Germany's Chemical Industry Hits Bottom as Production Capacity Utilization Falls to Historic Lows; Local Plastic Market Sees Fluctuations, EVA Surges by 400

I. Germany's chemical industry is mired in crisis, with capacity utilization falling to a historic low.

Germany's chemical industry is the backbone of the "Northwest European Industrial Corridor": the "Golden Triangle" of Ludwigshafen, Leverkusen, and Frankfurt along the lower Rhine contributes nearly 80% of the country's capacity. Global giants such as BASF (the world's largest chemical company) and Bayer are gathered here, and the production, supply, and sales of specialty chemicals, pharmaceutical intermediates, and high-performance materials all emanate from this region.

According to recent data released by the German Chemical Industry Association (VCI), by the second quarter of 2025, Germany's chemical industry experienced a significant recession: the industry's capacity utilization rate plummeted to 71%, and the current production level has fallen to the lowest point since the reunification of Germany in 1991. Similar to the capacity surplus caused by the integration of East German factories back then, the industry is once again in a severe predicament. Meanwhile, the high tariffs policy upheld by the United States has continued to elevate market uncertainty.

A capacity utilization rate of 71% means that most factories are unable to make a profit (the profitability threshold set by VCI is around 82%). German chemical giants such as BASF, Covestro, and Lanxess are likely to continue reporting losses in their German operations in 2025—similar to previous years, these companies rely almost entirely on overseas markets like Asia and the United States to sustain overall profitability.

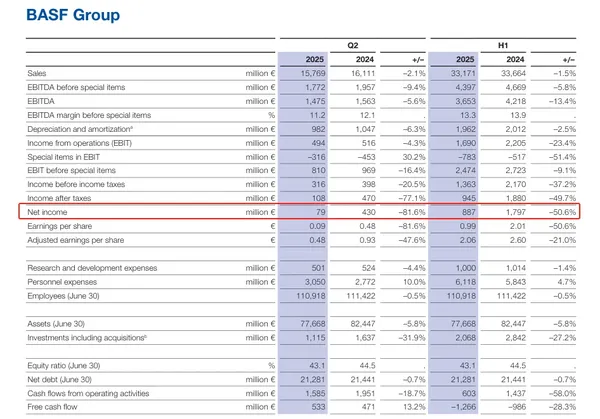

BASF 2025 First Half-Year Performance

In the first half of the year, sales amounted to 33.2 billion euros, a decrease of 1.5% year-on-year; EBITDA was 3.7 billion euros, a decline of 13.4% year-on-year; net income was 887 million euros, down 50.6% year-on-year.

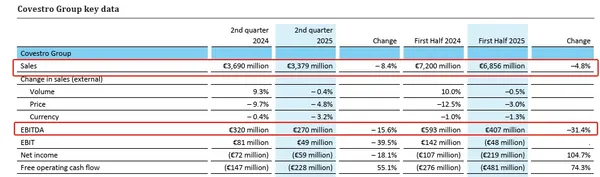

Covestro's performance in the first half of 2025.

Sales in the first half of the year reached 6.9 billion euros, down 4.8% year-on-year; EBITDA was 407 million euros, down 31.4% year-on-year.

LANXESS Q2 2025 Results

In the second quarter, sales amounted to 1.466 billion euros, a year-on-year decrease of 12.6%; EBITDA was 150 million euros, down 17.1% year-on-year. Overall weak demand led to a decline in sales across all business units. Meanwhile, Lanxess announced further plans for shutdown and reduction, including the early closure of the hexane oxidation plant in northern Germany (moved up from 2026 to the end of the second quarter of 2025) and the closure of a specialty chemicals plant in Europe.

Germany's domestic production has declined again, with a year-on-year drop of 5% in the second quarter of 2025, while order backlogs in early August hit their lowest level since 2009, sounding a fundamental alarm for the chemical industry. Meanwhile, over the past two years, BASF, Dow, INEOS, Celanese, and Huntsman have successively shut down plants. As experts have stated, "The brief hope for economic recovery driven by the chemical industry has been completely shattered."

The chemical industry is regarded as an economic barometer, with its global influence covering almost all manufacturing sectors. However, the current reality is not optimistic.

At the same time, in terms of policy, chemical companies are facing significant uncertainties, which is also a negative signal for the overall situation. Evonik CEO Christian Kullmann mentioned in an interview that if U.S. policies continue to fluctuate, economic uncertainty will inevitably increase. This specialty materials giant expects its adjusted EBITDA for the full year of 2025 to be at the lower end of the forecast range (€2 billion to €2.3 billion) — but only if the global economy does not weaken further.

II. Today's Latest Plastic Prices

(The above is compiled from Chemical New Materials and Dayi Yosu.)

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)