Wanhua Chemical Invests $27.3 Billion, 2026 Investment Map Revealed, $1.1 Billion Bet on Battery Materials

Recently, Wanhua Chemical released its annual investment plan, outlining a strategic blueprint of "consolidating its leading position in polyurethanes and launching a second growth curve in new energy" with a substantial investment of 27.3 billion yuan in projects and 2.22 billion yuan in external equity investments. As the world's largest producer of MDI and TDI, Wanhua Chemical, while consolidating its traditional strengths, is advancing into the fields of new energy materials and fine chemicals with unprecedented force.

Traditional main business: continuously expanding production, consolidating global dominant position

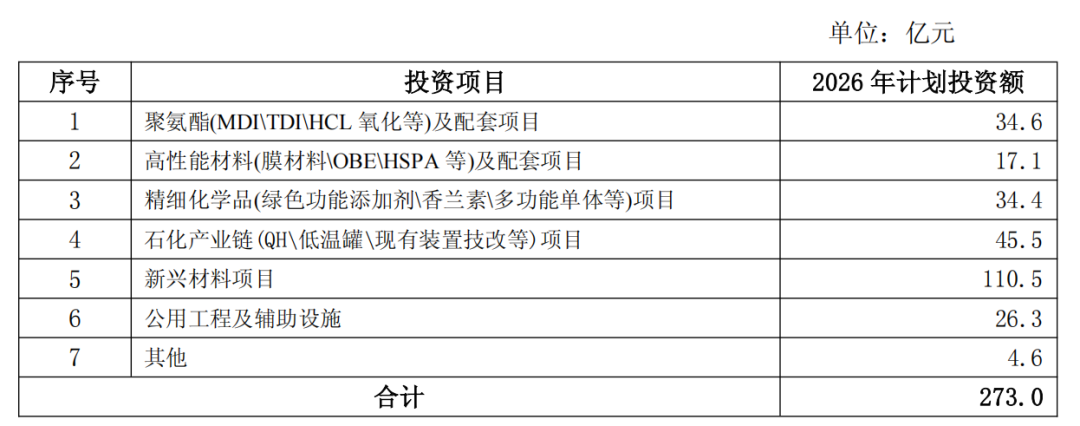

In the polyurethane sector, Wanhua Chemical continues to demonstrate a strong momentum of expansion. It plans to invest 3.46 billion yuan in polyurethane and related projects in 2026, with a focus on the MDI capacity expansion and integrated supporting projects. The MDI capacity expansion at the Fujian base has entered its later stages, with plans to increase the total capacity to 1.5 million tons per year. The additional 700,000 tons per year of capacity is expected to be completed in the second quarter of 2026. At that time, Wanhua Chemical's total MDI capacity will exceed 4.5 million tons per year, raising its global market share to approximately 41%.

BuyChemPlasAccording to institute monitoring, the total planned new and expanded global MDI production capacity amounts to 1.07 million tons, of which Wanhua Chemical alone contributes 700,000 tons, accounting for 65%. This figure clearly indicates that new global MDI capacity is highly concentrated in Wanhua Chemical.

In the TDI sector, Wanhua has also been highly active. The Fujian base has a planned total capacity of 720,000 tons/year. The second 360,000-tons/year TDI project was completed and commenced operations in July 2025. Wanhua Chemical’s total TDI capacity has thus reached 1.47 million tons/year, firmly securing the top global position.

By contrast, traditional competitors such as BASF and Covestro have no clearly defined timelines for new construction or capacity expansion projects in China or globally. Within China, only Hualu Hengsheng (300,000 tons/year) and Dongfang Shenghong (300,000 tons/year) have announced plans for new TDI projects; Hualu Hengsheng’s project has entered the environmental impact assessment stage and is scheduled for completion by the end of 2027, while Dongfang Shenghong’s project remains at the preliminary intention stage. This implies that domestic TDI capacity will become increasingly concentrated at Wanhua, leading to significant changes in the competitive landscape.

Petroleum Industry Chain: Improve Layout, Consolidate Integrated Advantages

The cost advantage of the polyurethane business cannot be separated from the stable supply of upstream naphtha raw materials. In 2026, Wanhua Chemical plans to invest 4.55 billion yuan in petrochemical industry chain projects, focusing on the construction of the QH project, low-temperature ethane tanks, and the optimization and technical transformation of existing facilities. Among these, the construction of low-temperature ethane tanks is particularly crucial. The technical transformation of the Yantai ethylene plant has already been completed, switching from the more costly propane to the cheaper ethane as a raw material. This not only enhances the profitability of the petrochemical sector itself but also provides a stable and low-cost raw material support for the polyurethane business, amplifying Wanhua Chemical's overall competitive advantage throughout the industry chain.

Emerging Materials: RMB 11.05 Billion Investment to Build a Second Growth Curve

The most striking aspect of this investment plan is Wanhua Chemical's historic ramp-up in emerging materials. In 2026, Wanhua Chemical plans to invest RMB 11.05 billion in emerging materials projects, focusing on the construction of battery material facilities for lithium iron phosphate and iron phosphate—a sum significantly exceeding the combined investments in polyurethanes (RMB 3.46 billion), petrochemicals (RMB 4.55 billion), and fine chemicals (RMB 3.44 billion).

This marks the commitment of Wanhua Chemical to promote the development of new energy materials business, and to build battery materials as the company's true "second growth curve."

Meanwhile, Wanhua Chemical also plans to invest RMB 3.44 billion in a fine chemicals project to accelerate the industrial-scale production of its self-developed green functional additives, vanillin, and nutraceutical products, further enriching its product portfolio.

In addition to fixed asset investment, Wanhua Chemical plans to make an external equity investment of 2.22 billion yuan in 2026, mainly focusing on the layout of battery materials, the development of new material businesses, and the implementation of an internationalization strategy. At the same time, it will leverage the advantages of an integrated industrial chain in the park to collaborate with upstream and downstream partners. This indicates that Wanhua Chemical is not only relying on internal growth but also integrating external resources through capital ties to accelerate the implementation of its strategy.

Overall, Wanhua Chemical’s 2026 investment plan embodies the strategic implementation of “securing steady growth through core businesses while pursuing future opportunities through emerging businesses.” The company continues to expand production capacity in its traditional leading sectors—such as MDI and TDI—further consolidating its global dominance through scale advantages, cost leadership, and technological superiority, and significantly benefiting from the industry’s new upcycle. Simultaneously, it is aggressively entering emerging fields—including new-energy materials and fine chemicals—with unprecedented commitment, thereby building diversified growth engines.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

Continental Plans to Begin Sale of ContiTech in Early 2026

-

Recycled PE/PP Morning Outlook: Market Expected to Remain Weak Within Range

-

Uae abruptly withdraws from opec! price hike wave sweeps across everything—from t-shirts and sofas to smartphones

-

From passive response to proactive service: IFLYTEK Redefines the Intelligent Cockpit Paradigm

-

Mianbi Intelligence and Wutong Technology Deepen Collaboration