$520 Million Market! Global Mono-Oriented Polypropylene (MOPP) Film Industry

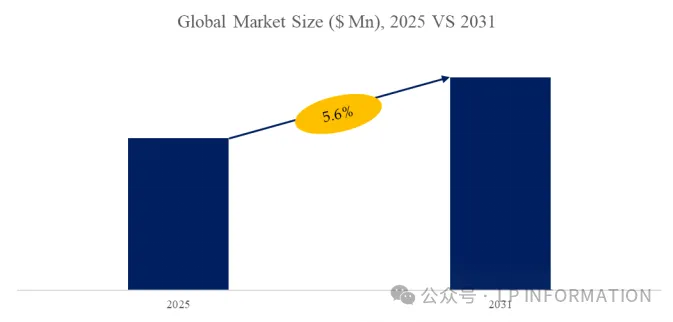

According to the US market research publisher LP Information, the global Mono-Oriented Polypropylene (MOPP) film market is expected to reach USD 520 million by 2031, with a compound annual growth rate (CAGR) of 5.6% in the coming years.

Figure 00001. Global Market Size of Monoaxially Oriented Polypropylene (MOPP) Film

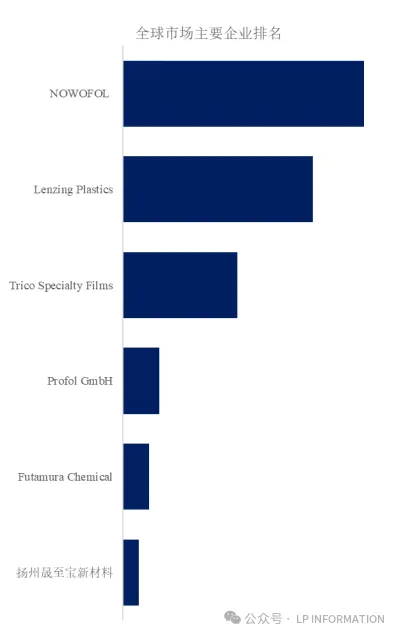

Figure 00002. Top 6 Global Manufacturers of Mono-Oriented Polypropylene (MOPP) Films and Their Market Shares (Based on 2024 Survey Data)

Major global manufacturers of mono-oriented polypropylene (MOPP) films include NOWOFOL, Lenzing Plastics, Trico Specialty Films, Profol GmbH, Futamura Chemical, and Yangzhou Sheng Zhibao New Materials. In 2024, the top five manufacturers worldwide accounted for approximately 59.0% of the market share.

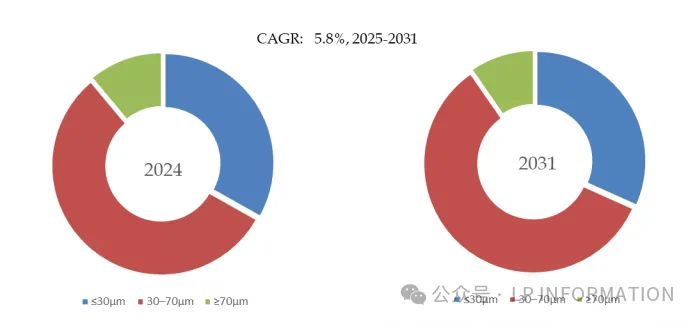

Figure 00003. Global Market Size of Mono-Oriented Polypropylene (MOPP) Films, by Product Type, with 30–70μm Segment Dominating

In terms of product type, the 30–70μm segment is currently the main product category, accounting for approximately 55.8% of the market share.

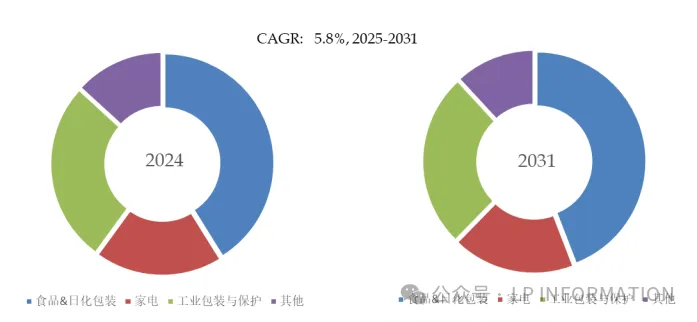

According to Figure 00004, the global market size of mono-oriented polypropylene (MOPP) films is segmented by application, with food & consumer goods packaging being the primary source of demand, accounting for approximately 41.1% of the share.

In terms of product application, food and daily chemical packaging is currently the primary source of demand, accounting for approximately 41.1% of the share.

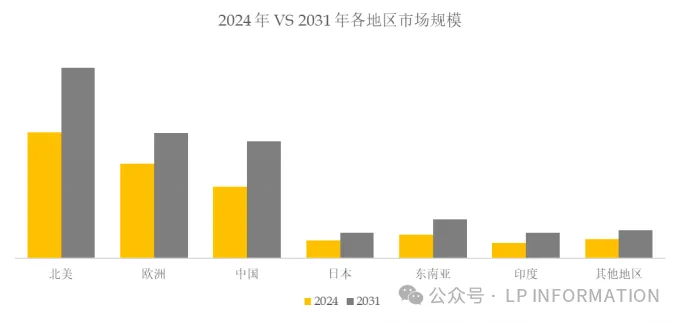

Figure 00005. Global Mono-oriented Polypropylene (MOPP) Film Scale, Major Regional Share

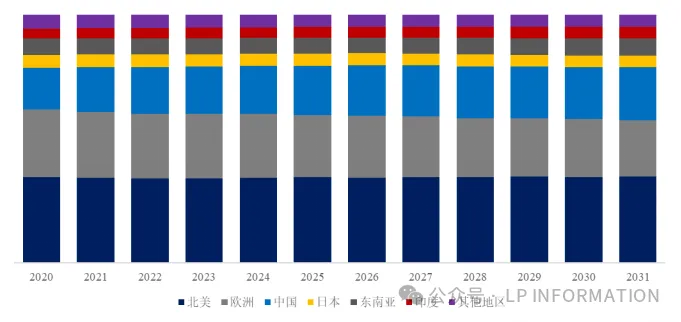

Figure 00006. Global Major Market Single-Oriented Polypropylene (MOPP) Film Scale

Main driving factors:

The mono-oriented polypropylene (MOPP) film industry is ushering in structural growth opportunities, especially against the backdrop of rising global demand for green packaging and functional materials. With increasing requirements for high-strength, easy-to-process, and environmentally friendly film materials in downstream sectors such as food packaging, labeling, home appliance protection, and industrial consumables, MOPP films are gradually replacing traditional materials in specific applications due to their superior longitudinal tensile strength, excellent stiffness, and good printability. The global market is transitioning from stability to growth, particularly in emerging regions like the Asia-Pacific, where MOPP film consumption is rapidly expanding and becoming a key driver of industry growth.

Currently, single-material plastic packaging films worldwide mainly focus on polyethylene and polypropylene. In developed regions such as Europe and the United States, concerns about recycling efficiency and environmental impact have placed policy and market pressures on traditional multilayer composite materials. In contrast, polypropylene-based single-material packaging, such as MOPP films, offers outstanding environmental advantages. Its simple structure and clear recycling pathways promote effective waste reutilization and drive the circular economy, significantly reducing the carbon footprint. It is a key direction for the future upgrade of sustainable packaging materials.

The development of the MOPP film market is being accelerated by policies and regulations. The European Union has introduced a revision of the Packaging and Packaging Waste Regulation (PPWR), and China is continuously advancing its action plan for managing plastic pollution. Both are advocating for packaging materials to be more environmentally friendly, functional, and easy to recycle. In this trend, MOPP films, which offer higher mechanical performance and environmental adaptability, are becoming a potential alternative in many brands' green material strategies. With improvements in process technology, optimization of raw materials, and expansion of application fields, MOPP films are expected to achieve technological breakthroughs, expand their market share in flexible packaging and industrial films, and enter a period of rapid growth.

Main obstacles:

One of the main challenges faced in the manufacturing of MOPP films is the high complexity of process control. Machine Direction Orientation (MDO) can significantly improve the film’s barrier properties, rigidity, flatness, and tensile strength, but it is very difficult to master in actual operation. For example, in multilayer films containing nylon or EVOH, although stretching can enhance barrier performance, it can also make the material brittle. Therefore, without precise control of process parameters such as preheating temperature, stretching ratio, and annealing position, product instability or deterioration of physical properties is highly likely to occur. This demands a very high level of technical capability, raising the industry’s entry barriers and making it difficult for small and medium-sized enterprises to enter the high-end market.

The product development cycle is long and the cost of trial and error is high. Since the structure and formulation design of MOPP films must be highly matched with the final application, even slight mismatches can result in products failing to meet strength, adhesion, or processing requirements. Many complex MDO products (such as multilayer functional films) are not only difficult to design, but also prone to issues such as wrinkling, film breakage, and edge warping during mass production. This requires prolonged and repeated adjustment of equipment parameters, extending the time to market and increasing both R&D and raw material consumption costs. Adhesive tapes produced with MOPP films may also experience problems such as delamination and insufficient adhesion.

In addition to technical and development challenges, supply chain and transportation risks are also external factors that cannot be overlooked. The MOPP film market is concentrated in Europe and the United States, but its customers are distributed globally, and the products are sensitive to transportation conditions. During periods of logistical constraints (such as the COVID-19 pandemic), delays in long-distance transportation will directly affect the normal use by downstream customers, especially in industries such as home appliances and food packaging, which have extremely high requirements for delivery stability. Furthermore, manufacturers being far from the end markets results in long feedback cycles, which is unfavorable for rapid iteration and optimization of product performance, thus placing them at a disadvantage in fierce competition.

Industry Development Opportunities

In the coming years, MOPP film is expected to attract more attention under the trend of single-material soft packaging. With the rising global demand for sustainable materials, MOPP film is gradually becoming a candidate for environmentally friendly packaging alternatives due to its good recyclability and simple structure. Particularly in niche applications such as labels, tapes, and protective films for electronic components, its high strength and excellent processing performance make it highly competitive. Meanwhile, with the application of new technologies such as anti-static, low-shrinkage, and high-transparency modifications, the performance of MOPP film will continue to improve, meeting more high-end demands.

The global market is also showing a trend of regional focus gradually shifting towards the Asia-Pacific region, particularly China. Although European and American manufacturers currently still dominate a large portion of the high-end market, the expansion rate of China's production capacity is significant. If domestic companies can overcome key technical bottlenecks, such as eliminating shrinkage and adhesion, and improving thermal stability and antistatic performance, they are expected to make breakthroughs in the mid-to-high-end industrial film market, further promoting the localization of MOPP film.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)