【Plastic Market Morning Update】Oil prices decline! PE and PP fluctuate, while PS and EVA slightly firm up.

Summary: Early morning market update for general plastics on April 2! Market focus shifts from oil-producing country sanctions to U.S. tariff policies, raising concerns about weakened demand prospects, leading to a decline in international oil prices. Limited marginal improvement in supply and demand keeps the PE market fluctuating; weak demand constrains price trends, with PP likely to consolidate within a range. Improved low-price transactions may lead to a slight uptick in PS market prices, while the PVC market remains range-bound. Rising prices in South China keep ABS prices in a narrow consolidation trend. Manufacturers are expected to continue supporting prices, with the EVA market likely to stabilize or consolidate.

PP:

One, Focus Areas

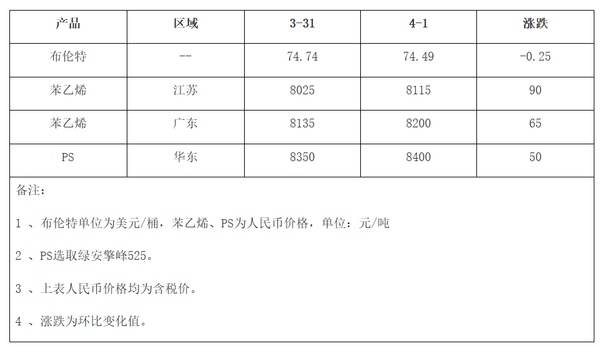

1. On April 1, market attention shifted from oil-producing country sanctions to concerns about US tariff policies, leading to worries about the impact on demand, resulting in a decline in international oil prices. NYMEX crude oil futures contract for May fell by $0.28 per barrel to $71.20, a decrease of -0.39%; ICE Brent crude oil futures contract for June also fell by $0.28 per barrel to $74.49, a decrease of -0.37%. China's INE crude oil futures主力contract for May rose by 11.6 to 549 yuan per barrel, with the night session rising by 4.3 to 553.3 yuan per barrel.

2、April 1: Propylene FOB Korea stabilizes at $800/ton, CFR China stabilizes at $825/ton.

On April 1st, the fifth line (300,000 tons/year) PP unit of Yulong Petrochemical restarted. The PP unit of Yan'an Energy (300,000 tons/year) was shut down for maintenance. The first line (70,000 tons/year) PP unit of Dushanzi Petrochemical was shut down for maintenance. The second line (140,000 tons/year) PP unit of Luoyang Petrochemical was shut down for maintenance. The first line (500,000 tons/year) PP unit of Inner Mongolia Baofeng was shut down for maintenance.

4. According to Lobang Information on April 1st, the two oil polyolefin inventory was 800,000 tons, an increase of 70,000 tons from the previous day.

Core logic:Downstream new orders follow-up is limited, and market action force is insufficient.

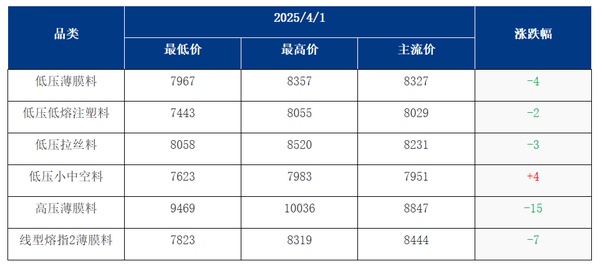

Price List

Three, Market Outlook

Recently, international oil prices have been relatively strong, providing ongoing cost support for PP. The number of maintenance shutdowns at upstream production facilities has increased, with the impact of stoppages rising by 18.72%. Coupled with the absence of new capacity additions in the short term, supply-side pressures have temporarily eased. Downstream factories have seen moderate new order follow-ups, with lackluster demand performance constraining price trends. It is expected that the polypropylene market may experience range-bound consolidation today.

PE

1. Points of Interest

1 Cost side:Market attention has shifted from production sanctions on oil-producing countries to the tariffs imposed by the United States, raising concerns that the demand outlook may be affected, leading to a decline in international oil prices. The NYMEX crude oil futures contract for May fell 0.28 USD per barrel to 71.20 USD, a decrease of 0.39%; the ICE Brent crude oil futures contract for June, which is in the process of rollover, fell 0.28 USD per barrel to 74.49 USD, a decrease of 0.37%.

2 Currently, the parking facilities involve 18 polyethylene units, with additional maintenance at Liaoyang Petrochemical, Daqing Petrochemical, and Sichuan Petrochemical units.

3 On the previous day, the domestic polyethylene market mostly declined, with a range of 2-15 yuan/ton. Spot supply was relatively abundant, downstream resistance to high prices persisted, and traders continued to offer slight discounts for shipments, creating a cautious atmosphere.

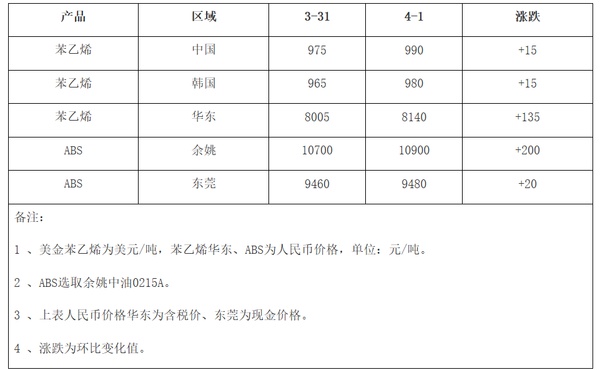

Price List

Three, Market Outlook

The increase in maintenance operations has led to continued price support upstream in the short term; downstream players are restocking based on pre-holiday essential demand, with market sentiment remaining cautious. In the short term, marginal improvements in supply and demand are limited, and the polyethylene market is expected to fluctuate.

PVC

ABS

One, Focus Areas

1 、 On April 1st, market attention shifted from oil-producing country sanctions to the U.S. tariff policy, raising concerns that demand prospects would be dragged down, leading to a decline in international oil prices. NYMEX crude oil futures for May contracts fell by $0.28 to $71.20 per barrel, a decrease of 0.39%; ICE Brent oil futures for June contracts fell by $0.28 to $74.49 per barrel, a decrease of 0.37%. In China, the INE crude oil futures main contract for May rose by 11.6 to 549 yuan per barrel, with a night session increase of 4.3 to 553.3 yuan per barrel.

III. Market Outlook

Yesterday, prices in the South China market rose, and prices in the East China market also increased. Terminal demand remained decent, with overall transactions booming. It is expected that today's market prices will maintain a narrow consolidation trend.

PS

One, Focus Areas

Raw material styrene has experienced a volatile rise, with stronger cost support. However, supply remains at a high level, and demand is not meeting expectations, resulting in an improvement in market sales at lower levels.

II. Price List

3. Market Outlook

The price of raw styrene has been volatile and increased, providing stronger cost support. However, with high supply levels and demand falling short of expectations, there has been some improvement in sales at lower price points. In the short term, the PS market prices may firm slightly. It is expected that the transparent改苯price in the East China market will be between 8,400 to 9,800 RMB per ton. (Note: "透明改苯" might refer to modified transparent polystyrene or another specific product; I've kept it as "transparent改苯" due to uncertainty about the exact context or product name.)

EVA

On April 1st, the market focus shifted from sanctions on oil-producing countries to the US tariff hike policy, with concerns that the demand outlook would be dragged down, leading to a fall in international oil prices. The NYMEX crude oil futures 05 contract dropped by $0.28 per barrel to 71.20, a decrease of 0.39% from the previous day. The ICE Brent crude oil futures switched to the 06 contract, falling by $0.28 per barrel to 74.49, a decrease of 0.37%. China's INE crude oil futures主力contract 2505 rose by 11.6 to 549 yuan per barrel, and the night session increased by 4.3 to 553.3 yuan per barrel.

Core Logic:On the cost side, ethylene and vinyl acetate are weak, reducing the support from the cost side. Some factories have switched to producing EVA foam material, which may add to the supply. Downstream foam demand is following a刚需 (mandatory) pattern, and market sentiment is becoming more relaxed. It is expected that the EVA market will likely remain weak.

Three, Market Outlook

In the short term, the domestic EVA market is expected to remain stable with some consolidation. The supply side is mostly focused on photovoltaic orders, and with the strong support from photovoltaic demand, EVA manufacturers will continue to maintain price stability. Downstream foaming demand remains steady, but transaction volumes are unlikely to increase significantly. Market participants are slightly panicked. It is expected that the domestic EVA market will mainly undergo weak consolidation. Mainstream market prices: hard materials will fluctuate between 11,200-11,600 yuan/ton, soft materials may fluctuate between 11,400-11,700 yuan/ton, and photovoltaic materials will fluctuate between 11,500-11,900 yuan/ton.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift