【Morning Plastics Market Update】Oil prices surge! As the maintenance season approaches, PE and PVC are showing weaker performance, while PP is experiencing range-bound fluctuations.

Summary: Morning prompt for the general plastics market on March 21! The United States continues to strengthen sanctions against Iran, and the instability in the Middle East brings potential supply risks, leading to an increase in international oil prices. Increased maintenance volumes alleviate supply pressures, with PE market prices showing a weak trend; overall demand is weak, and the PP market may experience range-bound fluctuations; there is no expectation of improvement in the supply and demand fundamentals, and the PVC market maintains a weak and stable operation; strong photovoltaic demand supports, and EVA is mainly expected to remain stable or slightly weaker.

PP

I. Focus Points

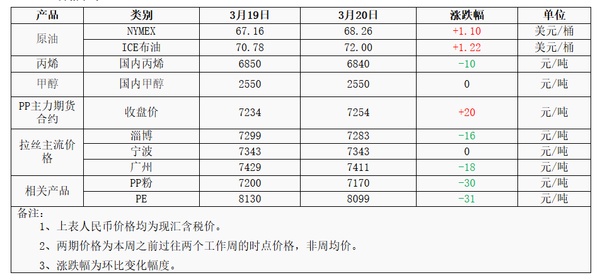

The US continues to strengthen sanctions against Iran, and the instability in the Middle East brings potential supply risks, leading to an increase in international oil prices. The NYMEX04 contract rose by $1.10 to $68.26 per barrel, a month-on-month increase of +1.64%; the ICE Brent crude futures 05 contract increased by $1.22 to $72.00 per barrel, a month-on-month increase of +1.72%. China's INE crude oil futures main contract 2505 rose by 0.6 to 522 yuan per barrel, and the night session increased by 12.1 to 534.1 yuan per barrel.

2, Propylene FOB Korea remains at 810 USD/ton, CFR China remains at 830 USD/ton.

3. The polypropylene capacity utilization rate for this period (March 14, 2025 - March 20, 2025) decreased by 5.08% to 76.98%; Sinopec's capacity utilization rate decreased by 2.95% to 87.12%.

4. This week, the domestic polypropylene production was 732,600 tons, a decrease of 44,800 tons from last week's 777,400 tons, with a decline rate of 5.76%. Compared to the same period last year, which was 642,500 tons, it increased by 90,100 tons, with a growth rate of 14.02%.

core logic: input format:Downstream order follow-up is limited, and weak demand is insufficient to support prices.

II. Price List

Three, Market Outlook

Today, international oil prices have risen significantly, enhancing cost support, which is beneficial for the spot quotes of plastics. The number of maintenance units at upstream production enterprises has increased, with a noticeable decline in weekly output data, and no new capacity has been added, making the supply pressure manageable. However, there has been no significant improvement in new orders from downstream factories, and overall weak demand provides insufficient support for PP prices. It is expected that the polypropylene market will fluctuate within a range today.

PE

I. Focus Points

1cost end:The US continues to strengthen sanctions on Iran, and the instability in the Middle East brings potential supply risks, leading to an increase in international oil prices. The NYMEX crude oil futures 04 contract rose by $1.10 per barrel to $68.26, a month-on-month increase of +1.64%; the ICE Brent crude oil futures 05 contract increased by $1.22 per barrel to $72.00, a month-on-month increase of +1.72%.

2current parking equipment:Currently, the parking equipment involves 26 sets of polyethylene equipment, with additional maintenance for Sinopec Shanghai Petrochemical and Daqing Petrochemical.

3、yesterday's market review:The domestic polyethylene market fell the previous day, with a decline of 8-60/ton. Factory prices were reduced, and as costs shifted downward, traders continued to offer discounts on sales, maintaining a cautious atmosphere.

core logic: input format:The spot market for polyethylene is operating with a weak and fluctuating trend.

II. Price List

Three, Market Outlook

Maintenance volume increase alleviates supply pressure; downstream factories have a bearish sentiment, leading to decreased procurement. In the short term, the contradiction between supply and demand still exists, and polyethylene market prices are operating on the weaker side.

PVC

I. Focus Points

3/20: The US continues to strengthen sanctions against Iran, and the instability in the Middle East brings potential supply risks, leading to an increase in international oil prices. NYMEX crude oil futures 04 contract rose by $1.10 per barrel to $68.26, up 1.64% month-over-month; ICE Brent crude oil futures 05 contract increased by $1.22 per barrel to $72.00, up 1.72% month-over-month. China's INE crude oil futures main contract 2505 rose by 0.6 to 522 yuan per barrel, and the night session increased by 12.1 to 534.1 yuan per barrel.

2, Carbide: Currently, the number of downstream vehicles awaiting unloading remains low, and regional shortages in arrivals are affecting PVC production loads. However, with improved profitability, there is an increased enthusiasm for production among manufacturers. Previously shut-down facilities are gradually resuming operations, leading to a growing trend in the supply of commercial carbide. Next week, due to maintenance on PVC in the Sichuan region, demand will decrease, which may gradually stabilize market prices. It is expected that, with the recent price increases in the Ningxia region, there will be an overall increase of 50 yuan/ton in market trading prices. However, next week, as the market enters a phase of stabilization and inventory replenishment, regional performance will become more pronounced.

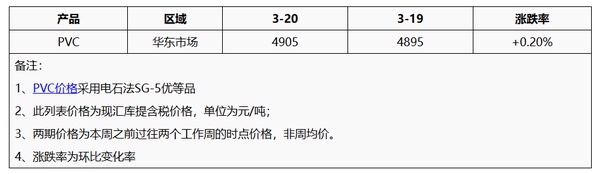

3, PVC: The domestic PVC market price remained firm yesterday, with a slight decline in transactions; the load of PVC production enterprises changed little within the week, and the supply slightly decreased due to the temporary impact of individual equipment loads. The atmosphere for exports at low prices was acceptable, and the spot prices in the market remained firm. As of March 20th, the warehouse withdrawal price for the five-type calcium carbide method in the East China region was 4800-4950 yuan/ton, and for the ethylene method, it was 4950-5200 yuan/ton.

II. Price List

Three, Market Outlook

PVC current supply remains at a high level, but domestic downstream demand is still mainly based on rigid demand. Forward orders are performing poorly, and there is no expectation of improvement in the supply and demand fundamentals. At present, the supply of raw material calcium carbide is tight, and prices still show signs of increase. The cost bottom support is firm, and at the same time, driven by foreign trade delivery and terminal restocking demand, industry inventory continues to decrease. Overall, the supply and demand of PVC continue to be in a tug-of-war, and it is expected that the PVC market will maintain a weak and stable operation in the short term.

EVA

I. Focus Points

3/20: The US continues to strengthen sanctions against Iran, and the instability in the Middle East brings potential supply risks, leading to an increase in international oil prices. The NYMEX 04 contract rose by $1.10 to $68.26 per barrel, up 1.64% month-over-month; the ICE Brent oil futures 05 contract increased by $1.22 to $72.00 per barrel, up 1.72% month-over-month. China's INE crude oil futures main contract 2505 rose by 0.6 to 522 yuan per barrel, and in the night session, it increased by 12.1 to 534.1 yuan per barrel.

2, Ethylene: The amount of market-available goods in the next cycle remains relatively ample, but it is difficult for downstream external purchases to increase. Considering the above factors, it is expected that the market will continue to decline. In the US dollar market, the weak performance of the domestic market, coupled with the low willingness of downstream factories to negotiate, has put pressure on import suppliers, and there is a possibility of individual negotiations becoming more flexible. The transaction range is expected to be maintained between 6800-7300 yuan/ton; the US dollar market is expected to be between 840-870 US dollars/ton.

Vinyl acetate: Some vinyl acetate production facilities are under maintenance or have delayed operations, and the release of new production capacity has been postponed. In the short term, market supply may decrease or fall short of expectations. The negotiation prices for large spot orders have started to ease, and intermediaries' sales pace is becoming more cautious. Industry sentiment is cautiously optimistic, with a focus on the production scheduling of downstream EVA. The market is expected to undergo a period of consolidation next week amid supply and demand dynamics.

core logic: input format:Cost side ethylene and vinyl acetate are weakly stable, with relatively weak cost support. The EVA supply side is under no pressure to maintain the market. Downstream foam demand follows rigid demand, and the supply and demand may operate stably or be adjusted for stability.

II. Price List

Three, Market Outlook

In the short term, the situation of weak supply and demand for EVA domestically may continue. Strong photovoltaic demand provides support, while foam demand is expected to follow rigid needs without change. EVA producers generally face no pressure in maintaining the market, with transactions being in a stalemate. Industry players are mainly adopting a cautious wait-and-see attitude, tending to conclude operations. It is expected that the domestic EVA market will mainly be stable but slightly weak. Mainstream market prices: hard materials will fluctuate between 11200-11700 yuan/ton, soft materials may fluctuate between 11400-11900 yuan/ton, and photovoltaic materials will fluctuate between 11500-11900 yuan/ton.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)