Massive Retreat of Japanese and Korean Battery Manufacturers

The once-dominant Japanese and Korean battery manufacturers are now retreating globally.

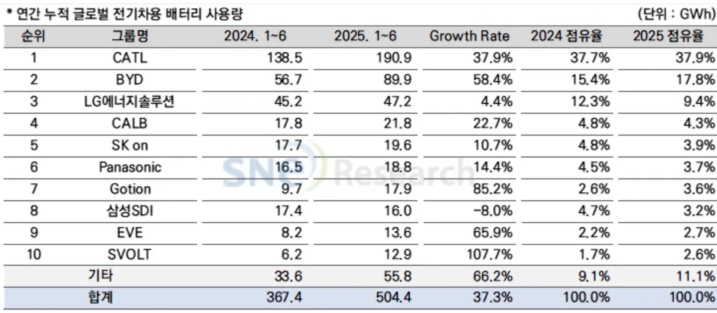

Recently, Korean research institution SNE Research released the latest data, showing that the global electric vehicle (EV, PHEV, HEV) battery installation volume reached 504.4 GWh in the first half of 2025, a year-on-year increase of 37.3%. The market share of a number of Japanese and Korean battery manufacturers, including LG Energy Solution, SK On, Samsung SDI, and Panasonic, further declined.

In the first half of this year, among the world’s top ten companies for power battery installation volume, China accounted for six seats, with a total installed volume of 347 GWh and a total market share of 68.8%, an increase of 4 percentage points year-on-year, reaching a record high. Japanese and Korean companies took four seats, with a total installed volume of 101.6 GWh and a combined market share of 20.1%, down 6.3 percentage points from the same period last year; this is far behind CATL alone (190.9 GWh).

Declining market share

In this list released by a Korean institution, the three major Korean battery companies, LG Energy Solution, SK On, and Samsung SDI, are showing signs of decline, as even their combined efforts could not surpass the second-ranked BYD.

In the first half of this year, BYD's global battery installation volume surged by 58.4% to reach 89.9 GWh, with its global market share rising to 17.8%. In contrast, the combined market share of the three major Korean companies dropped by 5.4 percentage points compared to the same period last year, falling to 16.4%, with a total installed capacity of 82.8 GWh.

LG Energy Solution, while still ranked third with an installed capacity of 47.2 GWh, only achieved a year-on-year growth of 4.4%, with its market share dropping from 12.3% in the same period of 2024 to 9.4%. The financial report released by LG Energy Solution shows that the operating income in the second quarter of 2025 decreased by 9.7% year-on-year to 5.56 trillion KRW (approximately 28.8 billion RMB).

It is understood that LG Energy Solution currently supplies batteries mainly to automakers such as Tesla, Chevrolet, Kia, and Volkswagen. According to analysis by SNE Research, "Due to a decline in the sales of models equipped with LG Energy Solution batteries, Tesla's usage of these batteries has decreased by 28.9%."

SK On ranked fifth with an installed capacity of 19.6 GWh, a year-on-year increase of 10.7%, while its market share declined from 4.8% in the same period of 2024 to 3.9%. The main reason is the weakened demand for its batteries in the European and North American markets. It is noteworthy that SK On has been operating at a net loss since 2021 and has yet to achieve positive profitability. In 2024 alone, the company's loss amounted to as much as 1.1 trillion Korean won (approximately 5.85 billion RMB).

In 2025, SK On will continue to face severe downward pressure on net profit, with losses expected to further expand. Nomura Orient International Securities released a report stating that SK On's operating profit is expected to incur a loss of $340 million (approximately RMB 2.44 billion), extending the loss trend from 2024. This is mainly due to a significant slowdown in global electric vehicle demand growth, resulting in a sharp decline in the utilization rate of its battery factories.

Samsung SDI ranked eighth with an installed capacity of 16GWh, a year-on-year decrease of 8%, making it the only company among the top ten to experience negative growth. Its market share also dropped from 4.7% in the same period of 2024 to 3.2%. An analyst from Morningstar predicted in the report that Samsung SDI will incur an operating loss of 398 billion KRW (approximately 2.06 billion RMB) in 2025, and has downgraded the company’s operating profit forecasts for 2026 to 2029 by 3% to 10%.

As the only Japanese battery manufacturer to rank among the global top ten, Panasonic secured sixth place with an installed capacity of 18.8 GWh. Although this represents a year-on-year increase of 14.4%, its market share fell from 4.5% in the same period of 2024 to 3.7%. Years ago, Panasonic once held the top spot in global power battery installations, owing to its superior cylindrical batteries as the exclusive supplier to Tesla.

Strategic Retrenchment and Adjustment

Facing multiple operational pressures and market challenges, Japanese and Korean battery manufacturers have initiated strategic business adjustments. For instance, LG Energy Solution announced at the beginning of this year that, due to a slowdown in the growth of the global electric vehicle market, the company decided to cut its annual capital investment by 30%. They also explicitly warned that due to changes in policy environments in key markets such as Europe and the United States, their annual revenue growth might significantly fall short of expectations.

In April this year, LG Energy Solutions announced that it would officially withdraw from an $8.45 billion (approximately 60.7 billion RMB) integrated battery industry investment project in Indonesia, ending the cooperation plan that had been in place since the cooperation agreement was signed in 2020. LG Energy Solutions stated that the decision to withdraw was a consensus reached after "comprehensively considering market conditions and the investment environment."

In May this year, according to foreign media reports, due to a slowdown in global electric vehicle demand, Panasonic adjusted the production plans of its battery factories. Panasonic Holdings CEO Yuki Kusumi stated that Panasonic will delay the construction of its third battery plant in the United States and focus on putting its second plant in Kansas into operation.

The Kansas plant is Panasonic's second-largest battery base in the U.S., with an expected investment of approximately $4 billion and a planned annual capacity of 30GWh. It was initially scheduled to begin full production in 2026. However, the latest news indicates that full production will be delayed until 2027 because Panasonic's key customer, Tesla, has seen sluggish sales of related models, prompting Panasonic to reassess its production plans.

It is worth noting that, as Japanese and Korean manufacturers have long focused on producing ternary batteries, the recent global popularity of lithium iron phosphate (LFP) batteries has forced them to adjust their product strategies. Companies such as LG Energy Solution, SK On, and Samsung SDI all hope to enter a broader market through LFP technology.

"Over the past five years, the market share of lithium iron phosphate batteries in the electric vehicle sector has increased by more than threefold. While providing a competitive range, the price of lithium iron phosphate batteries is about 30% cheaper than that of ternary lithium batteries," the International Energy Agency analysis indicates.

LG Energy Solution and its partner General Motors are reportedly upgrading their plant in Tennessee, USA, to convert the ternary production line to produce lithium iron phosphate batteries. SK On plans to mass-produce lithium iron phosphate batteries by 2026. Meanwhile, Samsung SDI has set up its first lithium iron phosphate battery production line at its plant in Ulsan, South Korea.

However, it is not easy for Japanese and Korean manufacturers to try to change their passive market position by focusing on lithium iron phosphate batteries. In this field, Chinese battery manufacturers not only have a leading technological advantage but also dominate in terms of capacity, cost, and supply chain. Moreover, Japanese and Korean manufacturers are also less efficient than Chinese manufacturers in production line expansion.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)