In the second quarter, many polypropylene maintenance shutdowns are coming. Which company has the longest downtime?

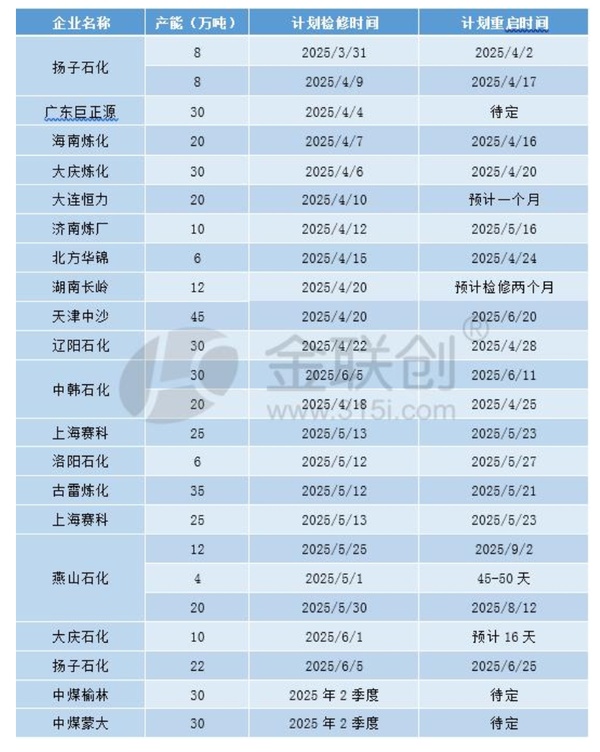

In the second quarter, the overall domestic polypropylene maintenance plans are concentrated, with the total capacity of the facilities reaching 5.02 million tons. Companies such as Yanshan Petrochemical, Tianjin Zhongsha, Zhongmei Yulin, and Zhonghan Petrochemical have maintenance plans, and the maintenance duration is relatively long, which somewhat offsets the supply pressure.

In the second quarter, new maintenance facilities concentrated in Northeast China, accounting for 19.67% of the national total, followed by North China and Northeast China, which accounted for 18.65% and 18.03%, respectively. In the Northeast region, this is mainly due to maintenance plans for facilities such as Daqing Refining & Chemical and Liaoyang Petrochemical, with a total maintenance capacity reaching 960,000 tons; in North China, facilities such as Yanshan Petrochemical, Tianjin Zhongsha, and Jinan Refinery also have maintenance plans, totaling 910,000 tons. Overall, the differences in proportions among regions are not significant, and the overall number of maintenance facilities in the second quarter is relatively high, indicating that supply pressure is expected to ease.

In the second quarter, with the expected commissioning of facilities such as Yulong Petrochemical and ExxonMobil's Huizhou project, production capacity will reach 3.3 million tons, leading to increased supply pressure. However, concentrated maintenance by enterprises in the second quarter may somewhat offset this supply pressure. On the demand side, the traditional operating rates for plastic weaving and plastic film are rising, and favorable policies for the home appliance and automotive industries in the second quarter will further boost demand. Additionally, macroeconomic favorable policies, including continuous easing of monetary policy with expected reserve requirement cuts and interest rate reductions of 1-2 percentage points for the year, will support demand. However, in the second quarter, OPEC+ will gradually restore 2.2 million barrels per day of voluntary production cuts (originally scheduled to expire at the end of March), coupled with rapid increases in crude oil production from South American countries like Brazil and Guyana. The supply and demand situation is expected to tighten first and then loosen in the second quarter, which may lead to a short-term rebound, but the overall outlook remains bearish. The destocking speed in the second quarter is constrained by the slow recovery of terminal demand, and some enterprises may resort to price reductions and promotions to alleviate pressure. Market participants are generally cautious about the overall recovery of demand and are pessimistic about future market trends. Overall, it is expected that the PP market will have limited upward momentum in the second quarter, primarily operating in a weak manner.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift