Plasticizer Industry Chain Trading Guide For The Coming Week

1. Domestic Plasticizer Industry Chain Price Overview This Week

Analysis of the Domestic Plasticizer Industry Chain Market:This week, the plasticizer industry chain showed mixed performance, with octanol and DOP rising somewhat, while other products mainly declined. Specifically:

n-Butanol:During the period, the domestic n-butanol market mainly fluctuated within a narrow range. Market movements largely centered around low-end prices. On the one hand, operating rates at domestic producers were not high, and export orders were sold in a concentrated manner, leaving domestic producers’ inventory levels low and providing some short-term support to the market. On the other hand, after n-butanol prices fell to a phased low, product profitability hovered near the cost line, and mainstream producers showed a strong willingness to hold prices firm, limiting market fluctuations. Toward the weekend, some domestic plants saw short-term fluctuations, while available spot supply in the market continued to shrink. Mainstream producers showed a strong intention to raise prices, but downstream buyers followed up cautiously; high-priced transactions were sluggish, and market deals were mainly concluded at low levels.

o-XyleneDuring this period (June 5-11, 2026), the domestic phthalic anhydride market showed a generally weak downward trend. In the week, Sinopec's listed price was lowered by 100 yuan to 9,100 yuan/ton, which impacted market confidence. The downstream phthalic anhydride market has entered a demand off-season, with companies being cautious in their purchases and resistant to high-priced raw materials, leading to a continued weak demand side. Although phthalic anhydride holders do not face pressure to clear inventory, the slowdown in exports, combined with lower crude oil prices and a bearish sentiment in the aromatics market, resulted in slight downward adjustments in traders' quotations, but actual trading discussions were scarce, and bearish sentiment increased. On the supply side, with many units undergoing maintenance and tight spot circulation, there is some support for prices at a certain bottom level, but it is difficult to counteract the dominant weak pattern driven by demand. Throughout the week, the downstream market remained stagnant, with refineries having no further plans to adjust prices, leading to a stable market operation for now. Overall, the interplay between cost support and weak demand indicates that the phthalic anhydride market will continue to undergo weak consolidation in the short term.

Phthalic anhydride:During this period (June 5-11, 2026), the domestic phthalic anhydride market showed an overall weak downward trend, with persistently sluggish terminal demand being the core factor dominating the market. The raw material ortho-xylene experienced a slight decline, which weakened cost support. The main downstream plasticizer sector operated at low capacity, leading to reduced consumption of phthalic anhydride, and market sentiment was generally bearish. There were both maintenance and restart activities in phthalic anhydride production facilities, resulting in a relatively stable supply. Although manufacturers maintained high price offers under pressure from high costs, downstream purchases were mainly based on essential needs, and the significant price difference with naphthalene-based products hampered transactions, resulting in a lack of actual deal negotiations. The noticeable decline in the raw material industrial naphthalene intensified bearish sentiment, and although there were still orders for naphthalene-based production, the pressure to sell was gradually increasing, prompting some holders to offer discounts. In contrast, the ortho-xylene method maintained steady pricing due to expected reductions in supply. Overall, the continued weak demand is constraining market transactions, and the short-term outlook for phthalic anhydride remains with expectations of slight downward adjustments.

OctanolThis week, the domestic octanol market has shown a slight increase and remained firm. During this period, the domestic octanol capacity utilization rate continued to decline to around 60%, the lowest level this year. The profitability of octanol remains poor, with mainstream factories primarily focusing on contract sales, resulting in a low level of spot supply. Domestic factories do not face significant shipping pressure, as downstream demand is driven by necessity. There are no bearish expectations in the market. At the beginning of this week, some factories raised their offers, and downstream purchasing was relatively good. The market is expected to maintain a firm operation in the future.

DOPDuring this cycle, the domestic DOP market rose first, followed by some corrections. Downstream buyers purchased on demand, while market participants maintained a cautious attitude. Spot supply of the raw material 2-ethylhexanol declined, and long-term cost pressure persisted, prompting traders to hold firm on prices. Faced with rising 2-ethylhexanol prices, costs in the DOP industry increased accordingly. With upstream support in place, DOP traders also followed suit in maintaining firm prices. However, downstream demand did not show any substantial improvement, with buyers continuing to procure DOP only as needed, leaving DOP traders facing significant resistance in inventory movement. Subsequently, as the upward momentum of 2-ethylhexanol prices weakened and entered a more stable phase, the weakness in downstream DOP demand became increasingly prominent. To ease shipment pressure, more traders gradually offered price concessions.

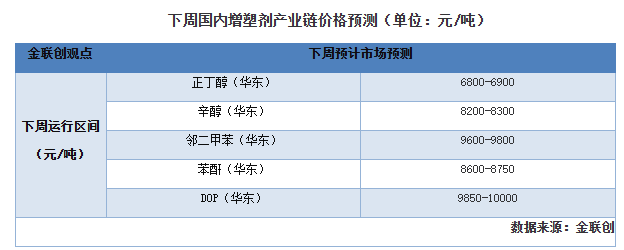

II. Analysis of Trends in the Domestic Plasticizer Industry Chain Next Week

Butanol and pentanol:This week, the domestic n-butanol market fluctuated within a narrow range. The inventory levels of domestic enterprises remain low. As the weekend approaches, some factories have shown short-term fluctuations, actively pushing for price increases. Looking ahead to next week, the demand outlook is average, with no significant improvement in demand expected. It is anticipated that downstream will mainly focus on low-priced essential purchases. As the concentrated exports have ended, some domestic factories still face pressure to sell spot goods. It is expected that they will primarily focus on active sales, but under high cost pressure, the extent of discounts is likely to be limited. Therefore, it is expected that next week will see a stalemate with narrow fluctuations. This week, the octanol market rose and maintained a strong performance. At the beginning of the week, some factories raised their offers, and downstream demand followed reasonably well. Major factories do not face selling pressure, which supports a strong market after the price increase. Looking ahead to next week, some domestic enterprises have recovery expectations, and the supply may show a month-on-month increase. The operating rate of downstream plasticizers is expected to maintain around 50-60%, continuing to focus on demand-based purchases. The octanol market lacks sustained upward momentum, and it is expected that next week will see the octanol market in a narrow range of fluctuations.

o-Xylene:Next week, China’s ortho-xylene market is expected to remain in a stalemate with a slightly weak and narrowly fluctuating trend. On the supply side, the restart of Yangzi Petrochemical’s phthalic anhydride unit has been postponed to late July, and with several other units still under maintenance, the industry operating rate will stay at a low level. Spot circulation will remain tight, providing bottom support for prices. However, constraints on the demand side are evident: the downstream plasticizer industry is gradually entering its traditional off-season, losses in the naphthalene-based phthalic anhydride sector continue, and operating rates are unlikely to improve, so purchases of ortho-xylene will remain limited to rigid demand. At the same time, reduced exports will further weaken demand support. Crude oil is fluctuating on the weak side, while aromatics are showing limited movement, offering little guidance from either costs or market sentiment. After Sinopec lowered its listed price this week, the market center has already edged lower. Although holders are not under pressure to clear inventories, their confidence in maintaining firm offers is insufficient amid demand weakness.

Phthalic anhydride:Next week, the domestic phthalic anhydride market is expected to continue its weak fluctuations, with a slight downward shift in the market focus. On the cost side, the raw material ortho-phthalic acid is likely to remain stable, providing some cost support for the ortho-phthalic anhydride; however, the cost support for naphthalene-based production is relatively weak, and the naphthalene-based phthalic anhydride may continue to weaken. In terms of supply, the overall industry operating rate is expected to decline. The ortho-phthalic production is anticipated to see reduced supply due to losses, and there are also minor maintenance plans for naphthalene-based facilities. Overall supply pressure is not significant, but there is no evident reduction. On the demand side, it remains the core bottleneck constraining the market. Terminal demand continues to be weak, with the main downstream plasticizer industry operating at low levels, leading to phthalic anhydride purchases being limited to just-in-time needs. Actual transaction discussions are light, and bearish sentiment in the market persists. Overall, the differentiated cost support combined with continued weak demand makes it difficult for the phthalic anhydride market to escape the weak pattern in the short term.

DOPFrom the perspective of supply and demand, the DOP industry is still seeing some shutdowns or production cuts, but major producers are generally maintaining normal operating rates, so spot supply remains stable. On the demand side, there has been no improvement. Market participants lack confidence in the outlook, buying interest remains cautious, and purchases of DOP are limited to small volumes for rigid demand. Therefore, although DOP producers have reduced operating loads, resistance to inventory digestion remains high, and the supply-demand imbalance persists. In terms of costs, upstream octanol has also seen reduced operating rates, but inventory digestion remains difficult, with prices mainly fluctuating within a range. Phthalic anhydride may continue to consolidate weakly. For DOP, cost support may weaken. Overall, DOP supply is expected to remain ample, with sellers prioritizing shipments. However, under the influence of the demand off-season, some moderate price concessions may occur. Considering poor profit margins and reduced operating rates, market fluctuations are expected to be limited, with prices generally showing a weak, gradual downward trend.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

A Look at the Material Suppliers Behind SpaceX

-

Government's Triple Action, Enterprises' Three Arrows in Five Days, Semiconductor Reshuffle! What Signal Does Japan's Chemical Industry Release?

-

Global Chemical Giants Accelerate Production Capacity Restructuring, Dow and Celanese Optimize Global Industry Layout

-

Name change without tax change: POM Anti-Dumping Duty Rate Inheritance Implemented

-

Fire breaks out at jiangsu meiside!