Off-Season Demand Weighs on PP Prices, Supply-Demand Imbalance Drives Volatile Trend; Plastics Weaken Today With POM Down Up to 300

Weak demand season suppresses PP prices; supply and demand contradictions dominate the volatile pattern.

Introduction: With the cooling down of macro policy speculation, the expansion project at CNOOC Daxie has been delayed until mid-August, easing supply pressure; on the demand side, weak demand persists, with downstream just-in-time purchasing during the off-season, and no improvement in demand currently, leading to cautious market sentiment.

1. Demand has eased, and expectations may improve.

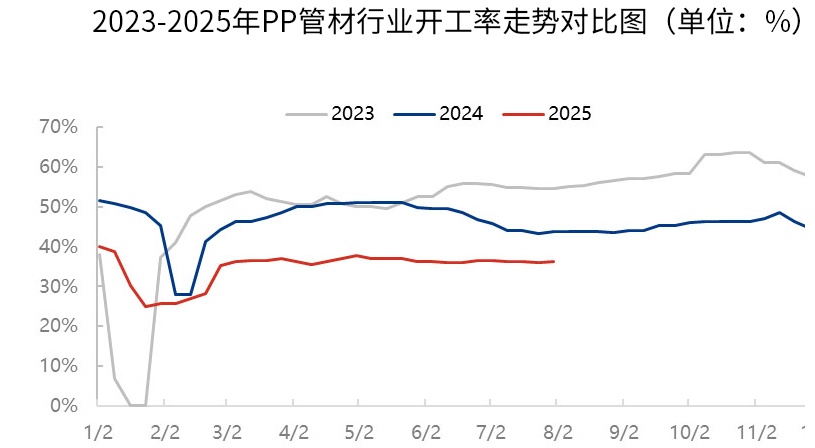

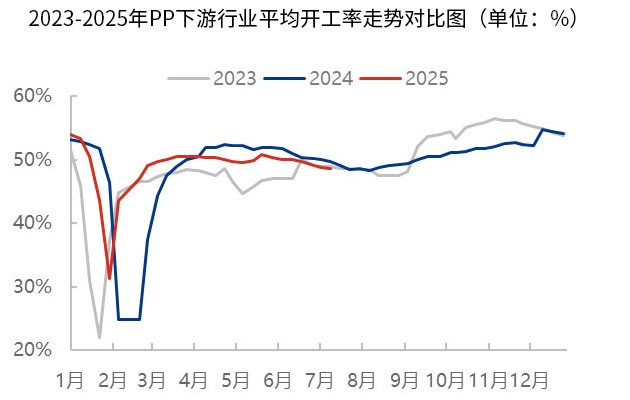

Driven by favorable macroeconomic policies, some downstream product manufacturers saw an improvement in orders last week. The average operating rate of China's polypropylene downstream industries—including woven bags, injection molding, BOPP, PP pipes, PP nonwoven fabric, CPP, PP transparent products, and modified PP (a total of eight downstream sectors)—rose by 0.03 percentage points to 48.40%. During the week, there was a clear divergence in the operating rates among various downstream sectors of polypropylene. Only the PP pipe, PP transparent products, and PP injection molding sectors showed an upward trend in operating rates. Among them, the PP pipe industry benefited from a slight increase in construction and infrastructure project initiations, leading to improved market demand and a rise in operating rates.

Overall, although there has been a slight recovery in demand from some downstream industries of polypropylene, the support on both supply and demand sides remains limited. However, as terminal demand gradually warms up in August, inventory replenishment is expected to steadily increase, and the operating rates across various industries may see a stable upward trend.

2. Macro guidance cools down, PP prices rise then fall back

The macroeconomic guidance on the market has weakened, and polypropylene has entered a demand pricing phase. On the fundamentals, the commissioning of Ningbo Daxie has been delayed, pushing back the expected supply pressure, and resources are being consumed positively during the commissioning window. In terms of demand, factory procurement pace has slowed down at the end of the month, with reduced enthusiasm, making it difficult to form upward momentum. Influenced by a strong policy cycle, market sentiment is becoming cautious, and spot price fluctuations are converging. As of July 31, 2025, the mainstream price for East China yarn is between 7080-7200 yuan/ton.

3. Medium- to long-term conflicts still lie in the fundamentals

At the macro level, the economic stabilization policies introduced by the Central Politburo Work Meeting and the expectation of RMB depreciation, which is beneficial for exports, will become important drivers guiding the market. The supply and demand sides are at a critical stage of variability, with intensive maintenance in August and new capacity expansion offsetting each other. The demand side is at a key period of seasonal transition, with potential for demand variables to improve from weakness. However, due to global trade barriers and tariffs, the demand side's valuation is lower than the same period last year. The support from the cost side is limited, with the expectation of OPEC+ production increase affecting international oil prices, leading to anticipated easing in oil-based costs. The supply-demand fundamentals of the polypropylene industry are difficult to change, with external policy becoming an important breakthrough to drive the market out of the stalemate. In a situation where external difficulties and internal challenges coexist, it is expected that the market's deadlock will persist, with intermittent surges driven by policy boosts. Close attention should be paid to changes in foreign trade export orders, fluctuations in the cost side, and the release of new capacity expansion.

Today's plastic prices

(The above content is compiled from Jinlianchuang and Dayi Yosu)

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)