[PP Weekly Review] Market Consolidates After This Week's Decline, Expected to Show Weak Narrow Adjustments Next Week

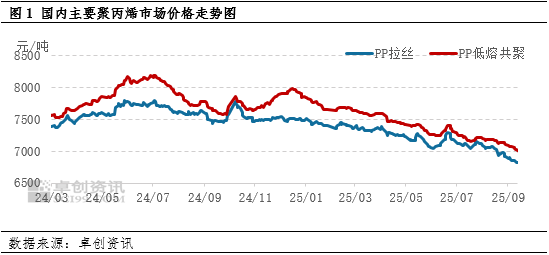

1Market Review: This week, the market declined and then consolidated, with the price focus continuing to slide.

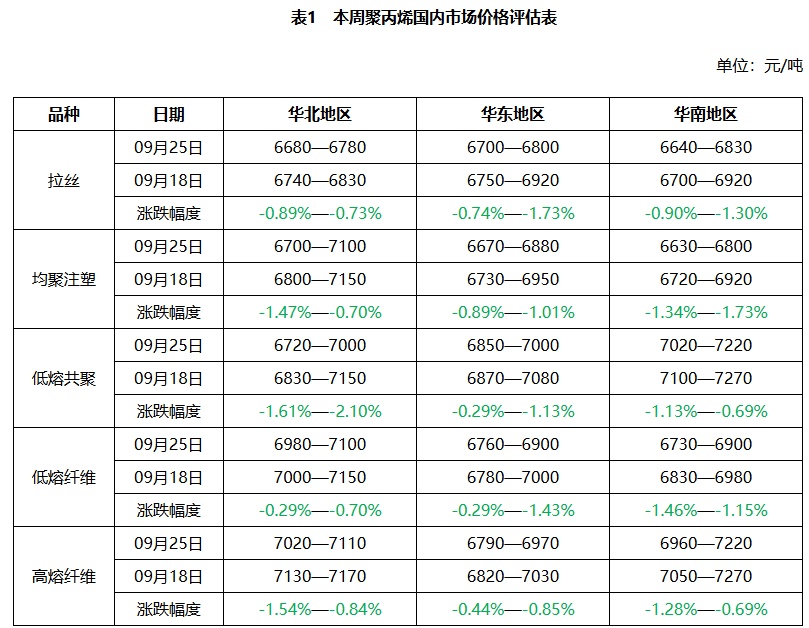

This week's domestic PP marketAfter the decline, there has been a consolidation, and the price center continues to move downward.As of this Thursday, the average weekly price of East China spinning is 6,773 yuan/ton, down 57 yuan/ton from last week, with a decrease of 0.83%. The regional price difference for spinning has slightly narrowed. In terms of types, due to insufficient support from fundamentals, the low-melt copolymer has a larger decline than spinning, and the price difference between the two continues to narrow.

2Market Outlook: As the National Day holiday approaches, there is insufficient fundamental support.

It is expected that the PP market will undergo weak consolidation next week. Taking East China as an example, it is anticipated that the price range for wire drawing will be between 6680-6800 yuan/ton, with an average price of 6760 yuan/ton. The price range for low-melt copolymer is expected to be between 6830-7000 yuan/ton, with an average price of 6910 yuan/ton.On the cost side, crude oil is expected to fluctuate mainly, providing limited guidance for PP. On the supply side, there will be no new capacity impact next week, but the number of maintenance facilities is expected to decrease, leading to a slight increase in supply. On the demand side, with the holiday approaching next week, most downstream entities have already completed pre-holiday purchases and are expected to mainly observe, making demand unlikely to provide support. Regarding inventory, production companies and traders are primarily focused on aggressive promotions to reduce inventory before the holiday, which is expected to weaken market support. Overall, the support from supply and demand fundamentals in the market next week is expected to be weak, with prices anticipated to adjust narrowly on the downside.

Supply:The maintenance of equipment is expected to decrease, while supply will increase slightly.Next week, there will be no impact from newly added production capacity. In terms of plant maintenance, there are no scheduled new maintenance units next week, and some existing maintenance units are expected to restart. The overall intensity of plant maintenance is expected to weaken, with an anticipated loss of 161,300 tons next week, a decrease of 18.12% compared to the previous week. Overall, supply is expected to increase next week. Regarding inventory, considering the increased inventory pressure after the holiday, production companies are primarily focusing on actively shipping before the holiday, and inventory is expected to slightly decline. For traders' inventory, on one hand, they need to prepare for the planned volume during the holiday period, and on the other hand, as the holiday approaches, downstream purchasing is gradually completing, increasing the resistance to traders' shipments. Therefore, inventory is expected to increase next week. For port inventory, domestic prices remain low, and the domestic and international markets continue to be inverted. Coupled with ample domestic supply, PP imports are limited. On the export side, overseas demand limitations restrict the growth of PP exports. Overall, PP port inventory is expected to remain relatively unchanged next week, around 39,000-40,000 tons.

Demand: Complete stocking in advance before the holiday, short-term demand is weak.Currently, the follow-up on new orders from downstream remains relatively limited. Recently, raw material prices have been hovering at low levels. After a slight recovery in downstream profits, there has been increased market participation to complete pre-holiday stockpiling. With the holiday approaching next week, the festive atmosphere in the market is gradually intensifying, and downstream purchasing enthusiasm is expected to weaken, leading to weak demand.

Cost:Next week, the average price of West Texas Intermediate crude oil is expected to be $64 per barrel, with a fluctuation range of $62 to $65 per barrel.Ukraine frequently attacks refineries within a certain European country's territory, causing it to restrict the export of oil products. Meanwhile, former U.S. President Trump openly calls on this European country, urging European nations to stop importing oil from it and completely eliminate their energy dependence on it. This situation poses a short-term risk of shifting global trade flows, although the risk of actual supply disruption remains low. Addressing the Middle East situation, the U.S. demands that Israel refrain from annexing the West Bank and calls for peace talks with Saudi Arabia, Qatar, and others, thereby reducing the risk of escalation. Consequently, geopolitical disturbances are providing support to oil prices, but cooling expectations exist, suggesting that oil prices may experience a fluctuating trend. From a risk perspective, the key concerns are the escalation of the Russia-Ukraine situation and the subsiding Middle Eastern geopolitical tensions. Crude oil is expected to mainly fluctuate, providing limited guidance for PP costs.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)