111,000 Tons of TDI Production Capacity Strongly Resumes! Price Surge Expected to Boost Wanhua Chemical's Profits

Specialized VisionOn July 30th, Wanhua Chemical released the latest announcement stating that its Fujian Industrial Park's 800,000 tons/year MDI unit, 360,000 tons/year TDI unit, and 400,000 tons/year PVC unit have completed shutdown maintenance and resumed normal production.

Source: Wanhua Chemical

This news quickly attracted market attention.—Just one month ago, the global TDI supply plunged into chaos due to multiple accidents, causing prices to surge over 50% in a single month. Can Wanhua Chemical’s resumption of production become the “firefighter” in this supply chain crisis?

Continuous landslidesIn July, TDI prices experienced an epic surge.

As the world's largestAs a producer of MDI and TDI, Wanhua Chemical’s production capacity layout is truly “colossal”: by the end of 2024, its annual TDI production capacity will reach 1.11 million tons, accounting for nearly 30% of the global total. After the commissioning of the second 330,000 tons/year TDI project in Fujian in 2025, the total capacity will climb to 1.44 million tons per year. The TDI facility at the Fujian Industrial Park, which has just resumed production, is one of the key nodes in its global supply chain.

However, looking at the global situationTDI supply, the specialized plastic world has been continuously hit by "black swan" events since July.

On July 16, a fire at Covestro's Dormagen plant in Germany caused the shutdown of a 300,000 tons/year TDI unit. The interruption of chlorine supply triggered a chain reaction, leading to European TDI prices soaring from 1,900 euros/ton to 2,500 euros/ton (approximately 20,700 RMB).

On July 27, a chlorine leak occurred at Mitsui Chemicals' Omuta plant in Japan, causing an emergency shutdown of its 50,000 tons/year TDI facility (the only production site), bringing Japan's TDI production capacity to zero.

Covestro EuropeA 300,000-ton/year facility has been shut down due to a fire, and Mitsui Chemicals’ 50,000-ton/year facility in Japan has been forced to halt production due to a chlorine leak. Coupled with routine maintenance at plants in China, Hungary, and other locations, more than 1.23 million tons of global TDI capacity has been paralyzed, accounting for 40% of the world’s total capacity. Against this backdrop, the resumption of production at Wanhua Chemical is nothing short of a “shot in the arm” for the tense market.

TDI, or toluene diisocyanate, is a core raw material for polyurethane materials and is widely used in soft foam fields such as sofas, mattresses, and car seats. Its chemical properties are reactive, with two isocyanate groups (-NCO) that can combine with polyols like "Lego bricks" to form a three-dimensional network structure, giving products elasticity and durability. However, it was this crucial material that experienced a "roller coaster" market trend in July 2025.

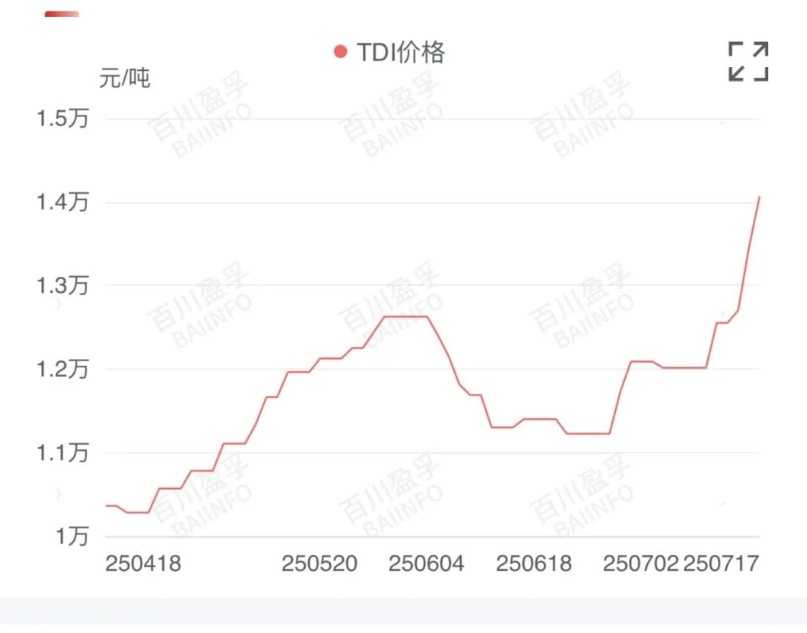

Source: Baichuan Yingfu

According to Baichuan Yingfu data,At the beginning of July, the average price of TDI in China was 11,733 yuan per ton. By July 27, it had surged past 18,000 yuan per ton, with a monthly increase of over 50%. A leading northern enterprise's payment price once soared above 20,000 yuan per ton, reaching an 18-month high. Traders closed their bids and were reluctant to sell, while end-user companies found it extremely difficult to procure goods. The market fell into a chaotic situation characterized by "available prices but no transactions."

Wanhua Chemical Resumes Production: Rush to Harvest or..."Lying down to win" and counting money?

Facing the worldWith 40% of TDI production capacity evaporated, Wanhua Chemical has undoubtedly become the biggest winner in this crisis. The resumption of production at its Fujian Industrial Park not only alleviated supply tensions but also directly captured the surge in overseas orders. In May 2025, China's TDI exports reached 51,600 tons, setting a new monthly record with a year-on-year increase of 98.45%; in June, exports were 48,000 tons, a year-on-year increase of 81.62%.

Wanhua Chemical's"Effortless dominance" is not accidental. By the end of 2024, its TDI production capacity of 1.11 million tons per year ranks first globally. After the commissioning of the second phase of the Fujian project with a capacity of 330,000 tons per year in 2025, its monopolistic position will be further consolidated. In contrast, the capacities of overseas giants Covestro, BASF, and Mitsui Chemicals have significantly contracted due to accidents, with Japan even facing a situation of 100% reliance on imports.

At the same time, it is actively building a moat through technological barriers.In 2024, the company’s R&D expenses exceeded 10.6 billion yuan, cumulatively overcoming 31 critical “bottleneck” technologies and developing 11 world-first innovations. For example, its independent MDI technology broke the monopoly held by BASF and Covestro; the fully localized ADI industry chain ended 70 years of foreign technological blockade; and the commissioning of the 400,000 tons/year POE project further broke Dow and Mitsui’s monopoly on photovoltaic materials. Each technological breakthrough signifies reduced costs and expanded market share.

Despite the currentTDI prices have gradually declined from their peak, but Wanhua Chemical's resumption of production can still benefit from the price premium. According to estimates, the production cost of TDI for domestic major manufacturers is approximately 9,500-10,005 RMB/ton. Based on the current average price of 17,000 RMB/ton, the net profit margin reaches as high as 50%-60%. Meanwhile, the company is mitigating cyclical risks through emerging businesses such as POE photovoltaic materials and lithium iron phosphate battery materials. The 200,000-ton POE project is operating at full capacity, and the second phase of 400,000 tons is scheduled to be put into production by the end of the year, with a gross profit margin exceeding 40%.

Epilogue: Cyclical"Antifragile" Evolution

Wanhua Chemical"Sitting back and reaping the benefits" is essentially the result of the vulnerability of the global supply chain being exposed and the resilience of China's leading chemical companies being highlighted.

In this "blitzkrieg" of TDI, the company leveraged its production capacity, technological barriers, and vertically integrated layout to turn a black swan event into a bargaining chip for pricing power. However, the cruelty of cyclical stocks lies in the fact that price increases will eventually trigger a supply-side backlash.

The true decisive move lies in whether one can..."Price elasticity" turns to "technical barriers"—POE replacing EVA, lithium iron phosphate breaking through energy density, citral breaking BASF's monopoly, these are the ultimate weapons for crossing cycles.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)