OPEC+ Production Increase Continues to Pressure Oil Prices Downward; Plastic Futures Main Contracts Mostly Rise

1. Overnight Crude Oil Market Dynamics

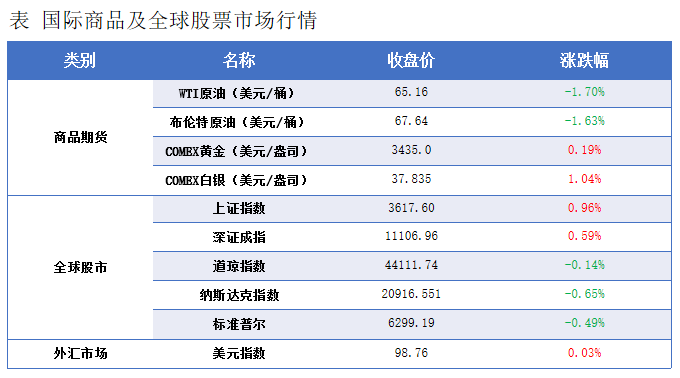

OPEC+ production increases continue to exert bearish pressure, and with geopolitical tensions temporarily easing, international oil prices have declined. NYMEXCrude oil futuresFor the September contract, the price is $65.16 per barrel, down by $1.13 or 1.70% month-on-month; ICE Brent crude futures for the October contract are at $67.64, down by $1.12 or 1.63% month-on-month. The main contract for China's INE crude oil futures, 2509, dropped by 7.7 to 509.1 yuan per barrel, with a night session decline of 6.6 to 502.5 yuan per barrel.

Future Market Forecast

On the 5th, U.S. President Trump mentioned in a speech that "if energy prices could drop another $10 per barrel, Putin would have no choice because his economy is already in bad shape. If the EU does not fulfill its obligations, a 35% tariff will be imposed on the EU. I am not worried about oil prices; India has the highest tariffs and will significantly increase tariffs on India within the next 24 hours." Trump's criticism of India's purchase of Russian oil has caused increasing tension in Indo-U.S. relations. Although the market widely expects India to be pressured to stop or reduce imports of Russian oil, India stated last week that regardless of what the U.S. says, it has no plans to stop purchasing Russian oil. The Kremlin is weighing concessions to U.S. President Trump, which may include reaching an aerial ceasefire agreement with Ukraine, in an attempt to avoid secondary sanctions. According to the latest news, President Trump stated that (the Middle East envoy) will meet with Russian representatives. It has not yet been determined whether tariffs will be imposed on Russia, and a decision on whether to sanction countries purchasing Russian energy will be made after the meeting on Wednesday. A 100% oil tariff is quite possible. However, from Monday's market trading trends, it seems more likely that the U.S. will not impose secondary sanctions on Russia, and the oil market has largely retracted the risk premium associated with sanction risks.

After OPEC+ firmly decided to accelerate production increases, the subsequent market supply pressure is a change that was anticipated. The market is already beginning to feel the impact of increased supply. On Tuesday, the Middle East crude oil spot benchmark prices declined, with Oman and Dubai crude prices falling to their lowest in over a month. The discounts have weakened significantly, and the spread structure continues to weaken, all of which point to a downward trend in oil prices. The seasonal support for oil prices from the demand side during the peak season is weakening. API data shows that crude oil inventory drawdown exceeded expectations last week, but the market seems too busy to pay attention. The raindrops formed two weeks ago have returned under the eaves, and ultimately the market needs to wait for the other shoe to drop. Will there be a headwind to change the trend this time? The answer is about to be revealed. Be sure to strengthen risk control and participate cautiously.

2. Macroeconomic Developments

◎Tariffs—①Trump: Announcement to be made next weekTariffs on pharmaceuticals and chipsThe tariff on pharmaceuticals can be as high as 250%. It will significantly increase within the next 24 hours.Increase Indian tariffs Failure to fulfill investment obligations in the U.S. will result in a 35% tariff. ② The U.S. trade balance for June recorded a deficit of $60.2 billion, the smallest since September 2023.

◎ The central bank and six other departments jointly issued guidance on financial support for new industrialization, adhering to differentiated policies and promoting advancement towards mid-to-high-end industries while preventing "involution" competition. The guidance specifies that by 2027, a mature financial system will be established to support the high-end, intelligent, and green development of the manufacturing industry, promoting the joint efforts of tools such as loans, bonds, and equity.

China has released an implementation plan for promoting a healthy environment, deploying comprehensive advancements in building a Beautiful China and Healthy China. The plan outlines six key actions and 16 specific measures, with a clear goal that by 2030, the compliance rate of residents' drinking water quality will continue to improve, and the level of environmental and health literacy among residents will reach 25% or above.

In June, the U.S. goods and services trade deficit shrank significantly by 16% month-on-month to $60.2 billion, marking the lowest level since September 2023. This was primarily due to companies cutting back on purchases after a large-scale import surge earlier in the year. The total value of imports fell by 3.7%, with consumer goods imports dropping to their lowest level since September 2020.

◎ The US ISM Non-Manufacturing Index for July fell to 50.1 from the previous 50.8, below the expected 51.5. New orders were nearly stagnant, employment contracted, and the price index reached its highest level since October 2022. In addition, the final S&P Global Services PMI for the US in July was 55.7, the highest since December 2024.

The final Eurozone composite PMI for July was 50.9, slightly up from 50.6 in June and reaching a four-month high, but below the initial estimate of 51. The composite PMIs of Spain, Italy, and Germany all showed growth, while France was the only major Eurozone economy to experience contraction.

3. Early Morning Update on the Plastic Market

International oil prices have fallen! Overnight, the main domestic plastic futures contracts mostly rose with some falling.

The plastic 2509 contract is quoted at 7,297 yuan/ton, up 0.12% from the previous trading day.

The PP2509 contract is quoted at 7079 yuan/ton, up 0.18% from the previous trading day.

The PVC2509 contract is quoted at 5008 yuan/ton, up 0.32% from the previous trading day.

The styrene 2507 contract is quoted at 7,254 yuan/ton, down 0.18% from the previous trading day.

4. Market Forecast

PE: The current polyethylene market is in its traditional off-season, with the demand side showing significant weakness. Traders are adjusting their operational strategies based on real-time market conditions. However, due to the lack of transactions in high-price ranges, overall market circulation activity is relatively low. Downstream enterprises are affected by the off-season effect, with operating rates declining both year-on-year and month-on-month. Their procurement of polyethylene raw materials has significantly reduced, focusing mainly on meeting the rigid demand for immediate production, with little willingness to replenish inventory proactively. Against this backdrop, the polyethylene spot market lacks effective demand support, and upward price momentum is insufficient, resulting in an overall weak consolidation pattern. In summary, without major positive factors such as a significant recovery in demand or unexpected prolonged shutdowns of facilities, polyethylene market prices are unlikely to rise and will oscillate weakly around the current levels. However, if there is a concentrated resumption of production facilities in the future, leading to a substantial increase in supply while demand remains weak, the polyethylene market prices may face downward pressure.

PP: There are no changes in the domestic PP facilities for now, and the start-up time of some units remains uncertain. The market is intertwined with both bullish and bearish factors. From the perspective of the international crude oil market, the continuation of U.S. sanctions on oil-producing countries is a positive factor. However, OPEC+’s stance on increasing production, the easing of geopolitical tensions, and the poor global economy are negative factors. Especially, OPEC+ might significantly increase production in September, and the U.S. sanctions on Russia are not expected to cause significant supply disruptions, which suppresses the market, thereby affecting the cost side of polypropylene. Against this backdrop, the domestic polypropylene dollar market prices have made partial narrow adjustments, while the domestic market prices continue to run weakly. The terminal market is affected by the macroeconomic environment and its own demand structure, leading to a continued low willingness to take orders. Traders are making slight adjustments to quotes to foster transactions, and actual transaction prices can be negotiated based on market conditions, but the overall spot market remains weak, with market transaction volume still sluggish, reflecting the weak supply and demand situation in the market. Overall, in the short term, the polypropylene market is expected to continue a weak and volatile pattern.

PVC: Currently, the product is undergoing slight adjustments within the range after a decline. The fundamentals of PVC have remained largely unchanged, with upstream PVC production enterprises maintaining high operating rates, resulting in a high level of supply. On the demand side, procurement continues to be primarily driven by rigid demand. After the futures prices declined, transactions improved slightly compared to when prices were at higher levels, but after today's rise in futures prices, the advantage of pricing by points disappeared, and the spot market has returned to a period of observation. Internationally, oil prices fell for the third consecutive trading day, reaching their lowest level in a week, as the Organization of the Petroleum Exporting Countries and its allies (OPEC+) agreed to significantly increase production again in September, exacerbating concerns about an oversupply of oil. Overall, in the short term, the PVC spot market will continue to experience narrow adjustments.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)