Nearly 30% price drop in one year! the spandex industry enters a tight competition! following xiaoxing, this chemical giant also begins to shrink its spandex production lines in china.

In recent years, as the domestic chemical industry enters a new round of capacity growth, the competition in the industry of various chemical fiber raw materials, including spandex, has become intense. Overseas chemical giants find it difficult to earn excess profits and are unwilling to engage in “close combat” with domestic companies, leading them to begin retreating.

South Korean chemical leader reduces production lines in China

According to reports, South Korea's Taekwang Group announced that it will suspend the operation of some spandex production lines at its Chinese subsidiary, Taekwang Chemical Fiber (Changshu) Co., Ltd., starting July 14, 2025, and will reassess its future strategy. This is the first time Taekwang Group has shut down production lines at a spandex factory in China. It is believed that this decision is due to the ongoing large-scale expansion of Chinese competitors and the slow recovery of market demand, leading to a deterioration in the profitability of the local factory.

Tai Kwang Fiber (Changshu) Co., Ltd. was established in 2003 and is the overseas spandex production base of the South Korean Tai Kwang Group, with an annual output of nearly 30,000 tons. Tai Kwang Fiber (Changshu) Co., Ltd. has suspended one production line for equipment inspection on July 14, 2025, and is considering shutting down another production line on July 21, with further adjustments possible based on evaluation results. According to a relevant person from the South Korean Tai Kwang Group, no specific decision has been made yet regarding whether to close or withdraw from the factory.

Previously, the South Korean Taekwang Group decided in May last year to suspend its investment in Taekwang Chemical Fiber (Ningxia) Co., Ltd.'s differentiated spandex project with an annual production capacity of 108,000 tons, and deemed the previous investment funds as losses, judging that they could not be recovered.

Tai Kwang Fiber (Changshu) Co., Ltd. was once regarded as a cash cow for the Korean Tai Kwang Group. However, the company has now incurred losses for three consecutive years and is currently in a state of complete capital impairment. Data shows that Tai Kwang Fiber (Changshu) Co., Ltd. has experienced a continuous decline in sales since 2021, resulting in consecutive losses. Considering that Chinese competitors are expanding their production capacity through large-scale investments, its future prospects look even bleaker.

Xiaoxing Spandex gradually shuts down old production lines.

Apart from Taekwang, another Korean giant, Hyosung, is also gradually shutting down its old production capacity.

The South Korean spandex company Xiaoxing Group is gradually advancing its capacity westward plan. Its old production capacity in the eastern coastal region is also being gradually shut down due to environmental and cost reasons. Xiaoxing Spandex (Jiaxing) Co., Ltd. has already shut down 8 production lines by the end of 2023, will shut down 2 more lines by July 2025, and plans to shut down another 2 lines by March 2026, with all shut down by the end of 2026.

According to China's "Carbon Peak Implementation Plan for the Chemical Fiber Industry," starting from 2025, a carbon tax of 200 yuan per ton will be levied on spandex that exceeds a carbon emission of 3.2 tons per ton. Some older facilities have emissions significantly above this standard, resulting in a loss of competitiveness in terms of pricing. The plan also mentions promoting lower energy-consuming "melt-spun spandex" technology. If the cost of upgrading the necessary equipment is high, this will accelerate the phase-out of older spandex facilities. Additionally, new capacity requires substantial funding, and with unclear profit prospects, foreign investment willingness in spandex production is currently low.

The spandex industry has fallen into "close combat."

As of the end of 2024, the global spandex production capacity has increased to 1.75 million tons, with domestic capacity accounting for over 75%. Compared to the same period last year, the year-on-year growth rate of global spandex capacity reached 7%, with the increase mainly coming from the mainland Chinese market, where the new spandex production capacity totaled 115,000 tons. Domestic spandex capacity reached 1.3545 million tons, a year-on-year increase of 9.3%. In terms of production, domestic spandex output reached 1.045 million tons, an increase of 11.3% year-on-year; regarding imports and exports, exports amounted to 69,600 tons, up 13.2% year-on-year, while imports were 47,900 tons, down 4.8% year-on-year. Domestic spandex apparent demand was 1.012 million tons, a year-on-year increase of 10.3%.

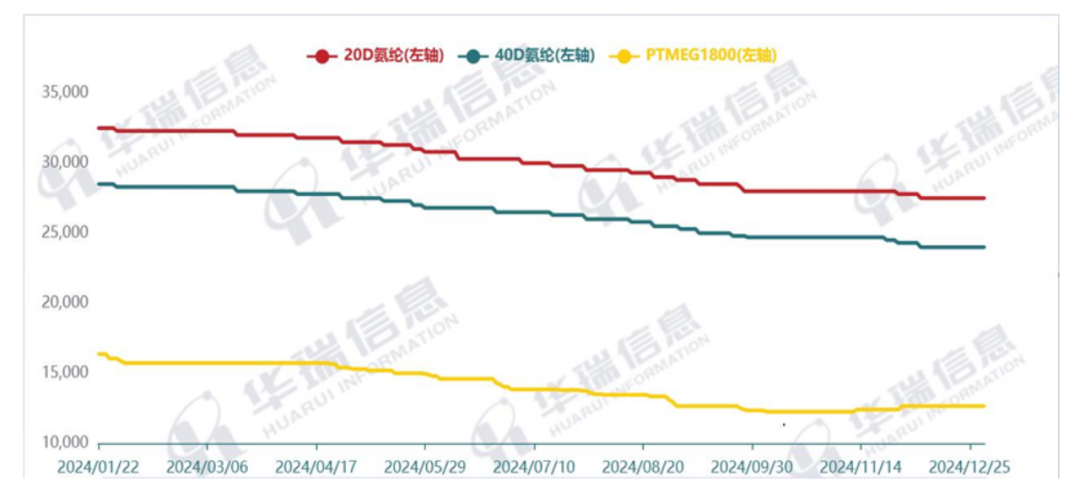

In recent years, the spandex industry has entered a downward cycle from the peak of prosperity in 2021. The prices of spandex fibers have been adjusting downward, the industry's profitability has decreased, and the market landscape is undergoing deep restructuring. In 2024, spandex prices will continue to trend downward, repeatedly hitting historical lows; the supply of spandex exceeds demand, and the prices of the main raw material PTMEG continue to decline, with the average annual price dropping by 29% compared to 2023. Lacking cost support, the situation of most companies in the industry incurring losses is still difficult to reverse.

Currently, apart from South Korea's Daewoo Group, which continues to actively build spandex production capacity in China, the market share of other foreign spandex manufacturers is being continuously squeezed, and they may completely withdraw from the Chinese market.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)