The Tug of War Between Cost Collapse and Tight Supply! Caprolactam Market Returns to a Downward Trend

Since June 2026, the caprolactam market has gone through a roller-coaster cycle of “rebound then pullback.” Last week, the market tentatively rebounded on the dual support of rising costs and reduced supply; however, this week, as signs of easing emerged in the Middle East geopolitical conflict, upstream prices for crude oil, pure benzene, and sulfur all turned downward, causing caprolactam’s cost support to erode rapidly and prices to retreat accordingly.

Pure benzene: Two price cuts in one week, with a cumulative decrease of RMB 600/ton.

As the primary raw material for caprolactam, pure benzene accounts for more than 60% of its production cost, so fluctuations in benzene prices have a direct impact on caprolactam. Following reports that the United States and Iran had remotely signed a memorandum of understanding and that the Strait of Hormuz would gradually reopen, geopolitical risks have eased significantly, and crude oil prices have continued to decline. As of the week ending June 18, Brent crude oil futures had fallen below the $80 per barrel mark.

Due to this drag, the price of benzene quickly fell. Sinopec's East China benzene listing price was 7,700 yuan/ton on June 11, and was lowered by 300 yuan to 7,400 yuan/ton on June 17, followed by another reduction of 300 yuan to 7,100 yuan/ton on June 18—an accumulated decrease of 600 yuan/ton within a week, representing a drop of 7.79%. The spot price of benzene in the East China market also declined, with the negotiation range falling to 7,050-7,130 yuan/ton on June 17.

Sulfur: From a Peak of Tens of Thousands to a Rapid Decline

The trend in sulfur prices has been even more dramatic. Since the beginning of 2026, sulfur prices have continued to climb, surpassing the 10,000-yuan mark by mid-June. On June 11, the highest transaction price of sulfur briefly reached 11,985 yuan/ton. However, after the U.S. and Iran reached a memorandum of understanding, sulfur prices retreated sharply. By June 15, the transaction price had fallen to 9,500 yuan/ton, and on June 18, SunSirs’ sulfur benchmark price stood at 9,334.33 yuan/ton. In Shandong, refinery ex-factory sulfur prices were further lowered on June 17 to 9,507-10,000 yuan/ton, with an average of 9,753.5 yuan/ton, down 600 yuan/ton on the day. Although the tight sulfur supply situation has changed only marginally, expectations of a gradual recovery in overseas supply have shifted market sentiment.

Caprolactam: Costs Collapse, Prices Follow Suit and Decline

With upstream raw material prices both plunging sharply, the cost side of caprolactam quickly turned bearish. On June 16, the spot price of caprolactam in East China was still RMB 11,500/mt, acceptance delivered. On June 17, as Sinopec lowered its pure benzene price again, the caprolactam spot price fell by RMB 300 in a single day to RMB 11,200/mt, a decline of 2.61%. Sinopec’s weekly settlement price for caprolactam stood at RMB 11,900/mt.

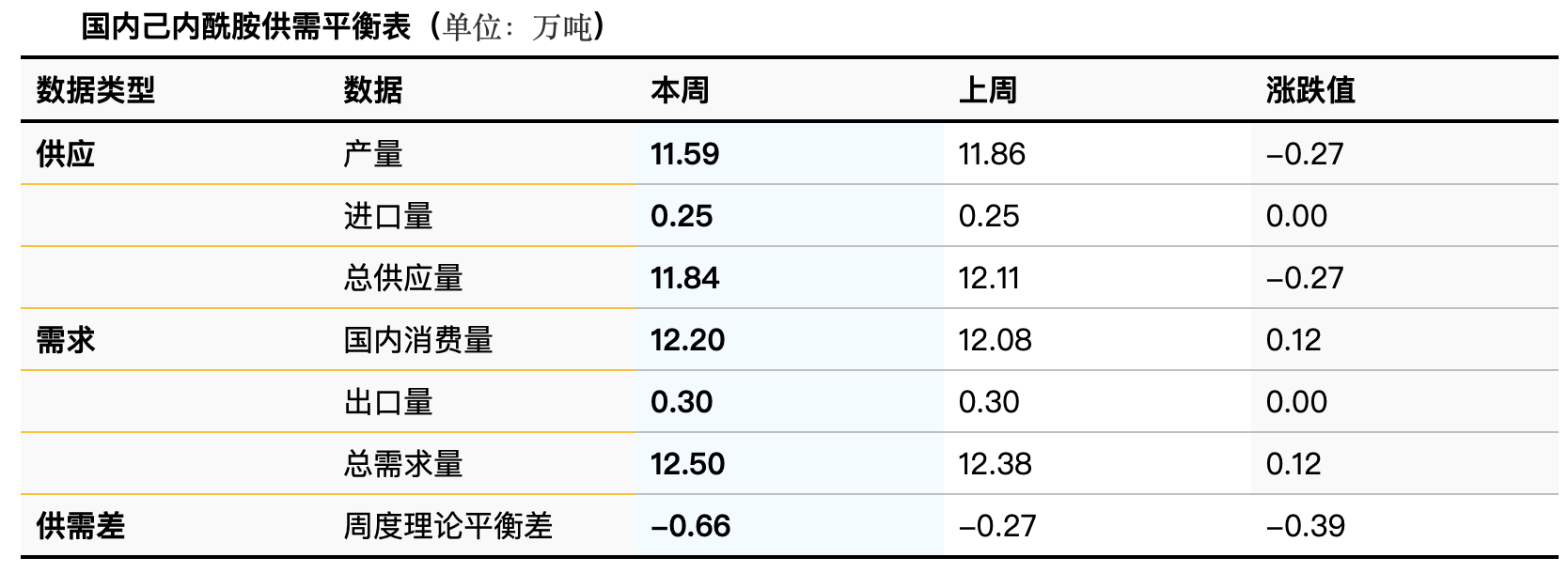

It is worth noting that despite the sharp decline on the cost side, the supply of caprolactam remained relatively tight, which to some extent cushioned the price decline. This week (June 12–18), domestic caprolactam output stood at 115,900 tonnes, down 2,700 tonnes from the previous period; the capacity utilization rate was 67.90%, down 1.58 percentage points from the previous period. The caprolactam capacity base was 8.13 million tonnes per year. From the perspective of supply-demand balance, total supply this week was 118,400 tonnes, while total demand was 125,000 tonnes, resulting in a weekly theoretical balance of -6,600 tonnes, with the supply-demand gap widening further from -2,700 tonnes last week. Enterprise inventories also fell to 27,000 tonnes, down 4,500 tonnes from the previous period.

Supported by relatively strong supply, caprolactam's decline has been slower than that of benzene, the benzene-caprolactam spread has widened, and losses in the caprolactam segment have narrowed. According to data from Longzhong Information, this week caprolactam plant gross margins were -461 yuan/ton, up 579 yuan/ton from the previous period. However, in the first week of June caprolactam production margins had fallen to -2,720 yuan/ton, and the industry's deep losses have not yet been fundamentally reversed.

Downstream PA6: Bearish cost factors pass through, with chips following the decline.

Downstream PA6 chip sales also slowed and prices declined under the bearish impact of weakening costs. As of June 18, prices for standard-grade PA6 conventional spinning chips in East China were at RMB 11,300-11,600/tonne, cash, short-distance delivery; spot prices for premium-grade PA6 high-speed spinning chips in East China were around RMB 12,000/tonne, acceptance bill, delivered. The weekly average profit for PA6 conventional spinning chips was RMB -560/tonne, with the industry still in a loss-making state. Downstream players are bearish on the outlook, becoming more cautious in raw material procurement, while PA6 polymerization enterprises are only maintaining purchases to meet rigid demand.

Outlook for the market: The weak and volatile game-like pattern is expected to continue.

Looking ahead, the cost side will remain the key variable driving the caprolactam market. The U.S. and Iran are about to enter the second round of negotiations, while the geopolitical risk premium continues to fade. In the short term, crude oil, pure benzene, and sulfur prices may continue to fluctuate with a weaker bias. As for sulfur, although current prices have fallen sharply from their highs, the level of 9,334 yuan/ton remains historically elevated, and the pace of overseas supply recovery will still need to be closely monitored.

On the supply side, caprolactam producers are mostly maintaining operating rates slightly below 70%. Luxi Chemical’s 650,000 t/y unit is undergoing a phase III turnaround, and Nanjing Oriental’s 400,000 t/y unit has been shut down. Overall supply remains tight, and this pattern is unlikely to fundamentally change in the short term, which may limit the pace of caprolactam price declines. However, sentiment on the demand side is bearish. Downstream purchasing remains cautious, PA6 chip sales have weakened, and polymer producers are becoming increasingly conservative in their expectations for feedstock procurement.

Overall, the decline in feedstock prices has weakened the bottom support of the caprolactam market and further intensified downstream pessimism. Going forward, the caprolactam market may return to a weak tug-of-war characterized by a downward shift in costs and relatively weak demand. Continued attention should be paid to the magnitude of feedstock price fluctuations and the dynamic adjustments on both the supply and demand sides.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

A Look at the Material Suppliers Behind SpaceX

-

Next-generation motors of new energy vehicles: Single-Round Thousand Horsepower, Replacing Brakes, How Powerful Are They?

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

United States Imposes 208.49% Tariff On Chinese Glass Fiber Products

-

Celanese Joins Forces With Aisan Industry to Reshape the Low-Carbon POM Competitive Landscape, Changing the Automotive Supply Chain