Downstream Operating Rate Increase Expected to Ease Fundamental Pressure, Polyethylene May Rise Slightly in August

[Introduction]: 7 Under the dual constraints of monthly supply and demand contradictions, and with some relief in market pressure from the macro side, polyethylene prices experienced a slight decline. The average monthly price of mainstream LLDPE film in North China was 7,205 yuan/ton, down 0.22% month-on-month.In August, the polyethylene market is expected to see a slight price increase as the fundamental pressure eases amid improved downstream operating rate expectations.

One, The supply side continues to exert pressure and downstream operation rates are declining, leading to a narrow downward trend in polyethylene prices.

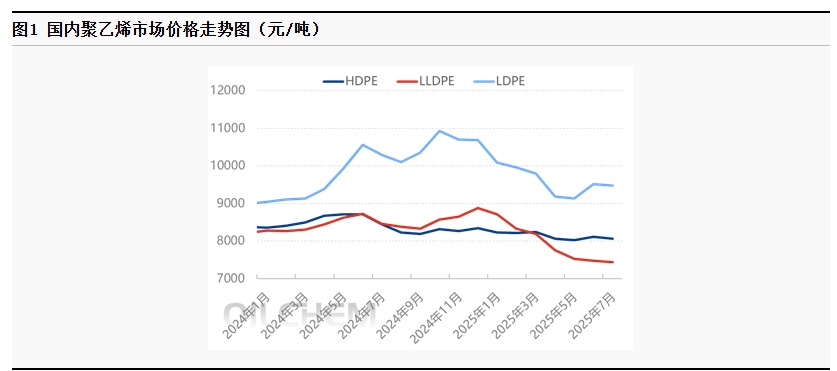

7 Domestic polyethylene prices fell in the month.

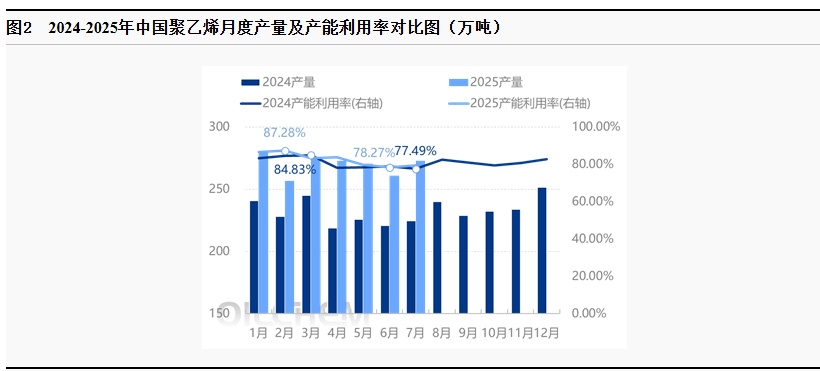

In July, with the commissioning of Jilin Petrochemical's new 400,000-ton/year plant, polyethylene production capacity reached 39.14 million tons. In terms of output, it increased by 4.48% month-on-month to 2.7264 million tons in July. The inventory of social sample warehouses rose by 10.77% to 561,700 tons, exerting pressure on the polyethylene market from the upstream supply side.

On the downstream side, by the end of July, the overall average operating rate of downstream PE industries dropped to 38.3%, down 0.4% from the previous month and 2.76 percentage points year-on-year, setting a record low for the same period in history.

However, on the macro level, the new round of policies for eliminating outdated production capacity released in mid-month offset part of the impact from fundamentals. Overall, under the dual constraints of supply and demand contradictions in July, and with some alleviation of market pressure from the macro side, polyethylene prices declined within a narrow range. By the end of the month, the average monthly price of mainstream LLDPE film in North China was 7,205 yuan/ton, down 0.22% month-on-month.

2. Newly commissioned enterprises within the month led to a 4.48% month-on-month increase in output.

In July, the domestic maintenance loss volume increased, with the loss volume month-on-month at -2.03% to 506,700 tons. Among them, the maintenance volume of low-voltage varieties decreased by 5.6% month-on-month, the maintenance volume of high-voltage varieties decreased by 1.84% month-on-month, and the maintenance volume of linear varieties increased by 5.04% month-on-month. The maintenance impact volume of low-voltage was 278,000 tons; the maintenance impact volume of high-voltage was 74,500 tons; and the maintenance impact volume of linear types was 154,200 tons.

7 Monthly New Polyethylene Production Units

In July, domestic polyethylene production reached 2.7264 million tons, a month-on-month increase of 4.48%. The capacity utilization rate rose by 1.16 percentage points month-on-month to 79.43%.

3.The operating rate downstream fell to 38.3% on a week-on-week basis.

In July, the operating rate of domestic downstream polyethylene was 38.3%, a month-on-month decrease of 0.4%.

In July, the overall operating rate of agricultural film increased by 0.1% month-on-month. The agricultural film industry continued to exhibit typical off-season characteristics in July, with overall performance remaining sluggish. Although the demand for greenhouse films slowly started to pick up, the increase in orders was less than that of the same period in previous years. Only a few large-scale enterprises saw a slight rise in operating rates, while small and medium-sized enterprises mainly engaged in intermittent production. The traditional off-season for mulch films saw most enterprises choosing to halt production for maintenance, except for a few that maintained sporadic order-based production.

Overall, the current agricultural film market exhibits clear seasonal characteristics. In July, the operating rate of agricultural film saw only a slight increase compared to June, and the market's recovery still awaits a seasonal demand turning point. The average operating rate of PE packaging film in July decreased by 0.23% month-on-month. This month's operating level mainly experienced slight and temporary fluctuations. Affected by demand, most companies supplemented with short-term orders, concentrating production on already received orders, with limited new orders coming in. 。

Section Four Translate the above content into English and output the translated result directly without any explanation.Polyethylene prices are expected to rise slightly in August.

Domestic PE market prices in August are expected to rise within a narrow range.

The polyethylene capacity utilization rate in August is expected to decrease by 0.79% to 78.64%. Despite the ramp-up of newly commissioned enterprises, output is only expected to increase slightly by 0.03% to 2.7271 million tons, showing little change compared to July. Exports are expected to decrease by 4.4% to 87,000 tons, while the total domestic market supply is projected to increase by 0.34% compared to July.

In terms of demand, it is expected that the overall average operating rate of downstream industries will increase by 2% to 40.3% in August. For agricultural films, the mid-to-late period will enter the "Golden September and Silver October" stocking season. This year, coupled with macro policy stimulus, the timing and strength of demand initiation are particularly crucial. The operating rate of agricultural films is expected to increase by 5.5%, while packaging films are expected to rise by 2.5%.

Overall, with the expectation of improved downstream operating rates in August, the fundamental pressures on the polyethylene market are expected to ease, and prices may rise within a narrow range. It is estimated that the average price of LLDPE in the North China market will be around 7,290 yuan/ton in August, 7,450 yuan/ton in September, and 7,520 yuan/ton in October. 。

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift