After €800 million loss, german chemical giant wacker bets on pace cost-cutting plan to navigate industry downturn

Image source: Wacker Chemie

Recently, German specialty chemicals giant WACKER released its fiscal year 2025 financial report, revealing the challenging conditions facing the global chemical industry amid a complex environment: annual sales declined by 4.1% year-over-year to €5.49 billion, and the company reported a net loss of €805 million—the worst performance in recent years. WACKER also announced the suspension of its dividend payout for fiscal year 2025. However, beneath this earnings pressure, the company's "PACE" cost-reduction program and strategic shift toward premium markets are quietly gaining traction, laying the groundwork for a recovery in 2026. This article will provide an in-depth analysis of WACKER's financial challenges, strategic realignment, and growth potential, contextualized within broader industry dynamics and detailed financial data.

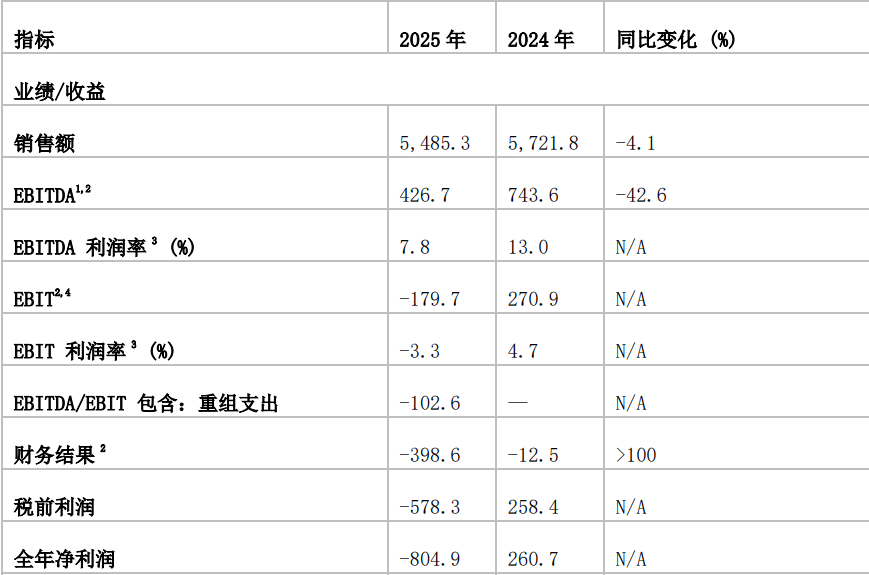

Table Wacker Group 2025 Key Financial Data (Unit: Million Euros)

I. Performance Under Pressure: A Financial Review Amid Multiple Headwinds

In 2025, the global chemical industry faced a triple blow of weak demand, high costs, and intensified competition, and Wacker's declining performance was a reflection of this industry trend.

From the perspective of core financial metrics, Wacker’s operational performance in 2025 exhibits a “three-declines-one-increase” pattern. On the revenue side, group sales declined from €5.72 billion in 2024 to €5.49 billion in 2025, a 4.1% year-on-year decrease, with none of the four business segments achieving growth. Profitability deteriorated even more sharply: EBITDA plummeted 42.6% year-on-year to €427 million; even after excluding restructuring and other special items, it still fell 29% to €529 million. EBIT swung from a profit of €271 million in 2024 to a loss of €180 million in 2025; the group recorded a full-year net loss of €805 million, a stark contrast to the €261 million net profit in the prior year.

The expansion of losses stems from the convergence of multiple adverse factors. On one hand, weak market demand has led to declines in both sales volume and prices; delayed investments by downstream industries such as automotive and construction have resulted in insufficient capacity utilization for core products, including silicones and polymers. On the other hand, persistently high energy costs in Germany have further squeezed profit margins, becoming a significant driver of declining profitability. Notably, asset impairments and restructuring expenses have emerged as key drags on performance: in 2025, the company recognized total valuation adjustments amounting to approximately €600 million, including a €308 million write-down of its shares in Siltronic AG, a €194 million reversal of deferred tax assets, an €89 million goodwill impairment arising from the acquisition of Spanish ADL Biopharma, and €103 million in restructuring expenses under the “PACE” program—collectively causing a substantial net loss.

From a financial structure perspective, Wacker’s capital position is also under pressure. As of the end of 2025, the Group’s total assets declined by 11% year-on-year to €8.37 billion, shareholders’ equity decreased by 22.4% to €3.76 billion, and the equity ratio fell from 51.4% to 44.9%; net financial liabilities rose to €886 million, an increase of 28.3% year-on-year. Nevertheless, the company achieved a certain degree of mitigation through precise cash-flow management: in 2025, net cash flow was nearly balanced (–€4 million), a significant improvement compared to –€326 million in the prior year, while holding €1.48 billion in liquid funds, providing financial support for cost reduction and transformation initiatives.

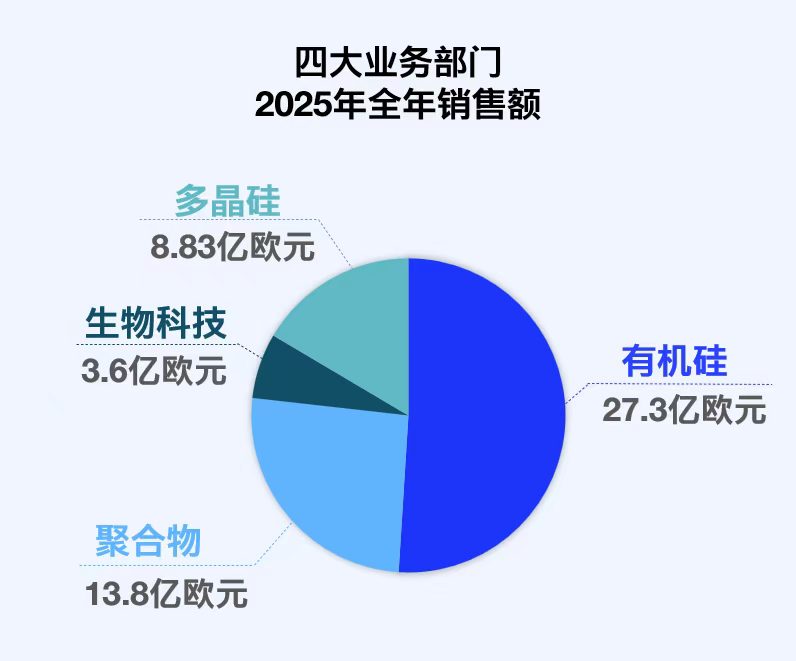

II. Divergence Across Four Major Segments; the Premium Market Becomes the Key to Breakthrough

All four business segments of Wacker (silicones, polymers, biotechnology, and polysilicon) face growth pressures in 2025, but their performance shows significant divergence, with high-end products and emerging market strategies serving as important barriers against industry cycles.

Image source: Wacker Chemie

Organosilicon business, as the Group's largest revenue source, in 2025Annual sales slightly declined by 3%.Up to 27.3Billion euros, EBITDAThen basically maintained the level of the previous year (3.36)1.3 billion euros, demonstrating strong business resilience.This performance stems from the company's deep expertise in specialty silicones. In 2025, Wacker expanded its specialty silicone capacity in Zhangjiagang, China, and Tsukuba, Japan. These high-value-added products effectively offset the price decline of standard products. However, an unfavorable product mix, currency fluctuations, and low capacity utilization continued to constrain earnings, preventing growth in this segment.

The property management business has been most significantly impacted by the weakness in demand from the construction industry, with sales declining by 6%.To 13.8Billion euros, EBITDADecline by 19%Up to 1.58billion euros.

The biotechnology business also faces challenges in 2025.Annual sales decreased by 4%.Up to 3.6Billion euros, EBITDAFrom 3500Euro significantly depreciated to 2100Euro, mainly due to the decrease in sales of mature products and a decline in customer orders. However, the company's new Wacker Biotech Center in Munich, scheduled to be officially launched in mid-2025, will provide support for the research and development of innovative biotech solutions, serving as a potential driver for future growth in this sector.

Polysilicon business shows "Polarizationdevelopment trend, 2025Year sales decreased by 7%Up to 8.83Billion Euros, EBITDAContract by 50%To 960010 million euros.Among them, solar-grade polysilicon has seen a significant drop in sales due to industry overcapacity, becoming the main reason for the decline in the sector's performance; while the semiconductor-grade polysilicon business performed outstandingly. After the new cleaning line at the German Burghausen plant came into operation, the capacity of ultra-high-purity semiconductor-grade polysilicon increased by more than 50%, and the purity level was further improved, fully benefiting from the continuous growth of the semiconductor industry, laying the foundation for the recovery of the sector.

In terms of regional markets, Wacker faces challenges from uneven regional demand due to its global footprint.In 2025, sales in the Asian market declined by 9% to 1.92 billion euros, and in the American market, they fell by 5% to 1.02 billion euros, with only the European market remaining largely stable at 2.22 billion euros. As the world's largest producer and consumer of chemical products, the slowdown in demand from the Chinese market has significantly impacted Wacker, which also underscores the urgency of "expanding demand in emerging industries" as outlined in the Stable Growth Work Plan for the Petrochemical and Chemical Industry.

Image source: Wacker Chemie

III. PACECost Reduction and High-end Transformation Double-wheel Drive

In the face of an industry downturn, Wacker did not passively defend but launched its largest-ever "PACE" cost reduction program while simultaneously advancing the high-end transformation of its business structure, forming a development strategy driven by both "cost-saving" and "revenue-generating" initiatives.

While controlling costs, Wacker is accelerating the high-end transformation of its business structure, focusing on high-value-added markets. The company has clearly defined three strategic directions: its chemical business focuses on specialty products; its polysilicon business targets the semiconductor market; and its biotechnology business is dedicated to biotech solutions.This transformation pathway closely aligns with the policy orientation outlined in the “Stable Growth Work Plan for the Petrochemical and Chemical Industries,” which emphasizes “accelerating high-end upgrades and avoiding low-level repetitive construction.” At the implementation level, Wacker’s new factory for high-performance room-temperature-curing silicone materials in the Czech Republic, its expansion of semiconductor-grade polysilicon production capacity, and the enlargement of its specialty silicone production base—though collectively resulting in a 34% year-on-year decline in capital expenditures to €466 million in 2025—represent highly focused investments in advanced manufacturing, laying a solid foundation for long-term growth.

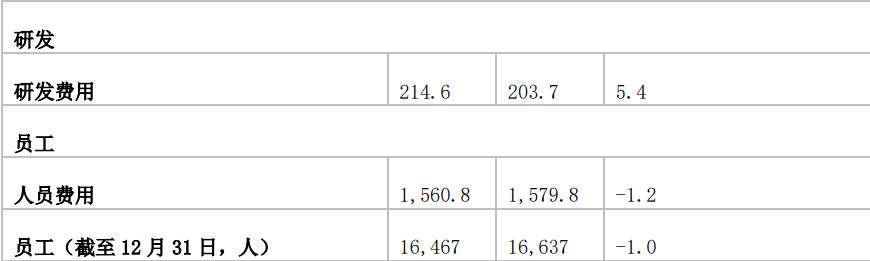

The continuous increase in R&D investment has become an important guarantee for supporting the transformation. In 2025, Wacker's R&D expenses increased by 5.4% year-on-year to 214.6 million euros. In the context of declining sales, the proportion of R&D investment further increased. Through technological innovation, the company maintains a technological lead in areas such as semiconductor-grade polysilicon and specialty silicones, providing support for product premiums. This is also the key reason why the EBITDA of the silicone business remained basically stable despite a decline in sales.

IV. 20262024 Outlook: Recovery is Expected but Challenges Remain

Based on the advancement of the “PACE” cost-reduction program and the expansion into high-end markets, Wacker is cautiously optimistic about its 2026 performance, expecting full-year sales to grow by a low single-digit percentage and EBITDA to range between €550 million and €700 million—marking a clear recovery compared to 2025.

By business segment, sales of the silicone and polymer businesses are expected to remain flat year-on-year, but EBITDA margin is anticipated to be slightly higher than last year, primarily driven by volume growth, selective price increases, and cost-reduction initiatives; adverse currency impacts will partially offset these gains. The biotechnology business is expected to achieve high-single-digit percentage sales growth, with EBITDA recovering to €0.3 billion. The polysilicon business is the most promising segment: sales are projected to grow in the low double-digit percentage range, with a significant increase in semiconductor-grade polysilicon volumes serving as the key growth driver; however, the solar-grade polysilicon business will continue to face challenges, and rising energy costs will pressure profitability, resulting in EBITDA remaining flat year-on-year versus 2025.

From an industry perspective, Wacker's path to recovery is highly correlated with the development trends of the global chemical industry. As the high-end and green transformation becomes a consensus in the industry, Wacker's strategic focus on specialty products and the semiconductor market is timely, and it is well-positioned to seize the initiative in the industry's recovery process.

V. Transformation Pains and Long-Term Value Amidst the Winter Chill

Editor: Lily

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Raw Material Supply Shortage! INEOS Phenol Declares Force Majeure on Phenol and Acetone Businesses

-

Lantiche Group To Shut Down Italian Adipic Acid Production Plant

-

Resin Market Trends Diverge: Buyers' Bargaining Advantage Hit by Geopolitical Uncertainty

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Strait of Hormuz Blocked Again, Supply-Demand Mismatch in Polyolefin Market Set to Intensify!