Specialty Engineering Plastics PPS Sector Heats Up: Why Are Giants Like Wanhua Chemical Rushing In?

Recently, the polyphenylene sulfide (PPS) industry has been dynamic, attracting widespread market attention. In September 2025, Wanhua Chemical announced a patent for the preparation of PPS resin, focusing on molecular weight control and end-group ratio optimization, significantly enhancing the material's processing performance and reactivity with silane coupling agents. This is the second related patent the company has released this year; back in April, it announced a technology aimed at reducing the generation of oligomer waste during the polymerization process.

Source: Chemical New Materials

Almost simultaneously, at the end of August, Huangshan Dongtai Qixin Technology Co., Ltd. announced the official commencement of its annual 80,000-ton PPS resin project. With a total investment of 1.6 billion yuan, the project is expected to achieve an annual output value of 4 billion yuan after production begins, and is poised to become one of the leading domestic producers of PPS monomers.

01 PPSCore materials of high-end manufacturing.

PPS, or polyphenylene sulfide, is a high-performance thermoplastic resin composed of alternating benzene rings and sulfur atoms, with a well-ordered molecular structure and a crystallinity of up to 75%. Its melting point is approximately 285°C. This material possesses several excellent properties: high mechanical strength, resistance to high temperatures, chemical corrosion resistance, good flame retardancy, outstanding electrical performance, and thermal stability. Therefore, it has become an irreplaceable strategic material in many high-end manufacturing fields.

Its application scope is extremely broad. For example, the automotive industry utilizes PPS to achieve lightweight designs, applying it to engine peripheral components and battery systems for new energy vehicles. In the electronics and electrical sector, it is used in 5G communication equipment, high-frequency connectors, and insulation components. In terms of environmental protection, PPS fibers are employed as industrial filter bags in high-temperature and corrosive environments. In addition, it is widely used in aerospace, military equipment, and medical devices.

The figure shows Xinhua Cheng's low ash content cross-linked PPS resin product (Image source: Xinhua Cheng)

02 PPSMarket Landscape: Intensified Competition Among Domestic and Foreign Enterprises

Currently, global PPS production capacity remains concentrated in the hands of a few international giants, including Japan's DIC, Kureha, Toray, and Belgium's Solvay. These companies have significant advantages in continuous production, process stability, and the development of high-end grades. In contrast, although the domestic industry started early, there was insufficient early-stage technological accumulation, and large-scale development has only been achieved in the past five years.

As of 2024, there are a total of 11 PPS resin manufacturers nationwide, with a total nominal production capacity of 92,000 tons per year, an effective capacity of approximately 68,000 tons per year, and an actual output of nearly 50,000 tons.

In line with global trends, the concentration of the PPS industry in China is also high. Five companies—Zhejiang NHU, Chongqing Lion, Tongling Ruijia, Zhongtai Xinxin, and Binhua Group—account for 91% of the total effective production capacity. As the leading company, Zhejiang NHU currently has a production capacity of 22,000 tons per year, consistently operating at full capacity and planning further expansion.

03 PPS Capacity Expansion: List of Projects Under Construction and Planned

In terms of capacity expansion, by June 2025, the total planned and under-construction PPS projects in China will have a total capacity of approximately 250,000 tons per year. However, most of these projects are still in the early stages, and it is expected that few will actually be realized. For example, Shengji New Materials' first phase of a 30,000-ton facility will be put into operation in the second half of 2025, Xinjiang Jufang Gaoke's production line technology upgrade is expected to be completed in October, and Mingquan New Materials' second phase is planned to be completed in 2027.

By the end of 2025, China's total PPS production capacity is expected to reach 129,000 tons, showing significant growth compared to previous years. However, by 2030, the compound annual growth rate is projected to slow to 2.1%, with production capacity reaching 143,000 tons per year, and market competition is expected to become more rational.

Table: Planned Projects of China PPS (as of June 2025) Data Source: China Huaxin

04 Consumption Growth: Dual Drivers of New Energy Vehicles and Environmental Policies

The market demand continues to grow strongly. In 2024, the apparent domestic consumption of PPS resin reaches 56,000 tons, with a compound annual growth rate of 9.5%. Among this, the dependency on imports remains high, with approximately 30,000 tons needing to be imported from abroad. The self-sufficiency rate has not yet surpassed half, standing at only 46.4%.

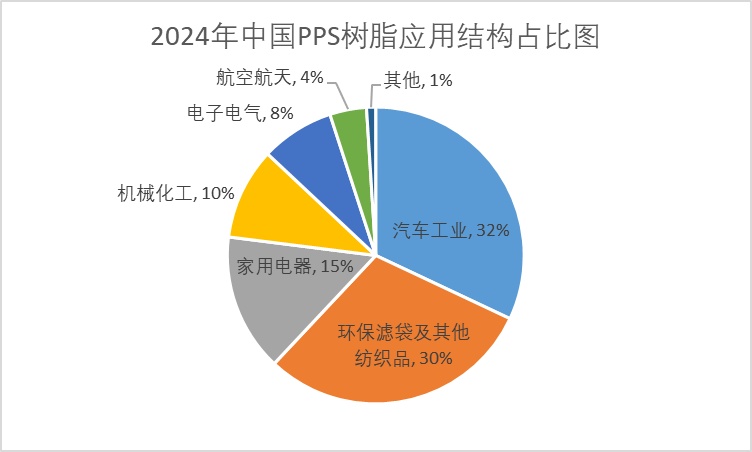

The main drivers of growth come from two aspects: the industrial environmental protection upgrade driven by the "dual carbon" policy (such as the application of high-temperature filter bags in the power and cement industries) and the demand for lightweight materials spurred by the boom in new energy vehicles. Currently, the automotive sector has become the largest consumer market for PPS, followed by environmental filter bags and household appliances.

Source of image: High Performance Resins and Applications

In terms of product types, injection molding grade, fiber grade, and extrusion grade PPS dominate the market. Fiber grade products are mostly used in eco-friendly textiles, while injection molding and extrusion grades are widely used in the automotive, electronics, machinery, and aviation sectors.

05 Future Prospects: Opportunities and Challenges Coexist

Looking ahead, China's PPS industry faces both opportunities and challenges. On one hand, domestic enterprises still lag behind international companies in high-end products, development of specialized materials, and production stability, especially encountering technical bottlenecks in continuous production control and byproduct treatment. On the other hand, with the ongoing expansion of the electronics, electrical, and new energy vehicle industries, the global supply-demand balance for PPS is becoming increasingly tight, presenting huge growth potential in the domestic market.

For enterprises such as Wanhua Chemical and other giants, the layout of PPS aligns with their strategies of high-end and green development. Although specific mass production plans have yet to be announced, the frequent release of patents and industry collaborations indicate that their commercialization process is steadily advancing.

In this context, whether domestic companies can break through technical barriers and enhance product competitiveness will be key to truly competing with international giants.

Edited by: Lily

Sources: High Performance Resins and Applications, Chemical New Materials, China Chemical Information, Special Plastics World, Sina Finance, etc.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)