Layoffs of 2,000! Three Major Giants Retreat Again!

Recently, there have been reports of asset sales and layoffs from the three major giants. If the transactions/plans are implemented, they will collectively secure approximately 11 billion yuan in substantial gains, while 2,000 people will be affected.

I. Dow

On September 2nd, Dow announced that it had sold a portion of its infrastructure joint venture shares to its partner Macquarie Asset Management for $540 million. Currently, Dow is focusing on further developing its core business. Not long ago, Dow also announced its exit from another joint venture, DowAksa, abandoning its carbon fiber business.Dow, exit!

It is reported that this transaction is a further step by Dow to evaluate the ownership of non-product-producing assets in its global investment portfolio. It follows Dow's sale of a 40% stake in certain infrastructure assets along the U.S. Gulf Coast to Macquarie at the end of 2024 (part of a previously reached agreement), which will increase Macquarie's stake in the Diamond Infrastructure Solutions joint venture to 49%, thereby raising Dow's total proceeds from the transaction from $2.4 billion to approximately $3 billion.

It is reported that Dow will not completely withdraw from this business; the company will retain its controlling stake in Diamond Infrastructure Solutions to ensure the continuity of safe and reliable operations.

From a business perspective, Dow operates three main business units, primarily involving ethylene and its downstream products, epoxy resins, polyurethanes, acrylic acid and esters, as well as organosilicon product chains.

Diamond Infrastructure Solutions is the infrastructure provider for Dow and its five plants located in Texas and Louisiana, USA. It comprises certain non-product production assets (power and steam generation, pipelines, environmental operations, and general site infrastructure) at Dow’s five manufacturing sites along the U.S. Gulf Coast (USGC): Freeport, Texas City, and Seadrift in Texas, as well as Plaquemine and St. Charles in Louisiana. Pipeline and storage assets are distributed across the U.S. Gulf Coast, connecting to major natural gas, NGL, and olefin hubs.

2. OMV

On September 4th, according to the Austrian newspaper Kurier, the Austrian oil, gas, and chemical group OMV plans to cut 2,000 of its 23,000 employees worldwide.

The report, citing union sources, states that the company's Romanian subsidiary, Petrom, will be particularly hard hit, and its refineries in southern Germany and Slovakia also plan to lay off employees. According to the report, about 400 of the 5,400 positions in Austria will be cut, and the company plans to "demonstrate social awareness as much as possible" during the layoff process.

However, the business merger plan of OMV's chemical subsidiary, Borealis, will not be affected.

On March 4, 2025, Abu Dhabi National Oil Company (ADNOC) and OMV reached a binding framework agreement on the proposed equity merger of Borouge and Borealis. The latter two companies are expected to merge into Borouge Group International in the first quarter of 2026, simultaneously acquiring Nova Chemicals, forming a leading new polyolefins company valued at over 60 billion USD and ranked fourth globally. This move will further expand their business footprint in North America. Currently, Borealis is already among the top ten global polyolefin producers and a leader in the European market for basic chemicals and plastics recycling.

3. ExxonMobil

On September 4th, according to the Financial Times citing informed sources, ExxonMobil is seeking to sell its European chemical plants located in the UK and Belgium due to the industry being affected by US tariffs and competition from China. The sale amount could be as high as $1 billion. ExxonMobil did not immediately respond to external requests for comment.

It is reported that due to U.S. tariffs disrupting global trade, causing order delays, and intensifying competition from cheap Asian imports, the European chemical industry is facing new pressures, threatening the sector’s recovery that is still affected by the 2022 energy crisis. ExxonMobil owns an ethylene plant in Fife, Scotland, and has multiple production sites in Belgium. The report states that the company has also discussed the direct closure of these plants.

There is currently no definitive conclusion regarding these reports, and ExxonMobil may choose to retain these assets. It is worth noting that in May of this year, ExxonMobil entered into exclusive negotiations with the French subsidiary of North Atlantic, a Canadian energy group, to divest its majority stake in its French subsidiary, Esso.

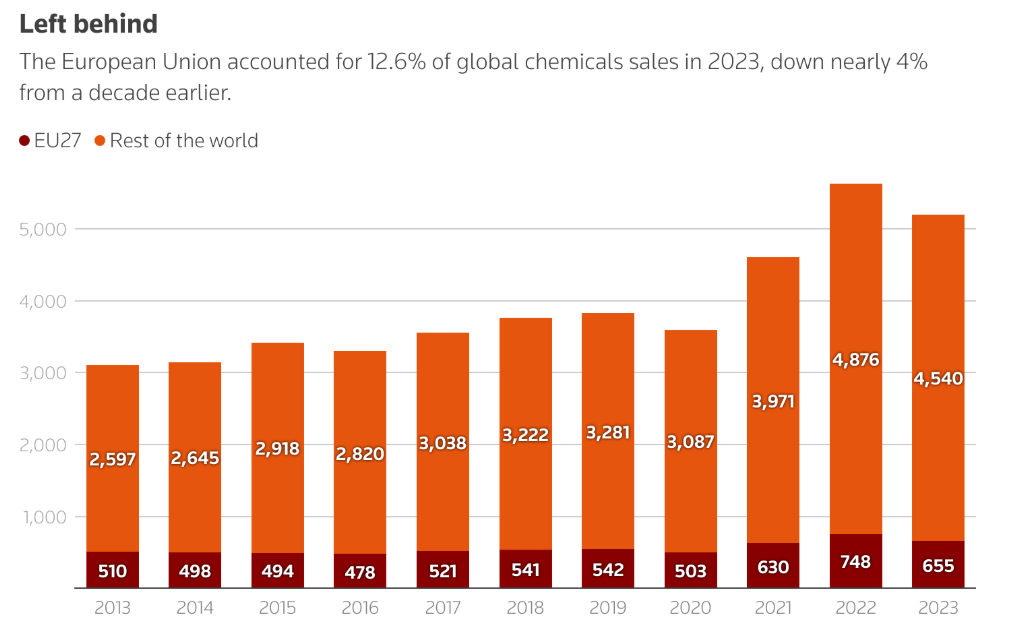

However, considering the current situation of gradual deindustrialization in Europe, it is not surprising if ExxonMobil continues to "withdraw." (As shown in the figure below, the sales of chemical products in the EU region show signs of decline.)

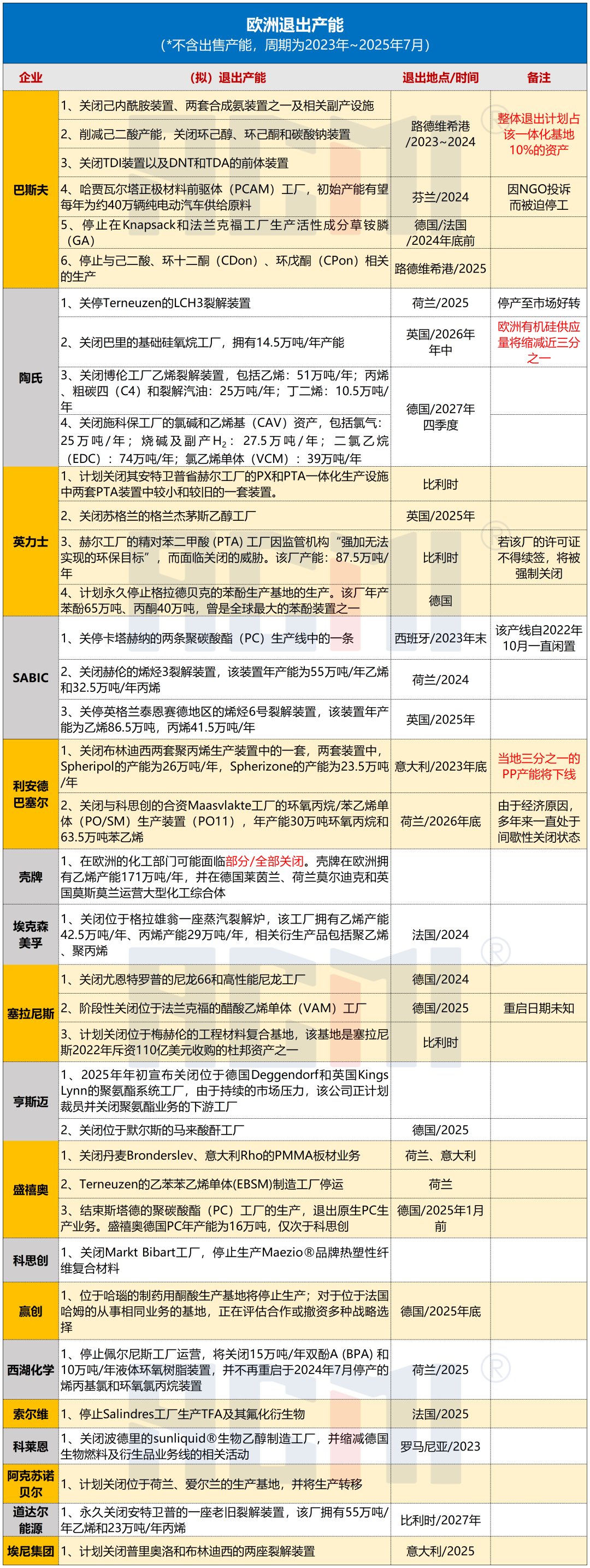

According to incomplete statistics, since 2023, major companies including BASF, Dow, Evonik, Huntsman, Celanese, INEOS, Covestro, SABIC, LyondellBasell, ExxonMobil, AkzoNobel, Shell, and TotalEnergies have been gradually “withdrawing” from Europe.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)