Shanghai 12,000, Monthly Rise Nearly 3,000! LDPE Rises Then Falls in April, Expected to Remain Weak and Volatile in May

Entering the second quarter of 2026, the global polyolefin market is being driven by two main themes: on one hand, persistent ethylene shortages in Europe are supporting firm raw material prices; on the other hand, the temporary ceasefire in the Middle East has led to a rapid elimination of geopolitical risk premiums. Amid this interplay of factors, domestic LDPE prices exhibited a classic “sharp rise followed by a correction” pattern in April. Building on the current supply-demand dynamics, Specialized Plastics Insight has reviewed LDPE price movements in April and issued its outlook for May.

European ethylene supply is tight, and the shortage in April and May is unlikely to be relieved.

Zhuan Su View learned that, affected by regional cracking units' concentrated production restrictions, planned maintenance, and global supply chain disruptions,April–MayTight ethylene supply conditions in Europe are difficult to alleviate. Currently, near-term import procurement in Europe has largely stalled, and downstream plants and traders have postponed most cross-border inquiries, price negotiations, and purchases. Sailing schedule

In the next two months, there will be no resumption of production or new capacity additions for cracking facilities in Europe, and the shortage of raw materials will persist, providing long-term support to the global polyethylene market.

Image source: ai

Meanwhile, Middle East tensions briefly eased, raising expectations for improved navigation through the Strait of Hormuz, causing the crude oil "war premium" to dissipate sharply. As a result, cost-side dynamics shifted from a sharp rally to high-range consolidation, prompting a shift in LDPE's bullish rationale.

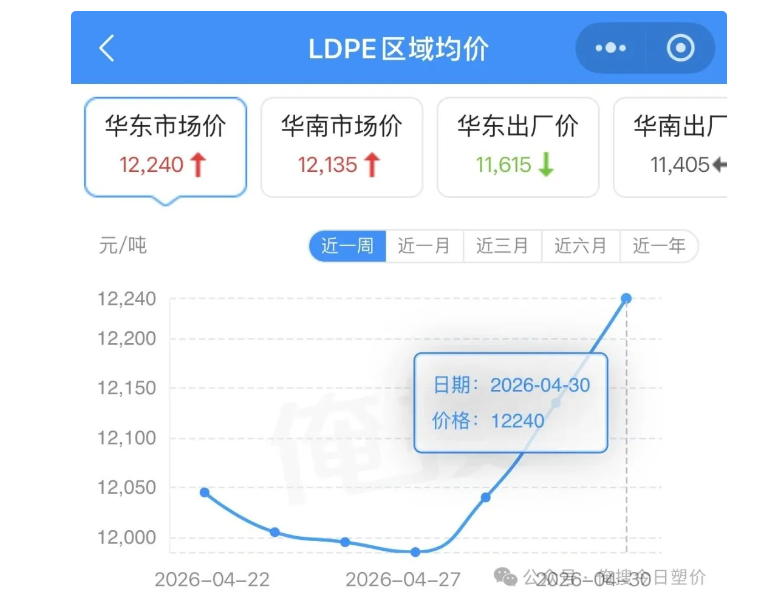

II. April LDPE: Surged to RMB 12,000 per ton—Monthly Gain Approaching RMB 3,000

According to NetEase Information data, LDPE experienced a strong upward trend in April, with the maximum increase of the month approaching.3000 RMB per tonDaqing Petrochemical 2426H from8650 yuan per ton 11,600 yuan/ton, increase34%As ofApril 30LDPE East China market priceRMB 12,240 per tonSouth China market price12135 yuan per ton。

Image source: Today's Plastic Price

This round of rise is mainly driven by three factors:

1. Crude oil costs remain strong, with international oil prices surging by over [X]% in a single day in early March.8%Brent breaks through$100 per barrelEpic support from the cost side;

2. Imported supply has contracted, as Iran—a major PE exporter—has seen declining plant operating rates and disrupted logistics, leading to a continued decline in domestic LDPE imports.

3. Europe is facing a shortage of ethylene, leading to a tight global supply situation. Downstream companies are locking in purchases, driving up spot prices. However, by mid-April, the market reversed sharply. According to Sumei Technology monitoring, the mainstream transaction price of LDPE melt index 2 film material in domestic markets has declined.$344 per ton 11407 yuan per ton, decline2.93%The market has shifted from a "frenzied surge" into a rational correction.

III. Why Has the Rally Stopped? The Fundamental Supply and Demand Picture Takes Over Again

In late April, LDPE prices fell, mainly due to weakened geopolitical impacts and a more relaxed domestic supply and demand situation.

On the supply side, driven by high profit margins, domestic LDPE units have maintained high operating rates, with weekly output remaining elevated.83,200 metric tons, higher than the annual average, with ample spot supply effectively making up for the decrease in imports.

On the demand side, the downstream sector entered the traditional off-season in April, with agricultural film demand entering the off-season, orders significantly shrinking, and new orders for packaging films being weak. The operating rate of the downstream products industry is only35.90%It declined month-on-month; insufficient demand combined with cautious pre-holiday stockpiling led to increasing inventory, and prices lost sustained upward momentum.

Image source: AI

IV. LDPE Price Outlook for May: Weak at High Levels, with a Downward Shift in the Price Center

Comprehensively considering key variables such as European ethylene supply, plant maintenance schedules, and seasonal demand fluctuations, Zhuan Su Shi Jie forecasts that LDPE prices in China will continue to trend weakly at relatively high levels in May, with the price center experiencing a slight downward adjustment. On the supply side, planned maintenance shutdowns at plants—including Yangzi BASF and Wanhua Chemical—will lead to a modest decline in domestic LDPE output in May; meanwhile, import volumes continue to contract, resulting in a temporary easing of supply pressure—though overall supply remains ample. On the demand side, the downstream off-season persists in May, with insufficient orders for agricultural films and packaging films; end-users are operating with low inventories and placing only small, just-in-time orders, making a concentrated restocking rally unlikely—thus demand is insufficient to support prices. On the cost front, the temporary ceasefire in the Middle East is exerting downward pressure on oil prices; however, the tight ethylene supply in Europe remains unchanged, and the crude oil price floor has risen, limiting LDPE’s downside potential. According to Longzhong Information, the mainstream domestic LDPE transaction prices in May are highly likely to decline to…11000 yuan/tonNearby, it is showing a "high-level fluctuation and weak consolidation" pattern.

V. Summary

In the short term, the domestic LDPE market will remain in a balanced state characterized by "limited external support and internal supply-demand pressure." Attention should focus on three key variables: the restart progress of European ethylene plants and the arrival of June seaborne cargoes, which directly affect global feedstock support; developments in Middle Eastern negotiations and fluctuations in international crude oil prices, which determine the strength of cost-floor support; and the actual impact of domestic plant maintenance schedules and the pace of downstream order recovery, which will dictate the direction of supply-demand dynamics. Operationally, downstream users should adhere to just-in-time procurement and rapid turnover principles to mitigate downside price risks and avoid chasing high prices. Traders should maintain light inventories, manage stock levels prudently, and refrain from accumulating high-cost inventory to prevent losses. In the medium to long term, against the backdrop of global polyolefin supply chain restructuring, integrated domestic refining and petrochemical enterprises will continue to demonstrate enhanced competitiveness through their complete industrial chains, underpinning LDPE prices at relatively high levels. However, market volatility is expected to gradually narrow, with prices returning to a reasonable range primarily driven by fundamental supply-demand dynamics.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Continental Plans to Begin Sale of ContiTech in Early 2026

-

$4 Billion! Medtronic Makes Another Acquisition

-

BASF Delivers First Batch of Innovative Cathode Materials for Semi-Solid-State Batteries to Weilan New Energy

-

Profit and Revenue Growth Struggle to Conceal Debt Repayment Pressure; Success of Kingfa Sci & Tech's High-End Strategy Yet to Be Seen

-

Why did a century-old european dental instrument giant relocate its manufacturing hub to china?