Mid-Year Report | 2025 Personal Care Small Appliance Market Summary: Breaking Through Amid Differentiation, Innovation Steers the Course

— Category Overview —

Hair dryer | Electric toothbrush | Electric shaver

01

Market Index

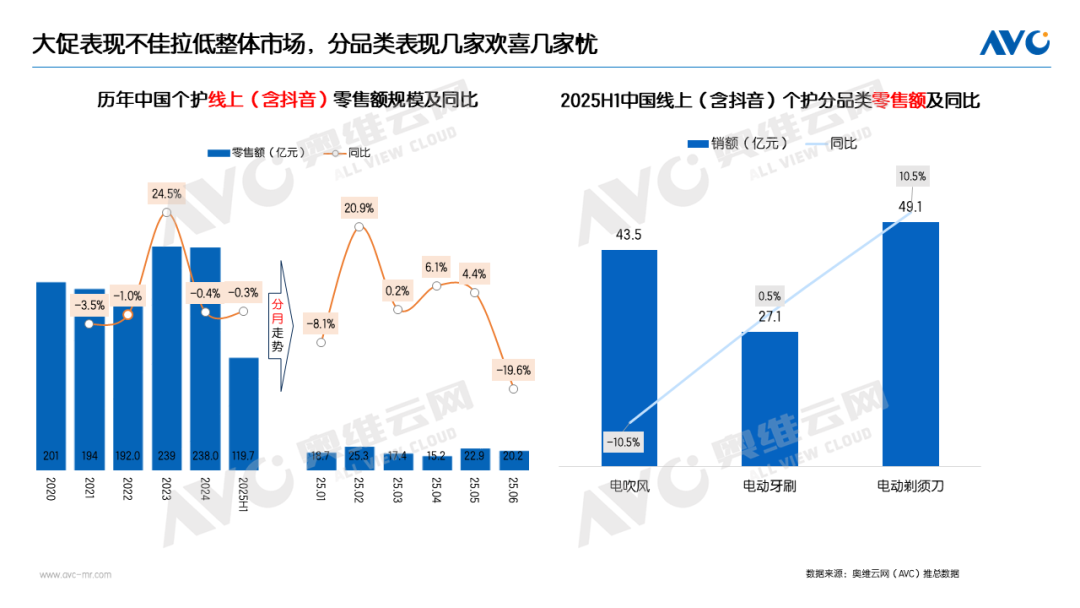

In the first half of 2025, the personal care small appliances market showed diverse development trends, with mixed sales performances across different categories. According to data from AVC (All View Cloud), the total online retail sales of personal care small appliances (including hair dryers, electric toothbrushes, and electric shavers) reached 11.97 billion yuan, representing a year-on-year decrease of 0.3%.

By category, the hair dryer segment experienced a 10.5% year-on-year decline in retail sales due to the saturation of the high-speed hair dryer market and the fading of technological dividends, weakening its previous growth momentum. The electric toothbrush segment achieved a 0.5% scale increase driven by structural upgrades; the deep penetration of intelligent features, breakthroughs in cleaning technology iterations, and segmented designs targeting different user groups have become the core drivers enabling it to withstand market fluctuations. Meanwhile, the electric shaver segment performed exceptionally well, with retail sales soaring 10.5% year-on-year, propelled by the continued penetration of portable products and dual-driven product structure upgrades, emerging as a prominent highlight in the personal care small appliances market in the first half of the year.

02

Channel Structure

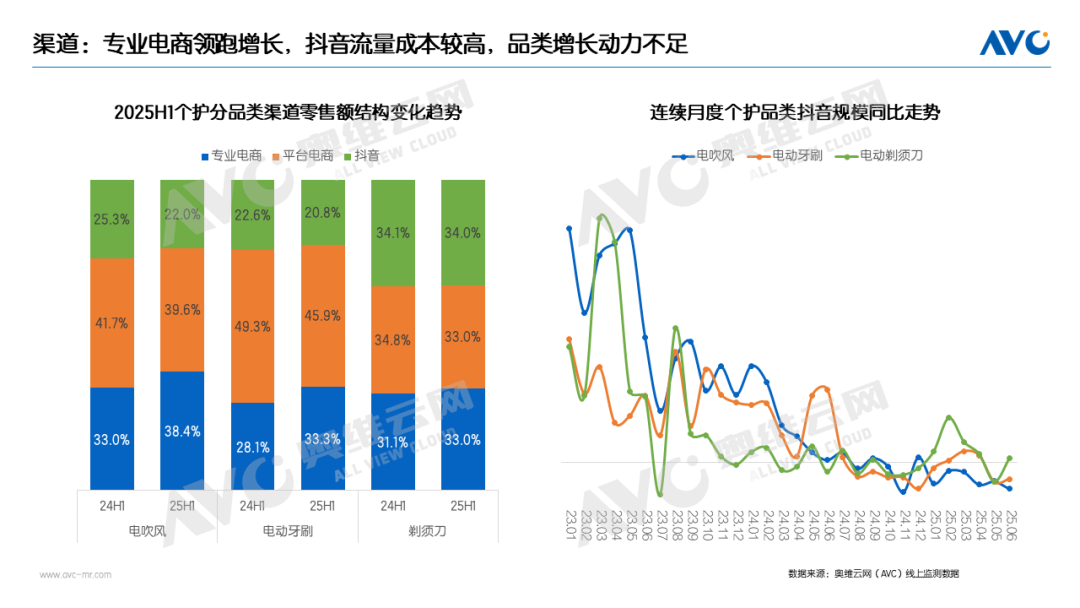

Professional e-commerce platforms have taken the lead in growth by precisely operating and capturing user mindshare in the personal care small appliance category. The retail market shares of hair dryers, electric toothbrushes, and electric shavers increased by 5.4%, 5.2%, and 1.9% respectively. In contrast, the Douyin channel is facing challenges such as market saturation and insufficient growth momentum. How to break through these bottlenecks through content innovation and deeper category cultivation has become an urgent issue to address.

Meituan, Alibaba, and JD.com are going all out as the battle for instant retail intensifies. According to estimates by the research team from the Institute of International Trade and Economic Cooperation of the Ministry of Commerce, the total scale of instant retail in China reached 650 billion yuan in 2023, growing 9.46 times over five years with a compound annual growth rate exceeding 56%. Personal care small appliances, due to their moderate price and immediate usability, highly align with the consumption scenarios of instant retail and are expected to gain more growth opportunities amid this channel transformation.

Channel integration is becoming deeper, with brands leveraging emerging platforms such as Douyin live streaming and Xiaohongshu for user education and brand awareness building. This, in turn, drives traffic back to traditional e-commerce platforms, forming a new pattern of coordinated channel development and supporting scale growth.

03

Product Trends

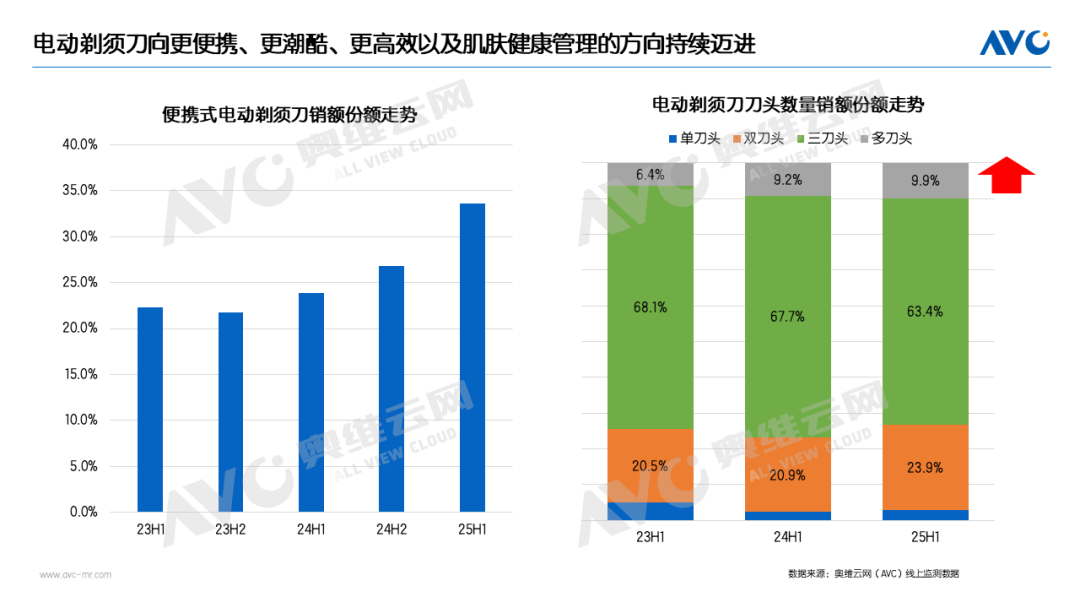

Electric shavers are continuously advancing towards being more portable, trendy, efficient, and better for skin health management.

Portability has become a mainstream trend, with market share rising from 23.9% in the first half of 2024 to 33.6% in the first half of 2025. Meanwhile, there is a significant upgrade in product premiumization, with the average price increasing by 23.7% year-on-year. As more brands enter the market, product innovation is emerging continuously. The design is becoming more refined and compact, with stainless steel and alloy materials enhancing the texture. Customizable elements, magnetic heads, and details such as sliding switches enhance the user experience. The iteration of efficient shaving technology is accelerating, with multi-head designs, optimized blade nets, and increased motor speed significantly improving shaving efficiency. Products suitable for sensitive skin, addressing men's skincare needs, and multi-functional products (shaving + nose hair trimming + facial cleansing + sideburn trimming) further meet consumers' higher demands for a comfortable shaving experience.

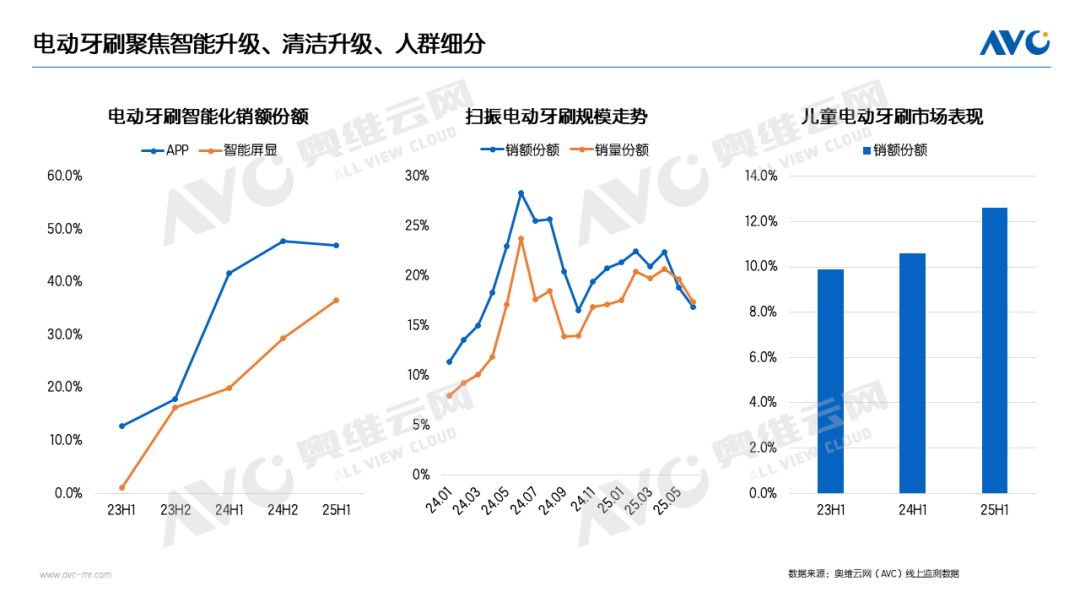

Electric toothbrushes focus on smart upgrades, cleaning enhancements, and market segmentation.

The intelligentization of electric toothbrushes is becoming more prominent, becoming a core competitiveness in the mid-to-high-end market. According to online data from AVC, in the first half of 2025, electric toothbrushes with app functionality will account for 47% of sales value, while those with smart display features will account for 36.6%. Products continue to upgrade, achieving a "thousand teeth, thousand faces" state by automatically adjusting the amplitude and vibration frequency according to different tooth surfaces. Since their debut in 2023, the penetration rate of oscillating electric toothbrushes has been continuously increasing, reaching a retail sales share of 20.3% in the first half of 2025. Some brands combine oscillation with visualization to provide a more intuitive cleaning experience. Children's electric toothbrushes are undergoing dual transformations in intelligentization and fun, with app functionality and smart displays both accounting for more than half. In terms of fun, besides cartoon appearances, designs like voice prompts, voice teaching, and brushing progress bars enhance children's initiative in brushing.

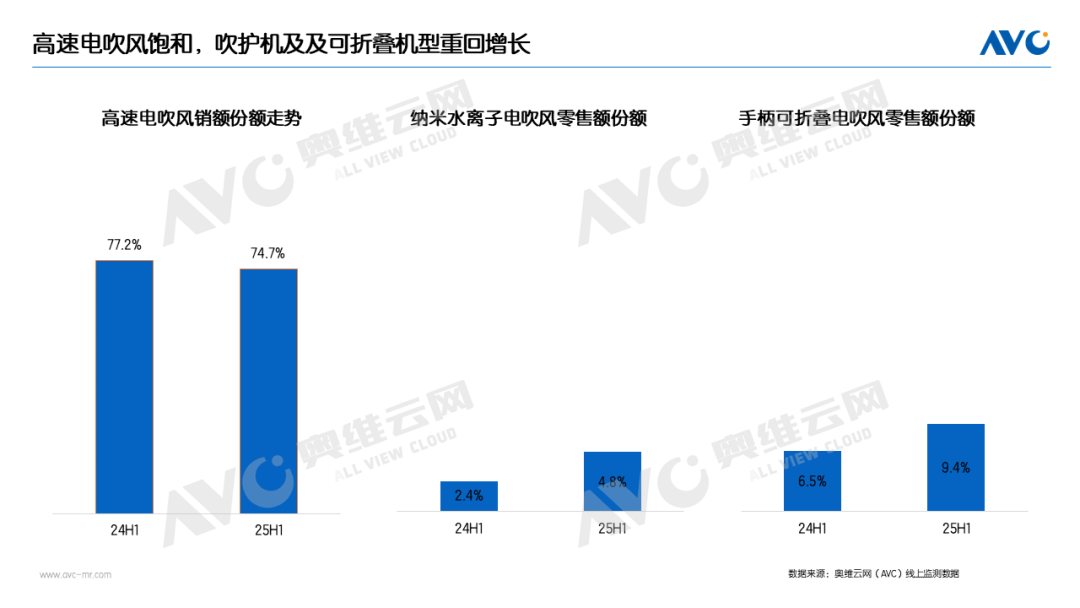

High-speed hair dryers reach saturation, while blow-dryers with protective features and foldable models return to growth.

Since 2021, high-speed hair dryers have experienced four years of rapid development, and now the market has become saturated. In the first half of 2025, the retail market share reached 74.7%, a year-on-year decrease of 2.5%. As the technology becomes increasingly mature, the value proposition of high-end features is gradually diminishing, and the market share of products priced between 200-300 yuan has significantly increased. Furthermore, in the context of severe product homogenization in the saturated high-speed market, hair care devices have returned to consumers' attention. The retail market share of nano water ion products has increased by 2.4% year-on-year, and foldable handles make them convenient for storage, precisely targeting business travelers.

Conclusion

The differentiated landscape of the personal care small appliance market in the first half of 2025 has essentially outlined the development trajectory for the entire year. For brands, it is necessary not only to keenly capture growth opportunities in various categories and continuously drive product innovation to create high-quality products that meet consumer expectations, but also to respond flexibly to channel transformations, optimize channel layouts, and enhance market penetration. Only by constantly adapting to market changes, using innovation as an oar and channels as a sail, can brands ride the waves of the personal care small appliance market and win broader development opportunities.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift