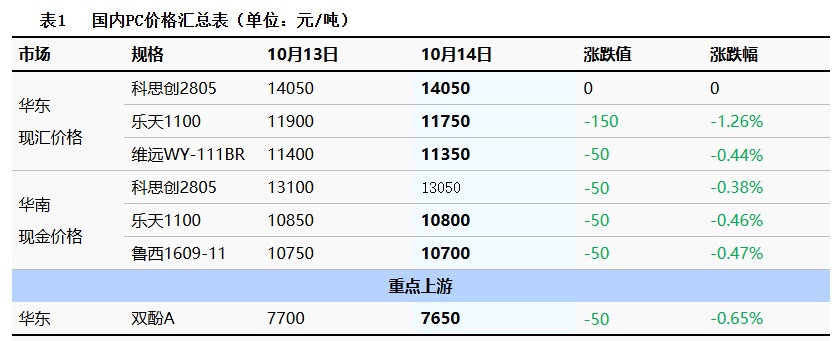

②、 Bisphenol A closed at 7650 in the East China market. Yuan/ton, a month-on-month decrease of 50 yuan/ton.

This week, the latest factory prices for domestic PC are stable or have increased by 100-200 yuan/ton.

2 Spot Overview

Today, the domestic PC market is experiencing a narrow range consolidation. As of the afternoon closing, the mainstream negotiation reference for low-end injection molding grades in East China is 10,400-13,400 RMB/ton, while mid-to-high-end grades are negotiated at 14,050-14,800 RMB/ton. The overall focus remains roughly stable compared to last Saturday. At the beginning of the week, there is little news about the latest ex-factory guidance from domestic PC manufacturers. Only a certain PC factory in Southwest China has raised its latest ex-factory price by 200 RMB/ton. In terms of the spot market, both East and South China are maintaining stability and consolidating. There are no new favorable factors to boost the fundamentals, and downstream buyers, after a phase of purchasing, are mainly observing and digesting inventory. Traders are becoming more cautious, conducting flexible negotiations and transactions, with some reports of low-priced offers circulating.

3 Price Prediction

Currently, the overall response in the domestic PC market shows significant differentiation. Factories' attempts to maintain prices have insufficiently boosted the spot market, and with profit-taking and inventory management, the market's focus has been trending downwards. In the short term, the main PC factories' equipment maintenance and the continued expectation of overall supply being relatively low in the fourth quarter will still support PC prices. However, considering the slow pace of spot inventory digestion and the weak influence of most related products, the domestic PC market is expected to primarily undergo narrow and weak consolidation.

PET: Polyester bottle chip market moves downward slightly

1 Today's Summary

Yisheng's basis remains stable, while other factories have lowered prices by 20-70. (Unit: Yuan/ton)

②. Today's domestic polyester bottle chip capacity utilization rate is 73.37%.

2 Spot Overview

Today, the spot price of polyester bottle-grade PET in East China is 5660, down 20 from the previous working day, which is in line with the morning forecast.

The market sentiment is pessimistic, and raw materials continue to decline. Coupled with the lack of favorable factors supporting the supply and demand of polyester bottle chips, factory quotations have been reduced by 20-70. The market focus is shifting downwards, with some traders restocking, and demand-driven restocking at low prices. It is heard that October sources were traded at 5880-5760, mostly at lower prices, with some slightly higher at 5820. November sources were traded at 5580-5770, and December sources at 5560-5710. Futures contract 2511 saw a premium of 10-100, with the basis remaining stable. A major terminal manufacturer is conducting a tender. (Unit: RMB/ton)

3. Price Prediction

External negative news has emerged again, leading to a strong sense of pessimism in the commodity market. The polyester bottle chip market may continue to adjust on the weaker side. With supply remaining stable, it is expected that tomorrow the spot price of polyester bottle chips for water bottles in the East China region will operate in the range of 5,550-5,700 yuan/ton.

PBT: Market Watching Operation

1 Today's Summary

This week's PBT manufacturers' quotes remained stable overall.

② There are fewer PBT unit maintenance activities this week.

③ The PBT production for this period is 22,600 tons.The capacity utilization rate is 53.14%, remaining stable compared to the previous period. This week, the average gross profit of domestic PBT is -324 yuan/ton, a decrease of 58 yuan/ton compared to the previous period. 。

2 Spot Overview

The mainstream price of medium and low viscosity PBT resin in the East China region today is 7,450-7,750 yuan/ton, unchanged from the previous working day. Today, the PBT market is running cautiously, the PTA market continues to show weakness, and the BDO market is consolidating in narrow ranges. The support from the raw material side is generally weak, the PBT market is operating with a wait-and-see attitude, the negotiation focus is weak and stable, and trading activity is scarce. , According to Longzhong Information, the price of low-viscosity PBT pure resin in the East China market is between 7,450 and 7,750 yuan per ton.

3 Price Forecast

The PBT market is expected to operate weakly. On the raw material side, PTA plants are resuming operations after reducing load, leading to a slight increase in supply while supply and demand remain tightly balanced. However, the ongoing tariff disputes continue to ferment, and with oil prices weakening, the overall commodity trend is sluggish, spreading pessimism in the market. In the short term, the PTA spot market is expected to continue its weak trend. BDO currently has some support on the supply side, with suppliers stabilizing the market and limiting operational space, while downstream demand remains weak, resulting in a generally weak and stagnant market. With no significant fundamental factors to provide a boost, the PBT market sentiment is bearish, and transactions are likely to revolve around just-in-time needs. Therefore, Longzhong expects the East China market's low to medium viscosity PBT resin to be priced at 7,450-7,750 yuan/ton tomorrow.

POM: Limited fundamental support, flexible operation by operators.

1. Today's Summary

The Kaifeng Longyu POM unit will undergo maintenance from October 9 for approximately 20 days.

The Tianjin Bohua POM plant was shut down for maintenance on July 7th, and the restart date is yet to be determined.

2 Spot Overview

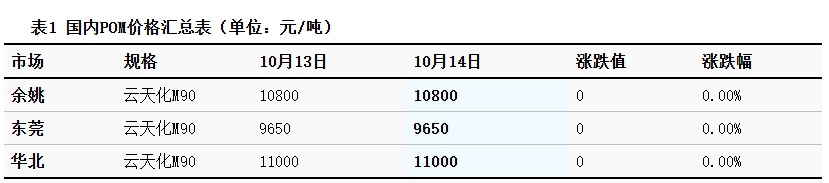

Based on the Yuyao region, today YunTianHua M90 is priced at 10,800 yuan/ton, with the price remaining stable compared to the previous period.Today, the POM market is weakly consolidating. The fundamentals are weak, the market sentiment is cautious, and there are no significant fluctuations in mainstream quotations. , End users are cautious in purchasing, and the market outlook remains pessimistic. As of the close, the domestic POM price in the Yuyao market is 8,100-11,100 yuan/ton (including tax), while in the Dongguan market, the cash price for POM is 7,300-10,400 yuan/ton.

3. Price Prediction

During the week, the shipment situation in various regions was poor, with limited guidance from petrochemical plants. The ex-factory prices remained stable, and the market inquiry atmosphere was weak. Traders were less enthusiastic about operating, maintaining a short-term bearish sentiment. Some offers had room for negotiation, while terminal factories operated at low load levels. Users followed up with sporadic replenishment, and transactions were conducted on a case-by-case basis.Longzhong expects that the short-term domestic POM market will run steadily.

PMMA: Trend remains stable

1 Today's Summary

①、 Today PMMA particles Market price stability 。

Today, the utilization rate of domestic PMMA particles remains at 60%.

2 Spot Overview

In the East China region, PMMA particles closed at 13,600 yuan/ton today, remaining stable compared to the previous working day, in line with the morning expectations. 。 The price center of MMA is weakening, with a wait-and-see attitude prevailing in the market. Most holders are reporting stable prices, while demand is relatively flat. Pre-holiday stocking sentiment is low, and actual transactions are limited.

3 Price prediction

The raw material market appears slightly sluggish, with moderate support from the cost side. The sentiment towards receiving goods on-site is not very positive, with holders offering prices according to market trends, and the speed of shipment is relatively slow. In the short term, PMMA particles remain stable and consolidated.

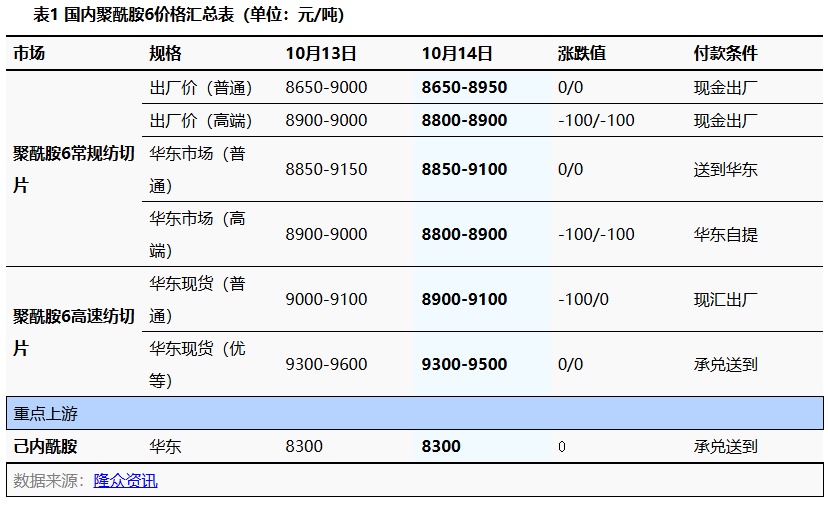

PA6: Multiple bearish factors in the market, PA6 market operates weakly.

1 Today's Summary

①、 Last week's settlement price for Sinopec caprolactam was 8,580 yuan per ton (six-month acceptance without interest).

②、 Sinopec's listed price of pure benzene is reduced by 100 RMB/ton to 5650 RMB/ton, effective October 14th.

2 Spot Overview

Today, the nylon 6 market is running weakly, with multiple bearish factors. The raw material market is consolidating weakly, and cost support is limited. The downstream demand is limited, and the purchase of raw materials is relatively cautious. Manufacturers are slow in selling, frequently offering low-priced slices, with actual transactions being negotiated. East PA6 conventional spinning ordinary price is 8,850-9,100 RMB/ton cash for short delivery, high-speed spinning spot price is 9,300-9,500 RMB/ton with acceptance delivery. Chao Lake price is 8,250-8,350 RMB/ton cash for self-pickup.

3 Price Prediction

From the cost perspective, the caprolactam market is running weakly, with diminished expectations for cost support. In terms of supply and demand, domestic polymer enterprises are operating steadily, with stable supply; however, downstream terminal orders are generally limited in demand. It is expected that the PA6 market will continue to run weakly in the near term.

PA66: The market spot supply is stable, and the market is operating steadily.

1 Today's Summary

①, 10/13: The U.S. softened its rhetoric on tariff increases, combined with the ongoing Russia-Ukraine conflict posing potential supply risks, leading to a rise in international oil prices. NYMEX crude oil futures for the November contract increased by $0.59 to $59.49 per barrel, a week-on-week increase of +1.00%; ICE Brent crude futures for the December contract rose by $0.59 to $63.32 per barrel, a week-on-week increase of +0.94%. China's INE crude oil futures for the December 2512 contract fell by 14.8 to 453.7 yuan per barrel, and increased by 0.1 to 453.8 yuan per barrel during the night session.

As of today, the domestic PA66 capacity utilization rate is 65%, with a daily output of approximately 2,550 tons. Some enterprises have increased their capacity utilization rates, while the downstream demand remains average. New capacities are being gradually released, resulting in a sufficient supply of goods in the domestic PA66 industry.

2 Spot Overview

Based on the Yuyao market in the East China region, today's EPR27 market price is referenced at 14,800-14,900 yuan/ton, stable compared to yesterday's price. 。 Downstream demand is weak, market spot supply is ample, raw material prices are fluctuating, resulting in significant cost pressure, and the market is undergoing adjustment.

3 Price Prediction

The cost pressure is relatively high, the market has ample spot supply, but the demand side is performing generally. The industry sentiment is cautious, and the domestic PA66 market is expected to consolidate weakly in the short term.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)