【PE Weekly Forecast】Downstream players continue to maintain basic inventory levels, it is expected that polyethylene prices will remain range-bound this week.

One, Focus Areas

1Cost side:Market concerns over U.S. tariff hikes increasing trade risks, potentially leading to a global economic recession, have caused international oil prices to fall. NYMEXCrude oil futuresThe May contract for West Texas Intermediate crude oil is at $69.36, down $0.56 per barrel, a decrease of 0.80% compared to the previous period; the May contract for ICE Brent crude oil futures is at $73.63, down $0.40 per barrel, a decrease of 0.54%.

2Currently available parking facilities:Currently, the parking devices involve 22 sets of polyethylene units, and there are no new device maintenance activities.

3Last week's market review:The domestic spot market price of polyethylene fell the previous day, with a decrease of 3-19 yuan/ton. Last week, market demand was limited, and end-users showed obvious resistance to high-priced resources, which restricted further price increases. Meanwhile, newly added production capacity was gradually being released, leading to a bearish market sentiment. Merchants maintained an active selling strategy, but trading remained weak.

Core logic: Spot prices are fluctuating.

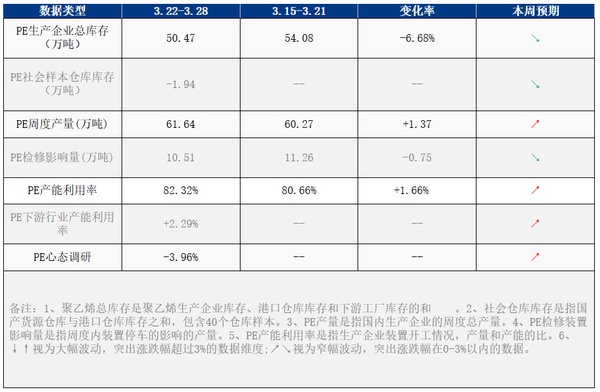

II. Price List

3. Market Outlook

From the perspective of the trend of the raw material end this week, it is expected that the support from oil-based costs will weaken, while the support from coal-based costs will remain largely unchanged. It is anticipated that the overall operating rate of various PE downstream industries will decrease by 0.02% this week. Although the consumer market has driven some short-term new orders, the gradual delivery of these short-term orders will reduce the support for production, potentially leading to a decline in the operating rate. In terms of supply, the restart of maintenance facilities at Sino-Korean Petrochemical, Liaoyang Petrochemical, Wanhua Chemical, and Yangzi Petrochemical is expected, along with planned maintenance at Qilu Petrochemical. The estimated impact of maintenance on production this week is 57,400 tons, a decrease of 47,700 tons compared to last week. The total production this week is expected to reach 649,300 tons, an increase of 32,900 tons from last week. Overall, although there will be an increase in maintenance on the supply side this week, newly commissioned companies will gradually enter normal production, and downstream sectors will continue to maintain necessary inventory preparation. It is expected that the price of polyethylene will continue to fluctuate this week.

IV. Data Calendar

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift