Sinopec East China has comprehensively lowered its posted prices. Shanghai Petrochemical’s T300 and M800E, together with multiple injection molding grades from Zhenhai, were all reduced by RMB 100, and factory concessions have turned spot market sentiment bearish.

The industry repair scale has slightly expanded, with the proportion of parking rising to 31.45%. Multiple large units have concentrated on ramping up production, while several companies have shifted to non-wire-drawing grades, resulting in a significant reduction in daily wire-drawing output. In this period, supply still does not meet demand, but the gap between supply and demand has narrowed. In the next period, supply is expected to increase while demand declines, significantly weakening the support.

Spot PP raffia prices fell across all regions nationwide, with the largest declines in Northwest and South China, while BOPP prices also edged lower in tandem. Futures opened lower and continued to decline, and spot-futures basis levels in East China and North China narrowed simultaneously.

Propylene feedstock prices rose sharply, while PP powder weakened and industry capacity utilization edged down slightly. Intermediaries in the market are buying and selling quickly to hedge risks; downstream orders are insufficient and procurement remains cautious, so the market is under short-term downward pressure.

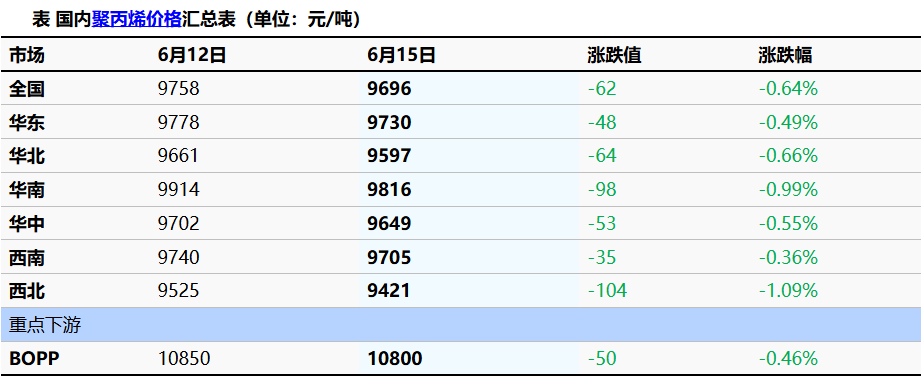

(1) Spot prices declined across all regions.

The national average price of raffia-grade PP was 9,696 yuan/mt, down 62 yuan on the day; the East China benchmark raffia-grade price was 9,730 yuan/mt, down 48 yuan. Regional divergence was evident, with Northwest China plunging by 104 yuan and South China falling by 98 yuan, while Southwest China saw the smallest decline at just 35 yuan. Downstream core BOPP prices were also lowered by 50 yuan to 10,800 yuan/mt.

Intraday futures opened lower and weakened, while spot prices generally fell by RMB 50-130 in the morning. In East China, the mainstream negotiation level for raffia was RMB 9,650-9,800/ton. As cost support weakened and demand remained sluggish, bearish sentiment in the market intensified. Downstream processors saw narrowing profit margins, slowed their purchasing pace, and actual spot transactions were difficult to expand, with only small orders driven by immediate needs changing hands.

(2) Synchronous narrowing of the spot-futures basis

The East China PP 09 contract basis was 1,094 yuan/ton, down 48 yuan month-on-month; the North China basis was 961 yuan/ton, down 64 yuan month-on-month. Spot prices followed the futures decline at a slower pace, while the previously high spot premium continued to narrow. Holders faced greater resistance in selling at high prices, and persistent weakness in the futures market continued to drag the spot price center lower.

Differentiation of upstream and downstream raw material price differences.

Shandong propylene prices surged sharply by RMB 755 to RMB 9,550, putting upward cost pressure on oil-based and PDH processes; methanol prices remained stable; Linyi PP powder prices were cut sharply by RMB 200 to RMB 9,370, with low-priced powder diverting orders from pellet materials and limiting the upside for pellet prices.

Industry capacity utilization stood at 63.95%, edging down by 0.10 percentage points. On the maintenance side, new shutdowns were seen at Luoyang Line 2, Qinghai Salt Lake, and Lihe Zhixin units, reducing daily output by 1,800 tons. On the supply side, Lianhong Line 2, Zhongjing Petrochemical, and Yulong Line 5 started up intensively, lifting overall daily output by 2,940 tons.

Production scheduling has shifted noticeably. Multiple units at Sinopec Shanghai Petrochemical, Sichuan Petrochemical, and Juzhengyuan have switched to producing transparent grades, low-MFR copolymer, and high-MFR fiber grades, resulting in a 2,850-ton reduction in daily raffia output. The contraction in raffia supply offsets part of the overall increase.

On the cyclical supply-demand side, during 6.5–6.11 the period remained undersupplied, but the decline in demand was greater than the decline in supply, causing the supply-demand gap to narrow. In the next period, supply increased while demand continued to weaken, further narrowing the supply-demand differential and gradually weakening price support.

Industry Profitability and Inventory Outlook

This week's data expectations indicate an increase in factory inventory, with slight declines in capacity utilization and total output. The processing profits of oil-based, coal-based, and PDH have all recovered and risen simultaneously, while export profits have seen a slight decline. Coal-based production continues to maintain high profitability and shows stronger resistance to downturns; oil-based and PDH processing profits have limited recovery space due to rising propylene prices.

Upstream refining and chemical companies are actively lowering prices to sell and replenish inventory; middlemen are adopting a low-inventory, quick turnover model, unwilling to stockpile and bear risks; downstream end-user orders are weak, processing plant profits are compressed, and there is a strong wait-and-see sentiment with price-cutting; overall, the market is predominantly bearish.

1. Overall Market Trend Forecast

In the short term, polypropylene is expected to maintain a weak downward trend.

Bearish factors: Sinopec’s large plants lowered ex-factory prices, leading market-wide price declines; supply–demand support for the next cycle has noticeably weakened; downstream demand is in the off-season, orders are insufficient and buying appetite is weak; the futures market remains weak and a narrowing basis is suppressing spot premiums.

Supporting factors: The industry's maintenance volume remains high, with a significant reduction in wire drawing production; the surge in propylene prices provides cost support, and there is currently no pressure to offload high-profit coal-based products; the increase in factory inventory is limited, posing no risk of large-scale accumulation.

Tomorrow, mainstream raffia prices in East China are expected to run at RMB 9,500-9,700/ton, with the intraday price focus continuing to move lower. Declines in Northwest and South China may still be larger than those in East China, while injection molding and copolymer grades are expected to follow raffia with slight price concessions.

If propylene and crude oil strengthen significantly again, the rise in costs may temporarily halt the decline; if downstream film and injection molding factories concentrate on restocking, an increase in transactions can alleviate the downward trend. This analysis is merely a logical deduction based on fundamentals and does not constitute trading or investment advice.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.