Uae abruptly withdraws from opec! price hike wave sweeps across everything—from t-shirts and sofas to smartphones

Recently, a major announcement shook the global energy market. On April 28 local time, the UAE officially announced that it would withdraw from the Organization of the Petroleum Exporting Countries (OPEC) and the "OPEC+" mechanism starting from May 1, ending its nearly 60-year membership. Following the announcement, international oil prices fell sharply, with WTI and Brent crude oil prices dropping straight, each barrel falling by more than $2 at one point.

BBC News report screenshot

Behind this news, a transformation perhaps more intense than that of the oil market is brewing deep within the industrial chain. The global chemical supply shock triggered by the disruption in the Strait of Hormuz has surpassed the 2022 European energy crisis in both speed and intensity by twice, with the prices of basic chemicals surging over 60% in recent weeks. Raw material shortages, price hikes from major players, and a reshuffling of the supply chain—a wave of price increases is rippling down the industrial chain from crude oil to finished products, with the impact of the Middle East conflict affecting everything from the T-shirts in wardrobes to the sofas in living rooms, and even the phones in our hands.

I. UAE’s “Exit from the Group”: A Strategic Pivot Amid Geopolitical Rifts

The UAE's "exit from the group" was not sudden. The UAE government stated in its statement that the decision to leave OPEC and OPEC+ was made after a comprehensive assessment of the country's oil production policy and current and future capacity, based on national interests, aiming to more effectively meet the urgent demands of the international market. In short, "the meaning behind this statement is: the UAE wants to increase production."

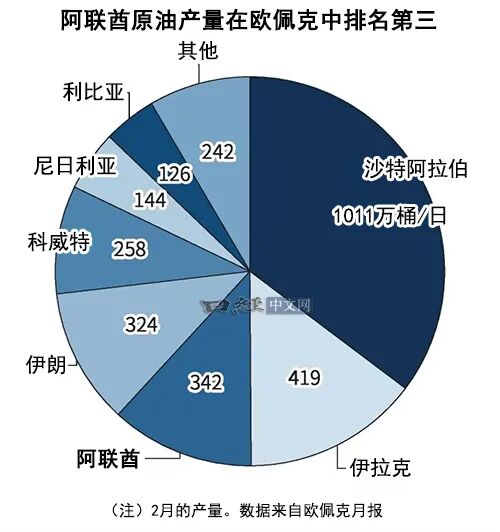

Before the Middle East conflict, the UAE's oil production accounted for 10% to 15% of the total production of OPEC countries. Leaving OPEC means the UAE can increase production without being restricted by OPEC quotas. Sergei Vakulenko, a former executive of Gazprom, analyzed that the UAE hopes to increase production by 30%, which is impossible under the OPEC and OPEC+ quota restrictions. Professor Bao Chengzhang from the Middle East Studies Institute at Shanghai International Studies University told Xinhua News Agency, "In the context of the 'blockage' of the Strait of Hormuz, the UAE hopes to get rid of OPEC's quota constraints, tap into its idle capacity, and flexibly adjust its production using the advantage of Fujairah Port, which is not affected by the 'blockage' of the Strait of Hormuz."

Saeed Al Tayer, UAE Minister of Energy and Infrastructure, stated in a media interview that the UAE’s announcement to withdraw is “well-timed” and will not significantly impact the oil market or prices, citing restricted passage through the Strait of Hormuz—which also affects the UAE—as a reason, and noting that this decision will help alleviate price pressures. He further remarked: “Global demand for energy will continue to grow, and the world needs more energy supply.”

But this time, the UAE's proactive "decoupling" from OPEC stems from long-standing rifts with Saudi Arabia. According to energy consultancy analysis cited by the BBC, the UAE's withdrawal "has been brewing for a while," as "Abu Dhabi has been pursuing ambitious capacity expansion but often feels constrained by the group's production quotas."

Reuters commented that against the backdrop of the Iran war having triggered a historic energy shock, the UAE's exit constitutes a significant blow to the oil-producing organization. UK business magazine, Business Matters, quoted the head of energy research at MST Financial, stating that this is "the beginning of the end for OPEC," warning that "Saudi Arabia will find it difficult to maintain the unity of the other member states and, in effect, will have to shoulder most of the burden for internal compliance and market management alone."

Screenshot of a report from the UK business magazine website Business Matters

Once the Strait of Hormuz becomes navigable again and exports resume, the UAE, which is not subject to quotas, will be capable of significantly increasing production, thereby structurally weakening OPEC's control over oil prices.

II. The Chemical Storm under Energy Supply Shocks

If the UAE's "withdrawal from the group" is a thunderclap in the geopolitical landscape, then the disruption in the Strait of Hormuz is triggering a chemical supply shock that is sweeping across the globe with far greater depth and breadth than anticipated.

The Strait of Hormuz—the world’s critical energy chokepoint, through which approximately 21 million barrels of crude oil pass daily—has been disrupted, triggering an unprecedented global chemical supply shock. According to Goldman Sachs’ latest report, prices of basic chemical products have surged over 60% in recent weeks, marking the fastest pace on record; “the speed and magnitude of the price increase are twice those observed during Europe’s 2022 energy crisis.”

What is more concerning is that this shock has hit the Asia-Pacific region particularly hard. The region relies on the Middle East for about 70% of the raw materials needed for chemical production, much higher than Europe's 20%; and the Asia-Pacific is precisely the core production area for global chemicals, accounting for about 65% of global production and 51% of manufacturing value-added. A disruption in raw materials from the Middle East means that a critical hub in the global supply chain has been directly hit hard.

About 20% of global chemical supply has been disrupted, with multiple petrochemical plants operating at minimum capacity (50% to 60%). As inventory continues to be depleted, some factories face the risk of shutdown. The impact has spread from low-value industries such as textiles and packaging to high-value sectors like construction and South Korea's semiconductor and memory chip production, which are now facing shortages of key chemical solvents. These solvents are typically by-products of basic chemical production and cannot be quickly restored independent of main production capacity.

III. Price Hikes by Industry Giants: A Ripple Effect Across the Entire Industrial Chain

Amid energy supply shocks, chemical giants at the upstream of the industrial chain have begun to act collectively, issuing price increase notices like snowflakes, becoming the most direct barometer of this round of shocks.

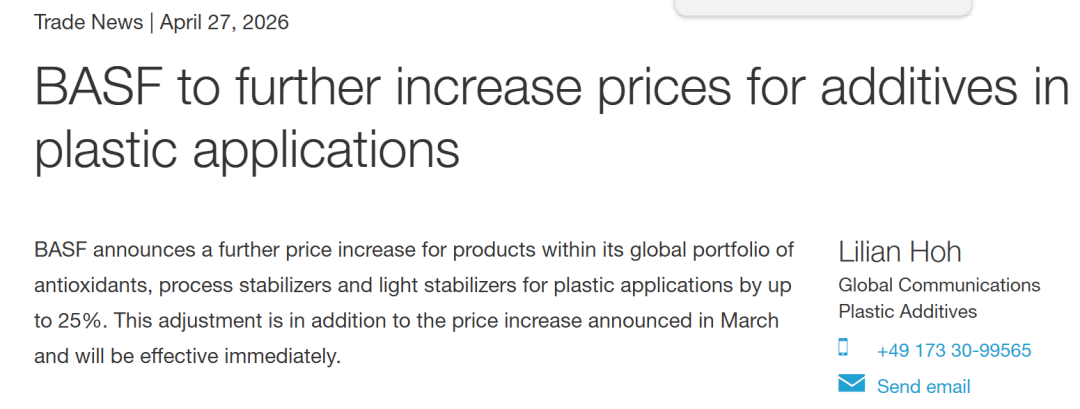

As an industry benchmark, BASF has issued price increase announcements five times consecutively since the outbreak of the Middle East conflict, covering multiple product categories including butyl acrylate, MDI, TDI, amine-based products, antioxidants, processing aids, and light stabilizers, with price adjustments affecting major global markets such as Europe, North America, and Asia-Pacific. On April 27, BASF announced another global price increase of up to 25% for antioxidants, processing stabilizers, and light stabilizers used in plastic applications, explicitly attributing the price adjustment to comprehensive cost increases in raw materials, energy, and logistics resulting from the Middle East military conflict.

Domestic industry leader Wanhua Chemical has also frequently raised prices across multiple product lines. As of April, the price of polymeric MDI increased from approximately RMB 14,500 per ton to approximately RMB 15,500 per ton, and the average price of TDI rose from approximately RMB 13,200 per ton to approximately RMB 15,800 per ton. Wanhua Chemical’s subsidiary, BorsodChem in Hungary, effective April 1, increased prices for all MDI products in the Europe, Middle East, and Africa regions by EUR 500 per ton (approximately RMB 3,982 per ton).

The core raw materials of the polyurethane industry chain, MDI and TDI, have experienced a rare "epic" price hike - on March 31, Sadara, the largest MDI/TDI producer in the Middle East and a joint venture between Saudi Aramco and Dow Chemical, announced a complete shutdown, with no set date for resumption of production, directly leading to a significant shortage in global supply.

Goldman Sachs issued a clear warning in its report: "Our recent conversations with investors indicate that the warning signals from the petrochemical industry have been noticed but not yet fully appreciated, largely because the impact has not yet been felt tangibly." From a cost perspective, the increase in petrochemical derivatives is expected to have an average impact of about 11% on the cost of goods sold for European and American companies, with the furniture industry being the most affected at 20%, followed by the medical aesthetics industry at 18%, and the apparel industry at 15%.

IV. Supply recovery is a long way off: Normalization is not expected until 2027 at the earliest

Compared to the current price surge, a more pressing issue is: how long will it take for the supply chain to recover?

However, the above calculation is based solely on the extremely optimistic assumption of "immediate recovery."

Dow Chemical stated that it will take approximately 250 to 275 days for the petrochemical supply chain to return to normal. It should also be noted that chemical products and raw materials face a “dual queuing” dilemma in the clearance of shipping congestion in the Strait of Hormuz, as they are prioritized after crude oil, fuels, and fertilizers.

Comprehensive analysis indicates that the physical supply relief for chemical products in Europe and Asia is not expected before Q3 2026, which will further drive up chemical product prices and exacerbate supply chain disruptions. The market is currently severely underestimating the depth and breadth of this shock, and investors must remain vigilant.

V. The War Spreads to the Wardrobe: The Price Surge in the Textile and Apparel Industry

At the end of the supply chain, consumers are gradually feeling the impact. A T-shirt costing just a few dozen yuan is being swept up by the turmoil in this long-distance supply chain.

Industry insiders told the media that the Middle East is the core supplier of global energy and petrochemical raw materials, with Iran being a significant exporter of crude oil and ethylene glycol. The geopolitical conflicts in the Middle East have directly led to disruptions in shipping through the Strait of Hormuz, causing the prices of PTA and MEG to rise by nearly 30% recently, which in turn has pushed up the domestic polyester prices.

Li Sijin, a senior analyst at CITIC Construction Futures, stated that the conflict in the Middle East has caused a systemic shock to the polyester industry chain, from raw materials to the end products, "A wave of price increases is sweeping through the global textile and apparel industry. Whether companies deplete their raw material inventories or increase imports, they cannot make up for the supply gap; the passing on of price increases to the downstream is just a matter of time and magnitude."

The shock has already been felt in major clothing production countries. Surat, India—global textile hub—Radheshyam Textile Company has 200 industrial looms used for weaving polyester fabric, half of which have been idle since the conflict broke out in late February. "Before the war, our daily output was 10,000 meters, but now it has dropped to 3,500 to 4,000 meters per day," said the chairman of the Surat Textile Merchants' Association. Rising costs have led to textile dyeing and printing factories in Surat to shut down two days a week, up from one day previously. "If this situation continues, raw material shortages will begin, and factories will have to shut down."

")

The image shows workers packaging printed polyester fabric inside the Bindal Silk Mill in Surat, India. (Reuters)

In Bangladesh, although local factories mainly produce cotton garments, they are also facing the dual pressures of rising prices of polyester sewing thread and increasing logistics costs. Coats Bangladesh, a thread manufacturer, has announced a price increase of 15.5% starting from April 15, citing "a sharp rise in the cost of oil-derived raw materials" and higher transportation costs.

Retailers will ultimately be unable to avoid the impact. Mainstream fast fashion brands such as Zara, H&M, and Uniqlo use polyester fiber in more than 90% of their clothing fabrics, and the production cost increase for some styles has already exceeded 20%. Industry sources said H&M expects its suppliers in Bangladesh to raise prices in the coming weeks.

Although retailers such as Zara and H&M have shifted primarily to recycled polyester fibers made from discarded plastic bottles to alleviate cost pressures, globally recycled polyester accounts for only 12% of total polyester production, offering extremely limited relief.

Zhou Lihang, a futures analyst from Zhejiang Futures, stated: "In the short term, as long as the conflict continues, the trend of terminal price increases will not stop. This summer's clothing orders will see a comprehensive price hike, with retail prices of finished garments expected to rise by 5% to 15%." High cost pressures will force the industry to shift toward a new phase characterized by "high prices, slow turnover, and compressed profits."

Six: Risk of Demand Contraction: High Price Does Not Necessarily Mean High Profit

However, price transmission is not a one-way street. Bluna Angel, chief analyst at Wood Mackenzie's Fiber Division, raised a warning that cannot be ignored: "If this situation continues for another month, forget it — our clothing production will decline, and so-called 'demand destruction' will occur, because retailers will have to raise prices, and consumers will cut back on spending."

This judgment has been corroborated at the macro level. According to the International Energy Agency, global oil demand is projected to decline in 2026—the first drop since 2020—as “demand destruction,” driven by consumption curbs and the transition to alternative energy sources, accelerates.

For end-user products, the transmission to consumers has a lag period of 6 to 12 months, with the peak price pressure expected to occur in the third or fourth quarter of 2026. The automotive industry has the longest lag, ranging from 9 to 18 months, while the apparel industry has a shorter lag, approximately 3 to 6 months. However, the average inventory coverage period across industries is only about 3.7 months, indicating a thinner buffer than expected.

This means that enterprises will face the dual squeeze of rising costs and declining demand in the second half of the year. Finding a balance between "selling at a high price" and "selling effectively" will be a common challenge for all downstream industries relying on petrochemical raw materials.

From the UAE's withdrawal from OPEC to the obstruction of the Strait of Hormuz, from chemical giants' consecutive price hikes to the transmission chain of a single clothing price increase — a crisis in energy and chemicals ignited by geopolitical tensions is rapidly and extensively rewriting the cost structure of global manufacturing. With about 20% of global chemical supply already disrupted, the light of supply chain recovery is not expected to appear until at least the third quarter of 2026, and before that, the price shock will continue to spread downstream.

Industries such as furniture, medical aesthetics, and apparel were hit first and hardest, becoming the most severely affected sectors in this crisis. Meanwhile, after export recovery, the UAE’s capacity to increase oil production without quota restrictions could pose a structural downside risk to oil prices over a longer time horizon.

As Goldman Sachs explicitly warned in the concluding part of its report: “Each day the Strait of Hormuz remains blocked, the supply shock to the global chemical industry and manufacturing sector intensifies. Investors must reassess their exposure to consumer goods, manufacturing, chemicals, and related supply chains, and fully prepare for potential cost pressures and inflation risks in the second half of 2026.”

In 2026, above a piece of clothing likely to be more expensive than usual and a refrigerator likely to see price hikes, there looms not only the smoke of conflict from the Middle East but also the far-reaching shadow of a disrupted supply chain.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Continental Plans to Begin Sale of ContiTech in Early 2026

-

$4 Billion! Medtronic Makes Another Acquisition

-

Profit and Revenue Growth Struggle to Conceal Debt Repayment Pressure; Success of Kingfa Sci & Tech's High-End Strategy Yet to Be Seen

-

BASF Delivers First Batch of Innovative Cathode Materials for Semi-Solid-State Batteries to Weilan New Energy

-

Why did a century-old european dental instrument giant relocate its manufacturing hub to china?