Mixed Fortunes in July New Energy Vehicle Sales

Even during the traditional off-season for automobile consumption, the new energy passenger vehicle market remains vibrant. Highly attractive policy subsidies, coupled with a stable supply environment, have boosted the consumption of new energy vehicles, resulting in a "not-so-slow" market in July. Some car manufacturers have achieved record-high wholesale sales of new energy vehicles.

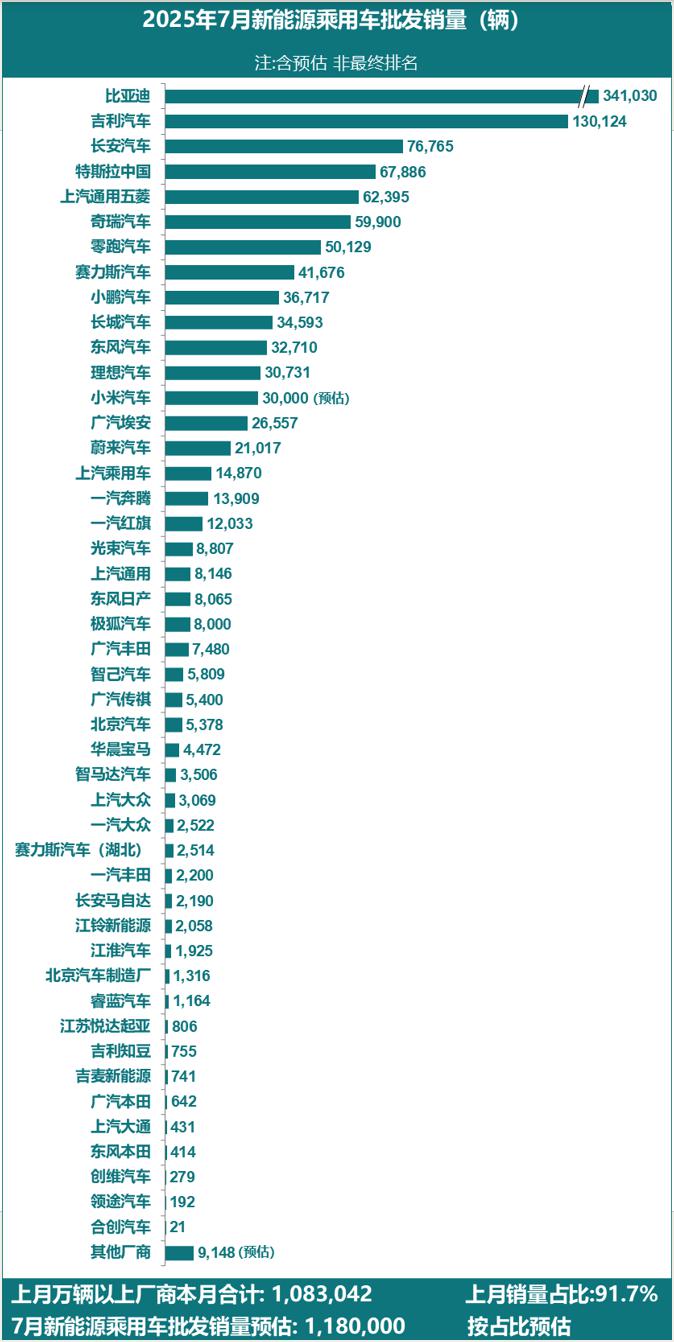

According to the China Passenger Car Association's forecast, the wholesale sales of new energy passenger vehicles nationwide in July reached 1.18 million units, representing a year-on-year increase of 25% and a month-on-month decline of 4%. From January to July this year, the cumulative wholesale volume was 7.63 million units, marking a year-on-year growth of 35%.

Analyzing the wholesale sales statistics of new energy passenger vehicle manufacturers for July released by the China Passenger Car Association, the lively market reflects numerous changes, revealing the fierce competition in the new energy passenger vehicle market.

The new 2+1 structure in the new energy vehicle market is becoming stable. BYD and Geely Automobile maintain the top two positions in new energy vehicle sales, with sales reaching 341,000 and 130,100 units respectively in July. Changan Automobile, SAIC-GM-Wuling, and Tesla are competing for the third position.

At the same time, the number of new energy passenger car manufacturers with monthly sales exceeding 10,000 vehicles has increased compared to last year. FAW Bestune and FAW Hongqi entered the 10,000-vehicles-per-month club with sales of 13,900 and 12,000 units respectively.

Many car manufacturers have achieved record-high sales in the new energy sector. Leapmotor, XPeng Motors, Xiaomi Auto, Dongfeng Nissan, and GAC Toyota have all reached historical highs in their wholesale sales of new energy vehicles. Notably, Leapmotor's monthly sales surpassed 50,000 units for the first time, leading the new wave of car manufacturing. Dongfeng Nissan and GAC Toyota, with their high "China content" models, have become pioneers in the transformation of joint-venture brands towards new energy. Geely Auto and Spotlight Automotive have also achieved their own record-high monthly sales performances.

In fact, behind the record-breaking sales and sustained high sales momentum is the creation of hit products that cater to market demand, such as the Leapmotor B10, Leapmotor C10, XPeng MONA M03, Xiaomi YU7, Dongfeng Nissan N7, and GAC Toyota Bozhi 3X. These models have driven the record-high sales of new energy vehicles for various brands.

The continuous boom in the pure electric small car market has driven the sales growth of new energy vehicles for automakers such as SAIC-GM-Wuling, Geely Automobile, and FAW Bestune. Especially SAIC-GM-Wuling, which experienced three consecutive years of declining sales, has leveraged the sustained popularity of the pure electric small car market. The sales of Wuling Hongguang MINI EV and the Wuling Bingo family have achieved rapid growth, enabling SAIC-GM-Wuling's new energy vehicle sales to maintain a high level and helping the company overcome the embarrassment of negative sales growth.

Joint venture brands' new energy vehicle sales diverge. In the wholesale sales statistics of new energy passenger vehicles in July, SAIC-GM, Dongfeng Nissan, and GAC Toyota achieved sales of 8,146 units, 8,065 units, and 7,480 units of new energy vehicles, respectively, thanks to their popular models with high "China content," making them leaders in the joint venture brand new energy transition. In contrast, new energy products from joint venture automakers such as FAW-Volkswagen, FAW Toyota, GAC Honda, and Changan Mazda are lukewarm, with monthly sales hovering between several thousand and even several hundred units.

In July, although the new energy vehicle market showed a strong performance during what is typically a slow season, external factors such as summer holidays and hot weather had some impact on the consumption of new energy vehicles. Among the 18 car companies with monthly sales exceeding 10,000 units, 12 companies, including BYD, Changan Automobile, Tesla, Chery Automobile, SAIC-GM-Wuling, Great Wall Motors, Li Auto, GAC Aion, NIO, etc., experienced a month-on-month decline in new energy vehicle sales.

Tesla, Li Auto, and GAC Aion all experienced both year-on-year and month-on-month declines. Among them, GAC Aion, which is in a deep adjustment period, saw its sales volume shrink to 26,600 units in July, representing a year-on-year decrease of 24.6% and a month-on-month decrease of 4.6%.

Tesla's sales in July were 67,900 units, a month-on-month decrease of 5.19% and a year-on-year decrease of 8.41%. The decline in Tesla's sales is partly due to two Xiaomi models diverting demand from the Model 3 and Model Y. Additionally, frequent price changes and the new Model Y L have led some consumers to hold off on purchasing.

Li Auto's sales in July hit a historic low, delivering 30,700 new vehicles, a year-on-year decrease of 39.74% and a month-on-month decline of 15.29%. The sales of Li Auto's L series products have shrunk amid fierce market competition. Meanwhile, the highly anticipated Li Auto i8 has faced setbacks in product configuration and marketing.

Fortunately, Li Auto promptly adjusted the configuration and pricing strategy of the Li Auto i8 by canceling the Pro and Ultra versions, making the Max version the standard configuration, and lowering the price from 349,800 yuan to 339,800 yuan, addressing consumer complaints about the complicated versions and the lack of support for optional high-end configurations.

Behind the rapidly growing new energy vehicle market, undercurrents are actually surging. Various automakers are fiercely competing in different market segments, and the competition is becoming increasingly intense. At the same time, new energy vehicles still present more opportunities than challenges. There are still structural blue oceans in niche markets, and creating best-selling models that meet market demand is the guarantee for sustained sales growth, as well as the key to changing the market landscape.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)