Titan Chemical Releases First Report After Name Change: Revenue Breaks 7.7 Billion for the First Time, Record High, Net Profit at a Low Point Under Pressure

Recently, Titanium Energy Chemicals submitted its first annual report card after the name change from "CNNC Titanium White." Since the stock abbreviation was officially changed from "CNNC Titanium White" to "Titanium Energy Chemicals" on October 20, 2025, the company has shown a significant increase in revenue but faced notable pressure on profitability in this deeper strategic transformation.

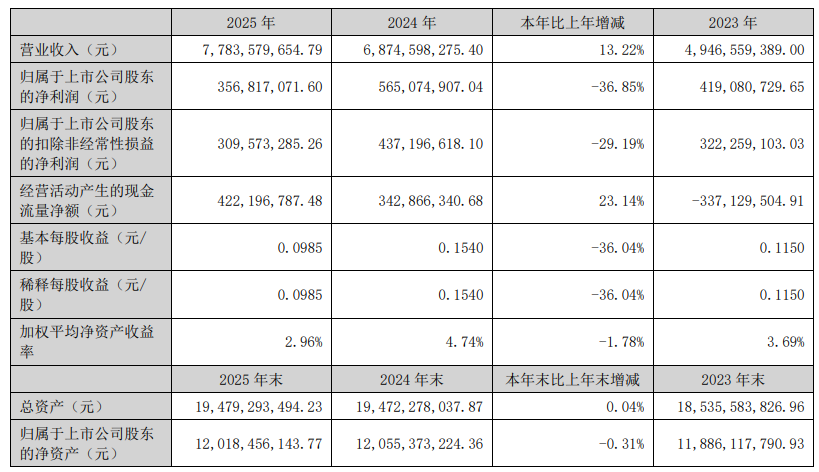

Annual report data shows that the company achieved operating revenue of 7.784 billion yuan in 2025, an increase of 13.22% compared to the previous year, breaking through the 7.7 billion yuan threshold for the first time and setting a new historical high. However, the net profit attributable to shareholders of the listed company was only 357 million yuan, down 36.85% from 565 million yuan in the same period last year.

Renaming is not just a change of name, but also a reaffirmation of strategic direction. Centered around the collaborative development of "titanium chemicals + phosphorus chemicals + new energy materials," the company is firmly advancing a "sulfur-phosphorus-iron-titanium-lithium" green coupled circular industrial system. It aims to resist cyclical fluctuations through a deep layout of the entire industry chain, striving to become one of the world's largest manufacturers of titanium dioxide by the sulfate process and yellow phosphorus. However, both the annual report and the latest first-quarter report indicate that in the early stages of this strategic transformation, the company is experiencing the pain of a downward industry cycle.

Titanium dioxide production and sales hit new highs, but costs squeeze gross profit margin to 9.19%

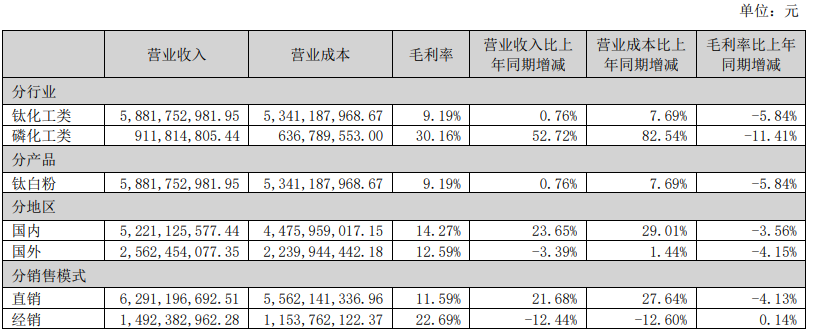

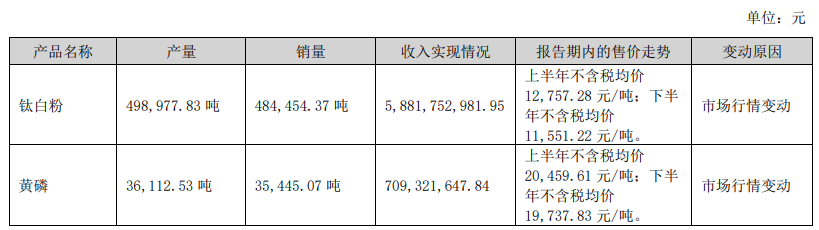

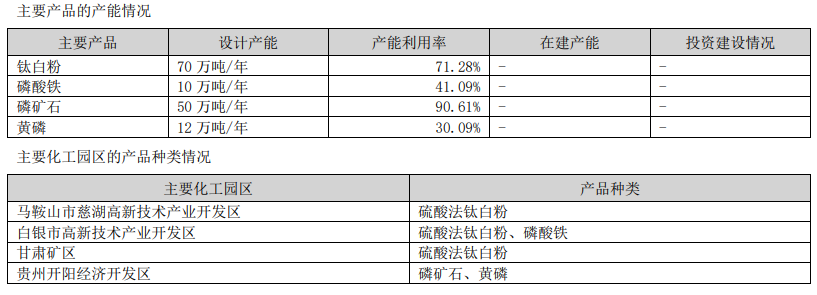

In 2025, Titan Energy Chemical’s titanium dioxide business continued to serve as a stabilizing pillar. The company produced 499,000 tons of titanium dioxide, representing a 9.70% year-on-year increase; and sold 484,500 tons, up 13.08% year-on-year—both production and sales volumes of titanium dioxide reached new historical highs. Revenue from the three core products—titanium dioxide, phosphate rock, and yellow phosphorus—accounted for over 87% of the company’s total revenue in 2025. The company’s annual titanium dioxide production capacity has approached 700,000 tons, ranking second domestically. Titan Energy Chemical demonstrated robust supply capability and strong market momentum.

However, the other side of income growth is a significant narrowing of gross profit margin. Annual report data shows that the gross profit margin for titanium dioxide in 2025 was only 9.19%, a sharp decline of 5.84 percentage points compared to the same period last year. The core reason for this "increased revenue but not increased profit" situation lies in the persistently high costs of upstream raw materials. Titanium concentrate and sulfuric acid account for more than 60% of the production cost of titanium dioxide. In 2025, domestic sulfuric acid prices surged significantly during the year, and titanium concentrate has remained at a high level for a long time, greatly eroding the profit margin. At the same time, the complex and changing macroeconomic environment both domestically and internationally has led to weak growth in end-user demand for titanium dioxide. The entire domestic titanium dioxide market remained in a weak operating trend throughout the year.

Accelerated release of yellow phosphorus production capacity, high phosphorite mining prosperity supports stable growth.

In the second growth curve of the company, the phosphate chemical sector has shown significant structural differentiation.

At the phosphate rock end, supported by dual demand drivers—new energy applications such as lithium iron phosphate (LFP) batteries and traditional agricultural use—the phosphate rock price remains at a high level in 2025. The Company’s wholly-owned subsidiary, Shuangyang Phosphate Mine, currently holds phosphate rock reserves of approximately 13.6 million tons, with an original ore production capacity of 500,000 tons per year. The ore’s average grade reaches 30%, classifying it as a relatively scarce high-grade phosphate resource domestically. In 2025, the Company produced 453,000 tons of phosphate concentrate, ensuring a stable supply of core raw materials for its yellow phosphorus production. The integrated “mine-chemical” business model confers a cost advantage, effectively hedging against industry volatility risks.

Huanglin Duan: In 2025, yellow phosphorus production capacity will enter a stable ramp-up phase. Annual yellow phosphorus production reached 36,100 tons, an increase of 86.84% year-on-year; yellow phosphorus sales amounted to 35,400 tons, up 84.35% year-on-year. The yellow phosphorus business has transitioned from its initial stage to a rapid capacity-ramping phase and is emerging as a new, stable source of revenue for the company.

The new energy materials segment exhibits strategic investment characteristics typical of an expansion phase. In 2025, the company produced 41,100 metric tons of lithium iron phosphate and sold 39,100 metric tons, with downstream customers already receiving volume shipments. However, given that the current domestic lithium iron phosphate industry operates at a capacity utilization rate of only around 50%, and the sector as a whole remains in a phase of capacity rationalization, profitability pressure in this segment is within expectations.

Hand-in-hand with Nippon Paint to lock in high-end demand, and partnering with Guizhou Phosphate Group to build an industrial moat.

During the reporting period, the company entered into two significant strategic partnerships worthy of close attention. First, the company signed a three-year Strategic Cooperation Agreement with Nippon Paint Holdings, establishing a strategic titanium dioxide supply relationship from 2025 to 2027. The company is expected to become one of Nippon Paint Holdings' largest suppliers of titanium dioxide products. This agreement not only secures a portion of the company's market share for the next three years but also signifies that the company’s product quality and service capabilities have received deep recognition from a global leading coatings giant, providing crucial support for overcoming current demand constraints and enhancing penetration in high-end application segments.

Secondly, the Company has jointly established Guizhou Zhonghe Phosphochemical Co., Ltd. with Guizhou Phosphate Chemical (Group) Co., Ltd., focusing on the “Sulfur–Phosphorus–Iron–Titanium–Lithium” green circular industry project. As the top player in China’s phosphate chemical industry, Guizhou Phosphate Chemical Group provides industrial empowerment to the Company, further strengthening its strategic layout in phosphate rock resources and the yellow phosphorus industry chain.

Green cycle builds cost moat, pressure remains in Q1 2026

In 2025, the company deeply focused on its four core business segments—resources, chemical engineering, new materials, and new energy—successfully developed phosphate iron and commenced mass production and supply. Environmental protection investments totaled RMB 373 million, with pollutant monitoring compliance rate and hazardous waste compliant disposal rate both reaching 100%. To date, the company holds 272 valid patents, including 50 invention patents, and its R&D investment accounted for 1.89% of revenue.

However, the company continues to face significant operational pressure entering 2026. In the first quarter of 2026, the company achieved operating revenue of RMB 2.181 billion, representing a year-on-year increase of 6.99%; however, net profit attributable to shareholders of the listed company amounted to only RMB 104 million, a year-on-year decline of 22.53%. According to the company’s financial report, the decline in net profit was primarily attributable to increased interest expenses resulting from higher bank borrowings, as well as foreign exchange losses arising from fluctuations in foreign currency exchange rates.

Faced with this situation, Titan Chemical has been seeking breakthroughs in two directions. Upstream in the industrial chain, it is actively advancing a new project in collaboration with Phosphorus Group, establishing a sustainable cost barrier through an integrated mining-chemical model. Downstream in the market, it has secured demand from leading customers through its strategic partnership with Nippon Paint, while continuously expanding distribution channels for downstream new-energy materials such as lithium iron phosphate. As each segment of the “sulfur–phosphorus–iron–titanium–lithium” green circular industrial chain is connected and production capacity comes online, a strategic roadmap for navigating cyclical fluctuations has already taken shape.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

Continental Plans to Begin Sale of ContiTech in Early 2026

-

Recycled PE/PP Morning Outlook: Market Expected to Remain Weak Within Range

-

Uae abruptly withdraws from opec! price hike wave sweeps across everything—from t-shirts and sofas to smartphones

-

From passive response to proactive service: IFLYTEK Redefines the Intelligent Cockpit Paradigm

-

Mianbi Intelligence and Wutong Technology Deepen Collaboration