Risen, but not fully risen? pa6 market is playing a dangerous divergence

One of the most eye-catching products in the chemical market recently is undoubtedly PA6.

Driven by the continued sharp rise in upstream sulfur prices, the cost of caprolactam has remained high, and the PA6 market has also experienced fluctuations under cost pressures. At the beginning of June, the PA6 chip market saw a round of price increases, with polymerization plants reluctant to sell at low prices. A small amount of replenishment from downstream buyers temporarily boosted trading activity in the market.

On the surface, this appears to be a natural cost-driven upswing. But upon closer examination, a question worth noting is beginning to emerge—The logic of price increases and the performance of terminal demand are beginning to diverge.

1. The Driving Forces Behind Prices

This round of price increases originated from sulfur.

Since 2026, domestic sulfur prices have followed an almost vertical upward curve. According to data from Shengyi Society, the price of sulfur stood at 3,661 yuan/ton at the beginning of the year and had climbed to 8,033.33 yuan/ton by June 8, marking an increase of 119.43% year to date. Actual transaction prices, however, have been even more astonishing — as of June 12, the mainstream transaction price of solid sulfur at Zhenjiang Port and Dafeng Port had risen to as high as 11,600 yuan/ton, with a cumulative increase of more than 210% this year, nearly ten times the low point in the second half of 2024, setting the strongest rally since 2008.

Image source: Securities Times

This sharp surge was no coincidence. In the global sulfur trade system, the Middle East accounts for about 45% of sulfur trade volume, and since transit through the Strait of Hormuz became restricted in late February, the arrival cycle for overseas cargoes has lengthened significantly. Meanwhile, Russia extended its sulfur export ban until the end of June, cutting off most European re-export supplies. Customs data show that China’s sulfur imports in April 2026 were only 295,500 tons, down sharply by 72.39% year on year and hitting a new monthly low in recent years, while port inventories were nearly halved compared with the same period last year.

High sulfur prices have directly driven up the production cost of caprolactam. According to data from Longzhong Information, Sinopec’s listed price for pure benzene in East China remained high at 7,700 yuan/ton after being lowered at the end of May. In the first week of June, caprolactam production gross profit had fallen to -2,720 yuan, while unit gross profit stood at -340 yuan.

The cost pressure from the raw material side has been clearly transmitted to the PA6 chip market. In mid-June, prices for conventional spinning-grade standard PA6 chips were in the range of RMB 11,500–11,900/ton, while quotations for some premium high-end chips reached RMB 12,100/ton, up slightly from the previous week.

II. Prices Have Risen, but the Market Is Cooling

However, on the other side of rising prices, the entire industry chain is experiencing an unprecedented "alternation of cold and heat."

In early June, the PA6 chip market was not moving smoothly. According to data monitored by SunSirs, the PA6 benchmark price fell from 12,300 yuan/ton at the beginning of June to 11,700 yuan/ton on June 7, a drop of about 4.88%. On the cost side, caprolactam prices were also weakening, with the benchmark price declining from 12,887.5 yuan/ton at the beginning of May to 11,100 yuan/ton, marking a cumulative drop of more than 6% in May. The price rebound in early June was driven more by a phased upward move caused by rising sulfur costs, rather than by a sustained rally supported by demand recovery.

More noteworthy is the change in operating rates. Data from Longzhong Information shows that in early June 2026, domestic PA6 polymerization capacity utilization continued to decline. From late May to early June, PA6 capacity utilization stood at 63.19%; in the week of June 5–11, it fell further to 62.56%, while output also decreased from 117,500 tonnes in the previous week to 116,300 tonnes. Compared with the peak capacity utilization rate of 72.50% in late March, the decline is quite significant.

The polymerization plants have proactively cut operating rates, behind which lies weak demand. According to data from Zhuochuang Information, as of early June, the average inventory level of PA6 sample enterprises had reached 11.7 days, with some companies holding more than 200,000 tons in inventory. With high inventory levels and insufficient downstream purchasing willingness, polymerization plants have been forced to trade price for volume, further slowing their procurement pace for caprolactam.

At the same time, industry profits for conventional spinning-grade PA6 chips have fallen into deep losses. Calculations by Longzhong Information show that as of June 11, based on the East China liquid spot price of caprolactam at RMB 11,500/tonne and the ex-works price of PA6 chips at RMB 11,500–11,900/tonne, the weekly average profit for conventional spinning-grade PA6 chips was RMB -590/tonne. Selling one tonne means losing money on one tonne, which is becoming the reality for many polymerization plants.

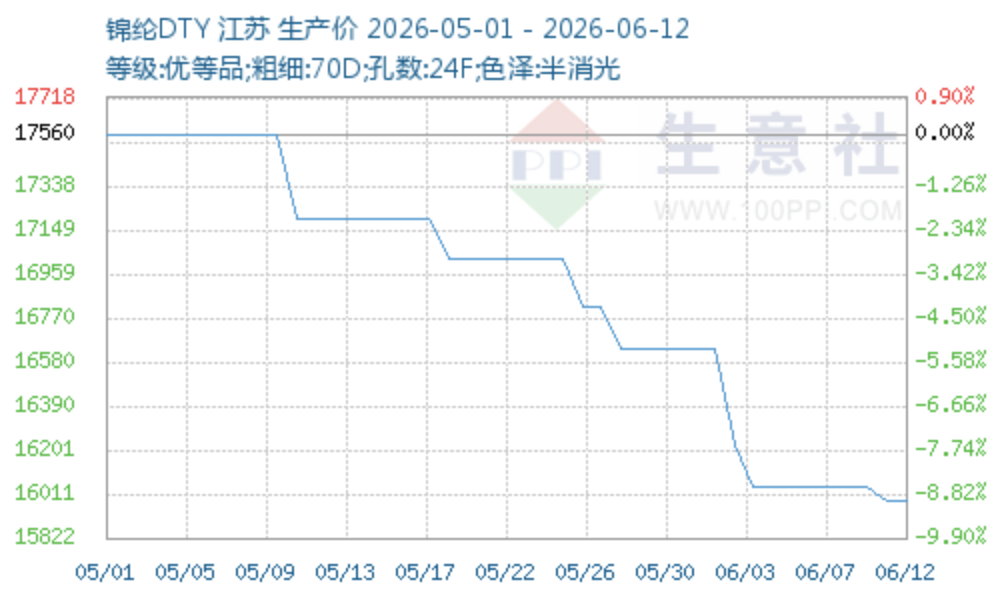

The nylon filament market, further downstream in the industrial chain, is also feeling a clear chill. In early June, the price of nylon POY fell from RMB 14,500/ton to RMB 13,800/ton, a decline of 9.51% over the period; nylon DTY dropped from RMB 16,640/ton to RMB 15,980/ton, a cumulative decrease of 3.97%. Throughout early June, the nylon filament market remained weak across the board and trended downward. Downstream buyers only maintained rigid-demand replenishment, with very little willingness to make large-volume purchases or build inventories in advance, and the volume of circulating market orders continued to shrink.

Longzhong Information pointed out in its market analysis in mid-June that the downstream textile market is in a traditional off-season, with weak order follow-up and continued pressure on industry operations. Terminal consumption has not shown significant improvement, and downstream factories have no motivation to expand production or increase procurement, leading to a continued tightening of purchasing from upstream.

III. Cost pass-through is beginning to show a disconnect.

In any upward market trend, sustained growth requires the support of downstream demand.

When demand grows in tandem, rising costs can be smoothly passed downstream, with each link in the chain jointly absorbing the higher prices. At present, the sharp surge in sulfur prices has indeed been passed on to caprolactam and PA6, but further transmission downstream has run into resistance. Caprolactam producers have been forced to cut output due to losses, and industry operating rates have already fallen from their peaks. Meanwhile, downstream nylon spinning and modified plastics companies are also facing weak demand, leaving them with little incentive to increase purchases.

The deeper issue lies on the supply side. A research report by Changjiang Securities pointed out that China’s total PA6 production capacity has exceeded 8.5 million tonnes, with output at around 7 million tonnes. The industry’s operating rate has been significantly dragged down, with some capacity sitting idle or awaiting commissioning. Amid the market downturn, companies are facing the dual pressures of cutting production to support prices and shifting their products toward differentiation and higher-end offerings.

Industry insiders describe the current market situation as being squeezed between a “high-cost plateau” and a “low-demand trough” — upstream raw material prices remain elevated, downstream orders are sluggish, and losses across the entire industry chain are intensifying. Longzhong Information analyst Zhuang Xiaohua stated bluntly that June to July is the traditional off-season for the textile industry, and with the recovery in automobile consumption proceeding slowly, end-user demand for PA6 is unlikely to see any substantial rebound.

IV. Market Outlook: Cautious in June, Awaiting Observation in July

For the remainder of June, the core contradiction in the PA6 market—the tug-of-war between cost support and weak demand—will persist. The high-level operation of sulfur has exerted strong upward cost pressure across the entire aromatics and downstream industrial chain, making it unlikely for pure benzene and caprolactam to decline significantly in the short term. This means that PA6 chips will continue to receive some support from the cost side, and a sharp collapse in the short term is unlikely.

However, as July begins, the risks need to be reassessed. According to Gong Yuqian, an analyst at SCI99, caprolactam’s downward trend in June was difficult to reverse, while the pure benzene market is facing dual pressure from rising domestic supply and replenishment from imported cargo arrivals, leaving prices with little upward momentum. On the demand side, amid a “buy on the rise, not on the fall” mentality and high inventory pressure, downstream players have shown very little willingness to build stocks. If cost support weakens further, coupled with persistently sluggish downstream demand, the PA6 market will come under even greater pressure.

For enterprises with essential production needs, purchasing on demand remains a reasonable choice, and normal production should not be affected by waiting for prices to fall. However, traders and downstream enterprises planning large-scale stockpiling are advised to remain cautious. At a stage when market sentiment diverges from actual demand, the risks of chasing higher prices and stockpiling should not be overlooked.

Written at the End

The most contradictory aspect of the PA6 market in this round lies in:The sharp surge in sulfur prices is real, the rise in costs is real, but weak demand is equally real.

When price increases are driven by costs rather than demand, market resilience is often significantly weakened. Whether downstream orders can improve is the key variable determining whether the PA6 market can truly emerge from its difficulties.

Data source:Securities Times, 21st Century Business Herald, SunSirs, OilChem, SCI99, Tonghuashun iFind, Changjiang Securities research reports, etc.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

A Look at the Material Suppliers Behind SpaceX

-

Government's Triple Action, Enterprises' Three Arrows in Five Days, Semiconductor Reshuffle! What Signal Does Japan's Chemical Industry Release?

-

Global Chemical Giants Accelerate Production Capacity Restructuring, Dow and Celanese Optimize Global Industry Layout

-

Name change without tax change: POM Anti-Dumping Duty Rate Inheritance Implemented

-

Fire breaks out at jiangsu meiside!