Polypropylene | Regional price spread narrows, industry competition intensifies

Changes in supply and demand patterns have narrowed regional price differences.

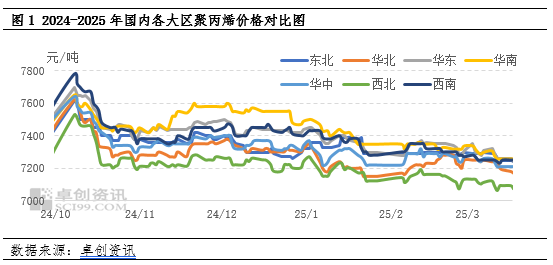

In March, the domestic PP market has shown weakness, with the price center moving downward and regional price spreads narrowing. According to data from Zhucu Information, apart from Northwest and North China regions where low-priced PP granular material still has a significant advantage, the price gap of low-priced PP granular material in other regions has narrowed. As of now, the price of low-priced PP granular material in the Northwest region is around 7,070 yuan per ton, while in the North China region it is around 7,170 yuan per ton. Other regions' low-priced PP granular material mostly ranges between 7,210-7,260 yuan per ton. The domestic PP prices are gradually becoming more consistent, which further increases the resistance to the outflow of resources within the region and intensifies the competitive landscape within the region.

Capacity base expands, regional production increases.

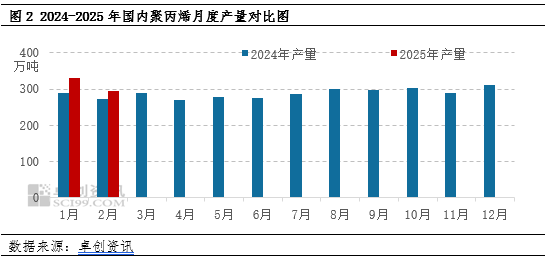

Against the backdrop of continuously increasing PP capacity at home, the supply volumes in various regions have all seen different degrees of increase, further intensifying the competitive landscape among regions. According to data from ZhuCE Info, in recent years, apart from the Southwest region, the production capacities in other domestic regions have all experienced varying degrees of growth. Among these, the North China, South China, and East China regions have seen particularly significant increases in production capacity. The expansion of production capacities across various regions has laid the groundwork for an increase in supply (the Southwest region mainly relies on nearby supplies from the Northwest region). As of now, China's total PP capacity has reached 44.32 million tons, with a notable increase in supply volume across various regions. In January and February 2025, the cumulative production of PP was 6.2376 million tons, an increase of 11.34% compared to the same period last year, with production in all regions being higher than the previous year. The relatively rapid increase in regional supply has also become a major factor driving downward pressure on regional prices.

Demand performance is weak, and regional competition is intensifying.

The poor demand performance has become a key factor driving the convergence of prices across different regions in the country. Entering March, which is traditionally the peak season for demand, the overall performance of PP (polypropylene) demand this year has fallen short of expectations. Affected by fluctuations in the international environment and domestic consumption downgrade, new orders from downstream sectors since the beginning of 2025 have been less than in previous years, with a slower procurement pace and weaker demand performance. Additionally, pre-sale货源提前点价导致需求被前置消耗,使得各大区现货资源消耗放缓。与此同时,各地区供应量呈现增长态势,在供需压力下,企业优先消化区域内需求,进一步加剧了区域内的竞争格局,这也是各大区拉丝价格趋向一致的关键因素。

Gross margins vary, and future supply will still face pressure.

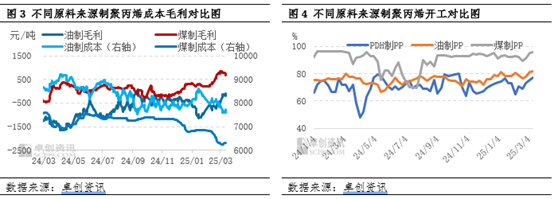

In the later stage, despite the basic fundamentals putting pressure on PP prices and leading to negative industry profit levels, some companies, especially those using coal-based production, still maintain relatively substantial profits and are actively producing. According to data from Zhushuang Information, as of now, most domestic PP enterprises across different raw material sources are experiencing gross profit losses. Specifically, oil-based PP is experiencing a loss of around 200 yuan per ton, PDH-based PP is facing a loss of approximately 400 yuan per ton, and both externally purchased propylene and externally purchased methanol-based PP are also suffering from losses. However, coal-based PP enterprises continue to maintain a gross profit margin of around 700 yuan per ton, which further boosts their production enthusiasm.

The operating load of coal-based PP has remained at a high level above 85%. Compared to this, the operating loads of PDH and oil-based PP are relatively lower. Especially for PDH-based PP producers, affected by the high prices of propane and low valuations of PP, some companies have reduced production loads, and there are also plans for some companies to undergo planned shutdowns for maintenance, resulting in generally lower operating loads for these facilities.

Overall, the short-term supply of PP is relatively limited due to maintenance of production units, and the supply in various regions is leaning towards abundance. However, April is a concentrated maintenance season for PP units, with several plants such as Qingdao Jineng Phase II, Jinan Refinery, and China National Chemical Corporation Tianjin planning to undergo lengthy maintenance. This is expected to further alleviate the pressure on the supply side.

Looking ahead, as the expectations for supply pressures gradually decrease, demand becomes the key influencing factor. In the short term, downstream recovery is relatively slow, but with the efforts of a large demand group, there are still positive expectations for downstream sectors such as daily necessities, packaging, and milk tea cups. Additionally, the domestic "old-for-new" policy will further boost domestic PP demand, along with the continued strength of PP exports. It is expected that the overall supply-demand pattern in the market will improve, gradually strengthening market support. The differences in supply and demand among various regions will once again lead to varying fluctuations in South China, North China, and East China, causing the price differences among these regions to widen again.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)