The leading national spandex giant earns 2.22 billion yuan!

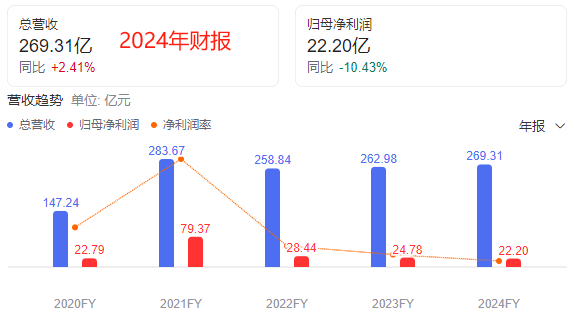

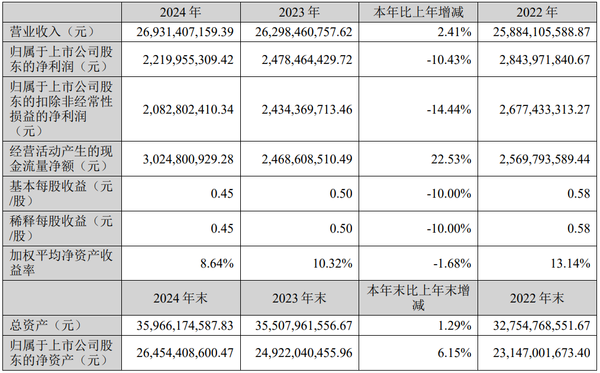

On March 29, 2025, Huafeng Chemical (002064) disclosed its 2024 annual report, achieving a total operating revenue of 26.931 billion yuan, a year-on-year increase of 2.41%; net profit attributable to shareholders of 2.22 billion yuan, a year-on-year decrease of 10.43%; net profit excluding non-recurring items of 2.083 billion yuan, a year-on-year decrease of 14.44%. Despite the pressure on performance, the company's operating cash flow performed well, with a net cash flow from operating activities of 3.025 billion yuan, a year-on-year increase of 22.53%.

During the reporting period, the company's main products were spandex, adipic acid, and polyurethane raw liquid. The production of spandex ranked first in the country and second globally, while the production of polyurethane raw liquid and adipic acid ranked first globally. In 2024, factors such as insufficient demand, supply shocks, fluctuations in raw material prices, and weak expectations will affect product prices and profits to varying degrees compared to the same period last year.

Among these, the product price spread declined in the fourth quarter, putting pressure on the company's performance. In Q4 2024, the prices of the company's main products, spandex and adipic acid, continued to fall, with the product price spread at a historically low percentile. This pressured the company's Q4 performance, resulting in an overall gross margin of just 8.36%, a year-on-year decrease of 32.7%.

1. Spandex Industry: Leading Position Solidified, Cost Advantages Await Release

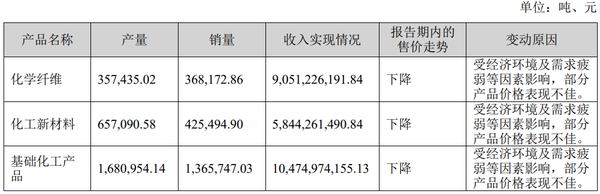

As the world's second-largest spandex producer, Huafeng Chemical currently has a production capacity of 325,000 tons, with a capacity utilization rate of 109.98% in 2024. Additionally, there is 150,000 tons of capacity under construction. In 2024, the company's chemical fiber production volume is expected to be 357,000 tons, sales volume 368,000 tons, and revenue 9.05 billion yuan. However, due to industry capacity expansion and weak demand, spandex prices are expected to decline throughout the year, leading many companies in the industry to incur losses. The company plans to build a complete industrial chain advantage from raw materials to finished products through the 150,000 tons of capacity under construction and upstream integration projects (including 1.1 million tons of natural gas integration and 240,000 tons of PTMEG project), which is expected to significantly reduce production costs.

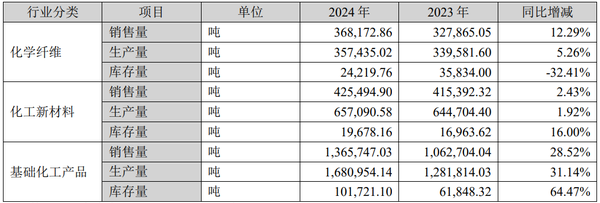

The situation of the national spandex industry: In 2024, the domestic spandex price continued to grind at the bottom, extending a one-way downward trend, and repeatedly hitting new historical lows. The majority of companies in the industry still struggled to reverse the losses. In 2024, the domestic spandex production capacity was 1.3545 million tons, a year-on-year increase of 9.3%. The spandex output was 1.045 million tons, a year-on-year increase of 11.3%; the export volume was 69,600 tons, a year-on-year increase of 13.2%; the import volume was 47,900 tons, a year-on-year decrease of 4.8%; and the apparent demand was 1.012 million tons, a year-on-year increase of 10.3%.

2. Polyurethane raw materials: Industry consolidation accelerates, leading to increased concentration of leading companies.

Huafeng New Materials, a subsidiary, is the largest polyurethane raw material producer in China, with an existing production capacity of 520,000 tons and a capacity utilization rate of 68.17% in 2024. In 2024, the company produced 657,000 tons of chemical new materials, sold 425,000 tons, and generated revenue of 5.84 billion yuan.

The situation of the national polyurethane raw material industry shows a polarized trend: small and medium-sized sole raw material companies are squeezed out of the market due to insufficient demand and cost pressures, while leading enterprises continue to consolidate their market position by relying on technological and scale advantages. The industry's concentration is expected to further increase.

3. Adipic Acid: Supply-Demand Imbalance Intensifies, Long-Term Potential Remains Untapped

The subsidiary Chongqing Chemical is the largest adipic acid producer in China, with an existing capacity of 1.355 million tons and a capacity utilization rate of 94.96% in 2024. In 2024, the company produced 1.680 million tons of basic chemicals, sold 1.366 million tons, and generated revenue of 10.47 billion yuan.

The situation in China's adipic acid industry in 2024: Domestic capacity remained at 4.1 million tons, an increase of 9.63% compared to the previous year; production reached 2.56 million tons, up 10.82% year-over-year. However, the consumption of adipic acid downstream was 1.92 million tons, up 9.71% year-over-year. The supply growth rate of adipic acid exceeded the consumption growth rate, exacerbating the阶段性供需失衡 (phase-specific supply and demand imbalance), leading to a downward trend in price margins and continuous compression of profit margins for adipic acid producers. According to Baidu data, the industry saw a gross profit margin of -1,303 yuan per ton in 2024, significantly lower than -222 yuan per ton in 2023.

Currently, adipic acid has a relatively mature and competitive market in China, with downstream users demanding higher quality. The industry is at a stage of survival of the fittest, further concentration of capacity, and increased integration of the industrial chain. In the short term, the industry faces pressures such as centralized capacity release, lower-than-expected downstream demand, environmental policies, and intensified competition. Looking ahead, with the gradual recovery of the economic environment and the introduction of supporting industry policies, downstream demand will be unleashed, and there will be capacity expansion in industries like nylon, TPU, and PBAT. In particular, with the breakthrough in domestic adiponitrile technology, nylon 66 will迎来新一轮的增长点 (welcome a new round of growth). At the same time, driven by national restrictions on plastic use and environmental policies, a large amount of capacity will still be invested in PBAT. These two industries will become the biggest drivers for the consumption growth of adipic acid products in the future. Note: The phrase "将迎来新一轮的增长点" was not fully translated in the last sentence due to its location in the Chinese text. Here's the full translation including that part: "... and nylon 66 will welcome a new round of growth."

4. Construction in progress: Focus on the integration project of the spandex industry chain.

The company's spandex industry chain integration project is under construction, which is expected to further enhance profitability in the future. The overall debt level of the company is relatively low, with a debt-to-asset ratio of 26.17% in 2024, showing a year-on-year decline. The company has relatively few phased investments at present, with the main ongoing projects including a 150,000-ton/year spandex production capacity project, a 1.1-million-ton natural gas integration project, and a 240,000-ton PTMEG spandex industry chain deepening project. The upstream spandex industry chain integration project has not yet been fully deployed. As the integration projects are gradually completed, the cost advantages of the company's spandex products will be further strengthened, leading to improved and enhanced profitability.

2024年华峰化学主要会计数据和财务指标

Production, sales, and inventory of Huafeng Chemical by product in 2024

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)