【PVC Weekly Outlook】Macro expectations remain highly uncertain, with the market expected to maintain weak volatility today.

One, Focus Areas

1. 3/28: Market concerns about the U.S. increasing tariffs and enhancing trade risks may lead to a global economic recession, causing international oil prices to fall. NYMEXCrude Oil FuturesThe May contract fell to $69.36, down $0.56 per barrel, with a sequential decrease of -0.80%; ICE Brent futures for May fell to $73.63, down $0.40 per barrel, with a sequential decrease of -0.54%. China's INE crude oil futures main contract for May fell by 1.7 to 541.7 yuan per barrel, and during the overnight session, it fell by 3.7 to 538 yuan per barrel.

2. Calcium Carbide: As of last Friday, the mainstream trading price in the Wuhai region remained stable at 2,700 yuan/ton, with smooth shipments from production enterprises. Procurement in the Sichuan region has gradually recovered, leading to increased regional demand. In the Wumeng area, rain and snow have caused road transport disruptions, exacerbating regional supply shortages. The situation is expected to continue today.Calcium carbide marketSteady adjustment and operation, with enhanced regional performance.

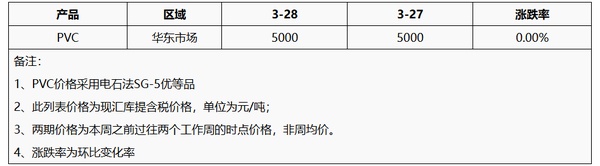

3, PVC: Last week, domesticPVC marketThe prices have shown a trend of rising followed by a decline, with the main driver still being the macro sentiment. However, the fundamental improvement in PVC is limited, and there is insufficient momentum for sustained market increases, leading to price consolidation after the rise. During the week, production fluctuations due to upstream company maintenance and load variations were not significant. Domestic demand was lukewarm, while foreign trade inquiry atmosphere was slightly better, with concentrated delivery of export orders in the market. As of March 28, the华东region's electricity method Type I prices ranged between 4900-5050 yuan/ton for spot cash warehouse withdrawal, while the ethylene method was between 5000-5200 yuan/ton.

II. Price List

Market Outlook

This week, the number of maintenance shutdowns in PVC production plants remains low, and with the resumption of operations at plants that underwent maintenance last week, market supply is expected to increase. Domestic downstream demand is primarily driven by rigid needs, putting pressure on domestic supply-demand dynamics. Foreign trade is focused on fulfilling previous orders, which somewhat alleviates inventory pressure on the industry. Macroeconomic expectations remain highly uncertain, particularly regarding global tariff policies. The market is anticipated to maintain a weak and fluctuating trend today.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)