JDI Embraces Dan-Sha-Li! Abandoning a Decade-Long Apple Aura, Can the Shift to Automotive Displays Restore Its Glory?

Japan Display (JDI), which has fallen into financial difficulties, recently announced that it will close its Mobara plant in Chiba Prefecture and sell its LCD and OLED production equipment, including the production line that has long supplied the Apple Watch. This not only signifies JDI's official exit from the smartwatch display panel market but also marks the end of its decade-long partnership with Apple.

However, JDI's move is not merely a contraction, but a structural adjustment that bets on the future: shifting from a capital-intensive panel manufacturer to a fabless model, and concentrating resources on new fields such as automotive panels and sensors. Is this transformation JDI's redemption, or just another unfinished dream? This must be analyzed from two major challenges and one key opportunity.

JDI Selling Factories to Survive: The Inevitability and Risks of Transitioning to Fabless

JDI's financial difficulties did not arise overnight. Over the past decade, JDI has been overly reliant on orders from Apple. Although it once grew rapidly due to the explosive demand for iPhones, JDI gradually lost its competitiveness as OLED replaced LCD, having clearly fallen behind in technological investment. In particular, the long-term leadership of Samsung and LG Display in the OLED sector further pushed JDI into trouble, ultimately forcing it to sell assets in exchange for cash.

However, it is not entirely impossible for JDI to shift to a fabless model. In fact, there are already successful cases in the semiconductor industry, such as TSMC, proving that a design-focused, outsourced manufacturing model is feasible. However, it should be noted that the panel industry is different from the semiconductor industry; its manufacturing technology and mass production scale rely more heavily on the accumulation of process experience. Without its own factories, JDI will lose the advantage of experimental technology verification, which may prolong product development cycles. This is the greatest uncertainty in its transformation process.

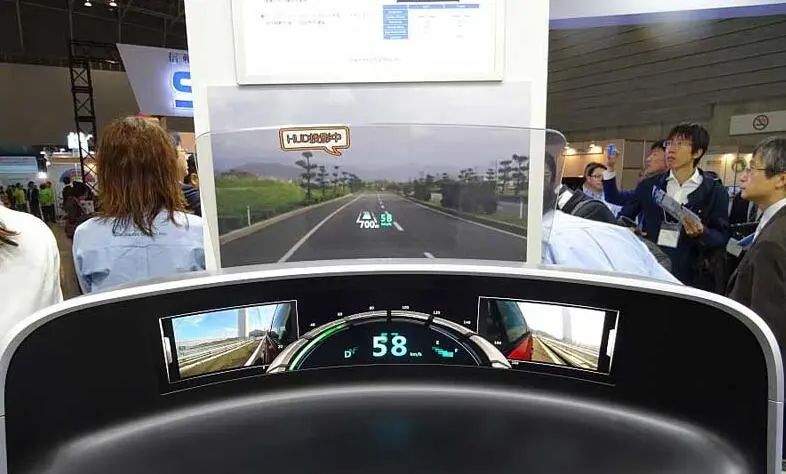

Automotive Panels and Sensors: JDI's New Battlefield

After JDI exited Apple's supply chain, it chose to focus on the automotive display and sensor markets, which is a pragmatic strategic shift. Although the automotive display market does not grow as rapidly as the smartphone market, it is highly stable. With the proliferation of electric vehicles and smart cockpits, the demand for high-end displays and sensing components continues to increase. According to data from a Japanese research institution, the global automotive display market has a compound annual growth rate of approximately 6-8%. For resource-limited JDI, this is a relatively controllable blue ocean market.

However, automotive displays are not without competitive pressure. Manufacturers such as Sharp and Innolux have been established in the field for many years, and automotive displays require extremely high standards for long-term supply stability and durability. This means that JDI not only needs to possess strong technological capabilities but also has to rebuild customer trust. On the other hand, JDI’s investment in the sensor field, if combined with its advantages in low-power display technology, may provide an opportunity to establish differentiated advantages with automakers and in the industrial control sector. This will be key to whether it can make a comeback in the future.

Structural Reorganization and Capital Cooperation: JDI’s Last Stand

The fate of JDI is not an isolated case but rather a reflection of the structural transformation of Japan's electronics industry. In the 1980s, Japan's electronics industry dominated globally in areas such as displays, semiconductors, and home appliances. However, with the acceleration of globalization and the IT cycle in the 1990s, Japanese companies gradually fell into three structural dilemmas: first, overly conservative technical decisions, often commercializing on a large scale only after the technology matured, which avoided burning money but allowed Korean and Taiwanese companies to surpass them through aggressive investments; second, insufficient capital support, as compared to the direct support of the South Korean government for Samsung and LG, Japan's industrial capital was dispersed, lacking the power to drive large-scale investments; third, over-reliance on vertical integration, which emphasized an all-in-one system from materials to manufacturing but lacked flexibility in a rapidly changing market, making it difficult to respond to emerging application demands.

JDI was established in 2012 through the merger of the panel divisions of Sony, Toshiba, and Hitachi amid these structural issues. Originally expected to integrate resources to compete against South Korea and China, it ultimately missed the opportunity for further expansion through cooperation with Apple due to delayed decisions on OLED transformation and insufficient capital. JDI's transformation is not only a technical and market challenge but also a capital battle. Over the past few years, JDI has repeatedly received capital injections from INCJ (Innovation Network Corporation of Japan). Now, by selling the Mobara factory and production equipment, whether the funds obtained can effectively support its transformation period is the key to success or failure.

The significance of this transformation for Japan's display industry

JDI's sale of panel equipment and the end of its partnership with Apple may seem like a sign of failure, but it is more likely an opportunity for rebirth by cutting losses to survive. Automotive panels and sensors are indeed predictable growth markets, but JDI must quickly establish technological differentiation without its own factories and strive for support from the government and the industry chain.

This is a high-risk but necessary bet. If JDI can precisely focus during its transformation and fully leverage the synergy of the Japanese industrial chain, it may still have a chance to return to the center stage in the next decade. Otherwise, this transformation is likely to be another missed opportunity for Japan's display industry.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)