Reduced Output Intensifies; Polyester Staple Fiber Faces Challenges in Maintaining Prices

Since the second quarter of 2026, the polyester filament market has been experiencing a deep confrontation triggered by active supply-side contraction. Faced with the dual challenges of continuously rising inventory pressure and weak downstream demand recovery, major polyester filament producers have further increased their production cuts at the end of the previous weekend, aiming to tighten the supply side to slow down the downward trend of product prices. As of April 20, the industry has entered a substantive production cut phase. It remains uncertain whether this "price protection" measure can achieve the expected effect in a weak demand environment.

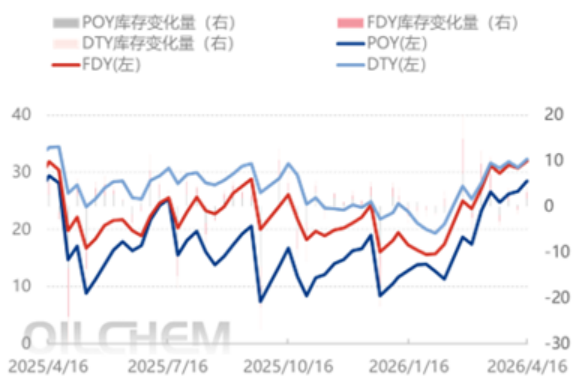

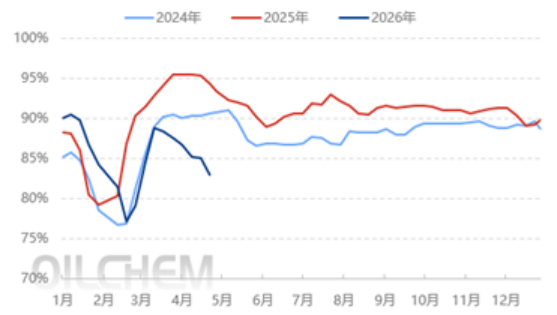

According to the latest data, although supply contraction has begun, the imbalance between supply and demand has not yet seen substantive relief. As of April 20, the average operating rate of polyester filament producers declined to 86.2%, down 1% month-on-month, indicating that some producers have started implementing production cuts. However, this operating rate remains relatively high, reflecting significant divergence in the extent of production cuts among enterprises of different scales. Meanwhile, inventory pressure remains pronounced. In the second week of April, industry inventory levels stood at 26.7 days for POY, 30.7 days for FDY, and 30.9 days for DTY, with POY inventories continuing to rise slightly on a month-on-month basis. Elevated inventory levels are not only intensifying producers' capital tie-up and storage costs but also serving as a key driver compelling them to prioritize price stability over discount-driven sales.

Domestic Direct-Spun Polyester Filament Industry Sample Inventory Weekly Trend Chart (Days)

Trend Chart of Domestic Polyester Filament Capacity Utilization from 2024 to 2026

While the effects of supply-side adjustments remain unclear, volatile cost fluctuations have further added external uncertainties to this round of price maintenance efforts. In the past week, the energy and chemical market experienced a collective decline. On April 17, affected by the easing of geopolitical tensions and macroeconomic sentiment disturbances, Shanghai crude oil and low sulfur fuel oil fell by more than 5% each, PX and ethylene glycol dropped over 3%, and PTA also fell by more than 2%. The rapid decline in raw material costs significantly weakened the cost support for polyester staple fibers, making the manufacturers' pricing efforts increasingly similar to "counter-cyclical adjustments." As of April 20, the PX benchmark price has fallen to 9,600 yuan/ton, a decrease of 1.03% from the beginning of the month. The downward shift in the cost base has further strengthened the wait-and-see attitude of downstream enterprises, and their resistance to high-priced polyester fibers has intensified.

Meanwhile, insufficient follow-through in end-demand has become the key bottleneck constraining price transmission. Although operating rates of weaving machines in Jiangsu and Zhejiang have modestly rebounded to 53.1%, up 3.2% month-over-month, they remain 4.3% lower than the same period last year, indicating that the recovery pace of downstream textile demand remains sluggish overall. More critically, weaving mills continue to exhibit weak willingness to purchase raw materials, with raw material inventory levels hovering around a low of approximately 9.9 days, reflecting a cautious procurement strategy across the downstream sector focused primarily on meeting immediate needs while gradually drawing down earlier stockpiles. In terms of actual transaction activity, the overall sales-to-production ratio for polyester filament yarn stood at only 20%–30% on April 17, with some localized price negotiations already showing signs of softening. By April 20, market sentiment among producers had further diverged: after proactively lowering quotations, lower-end transactions in Zhejiang saw some modest improvement, yet the average sales-to-production ratio recovered merely to 40%–50%. This reactive "trading price for volume" adjustment underscores that, in an environment of inelastic demand, the strategy of cutting production to support prices is facing severe practical challenges.

Overall, the current deep production cuts in the polyester filament yarn industry are more of a defensive self-rescue by companies under the dual pressures of high inventory and weak demand. In a macro environment characterized by sharp fluctuations in the cost side and persistently low procurement willingness from the downstream, whether the contraction in the supply side can truly stabilize the price center remains to be verified. Moving forward, it is crucial to closely monitor the implementation strength of production cuts by leading companies, the marginal changes in raw material prices, and whether there are substantial signs of recovery in terminal textile orders.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Continental Plans to Begin Sale of ContiTech in Early 2026

-

$4 Billion! Medtronic Makes Another Acquisition

-

BASF Delivers First Batch of Innovative Cathode Materials for Semi-Solid-State Batteries to Weilan New Energy

-

Profit and Revenue Growth Struggle to Conceal Debt Repayment Pressure; Success of Kingfa Sci & Tech's High-End Strategy Yet to Be Seen

-

Why did a century-old european dental instrument giant relocate its manufacturing hub to china?