Net Profit Soars 50%, Costs 30% Lower Than Competitors! In a World Where Oil Prices Exceed $100, the Golden Age of Coal Chemicals Has Just Begun

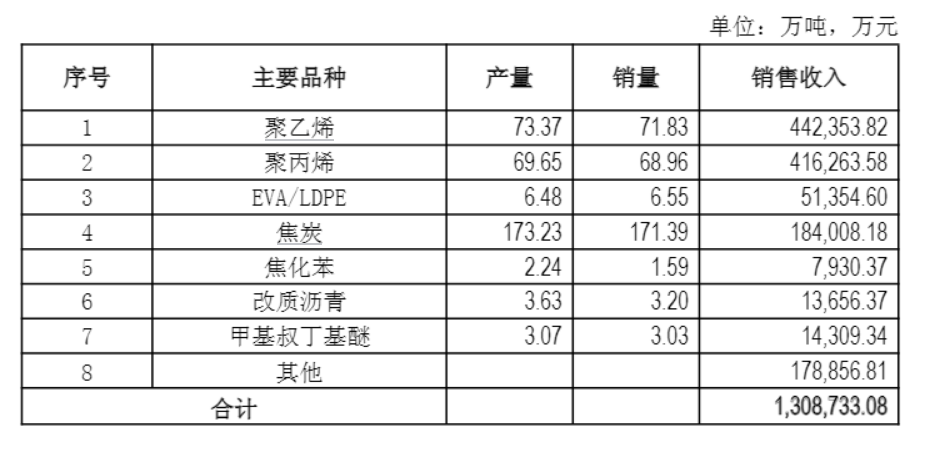

Recently, Baofeng Energy released a set of results that many peers envy: revenue reached RMB 13.237 billion (including RMB 130.8733 billion in main business revenue and RMB 1.494466 billion in other business revenue), an increase of 22.90% year-over-year; net profit attributable to shareholders was RMB 3.661 billion, surging by 50.23% year-over-year. These figures reflect not only the company's outstanding performance but also serve as a testament to the entire coal chemical industry's resilience through cyclical fluctuations.

As Brent crude oil breaks through the $100 per barrel mark from $60 at the beginning of the year, the landscape of the petrochemical industry is quietly being redrawn. Every dollar increase in oil prices adds pressure on oil-based olefins enterprises; while for coal-based enterprises, it means the cost scissors gap is further widened — the advantage is not shrinking, but expanding.

A financial statement, read two logic

To understand this quarterly report of Baofeng Energy, it is necessary to look at two dimensions: one is the intrinsic growth of its own performance, and the other is the extrinsicbonusdividend"bonus""""external benefits""external advantages" To understand this quarterly report of Baofeng Energy, it is necessary to look at two dimensions: one is the intrinsic growth of its own performance, and the other is the external benefits provided by the industry environment.

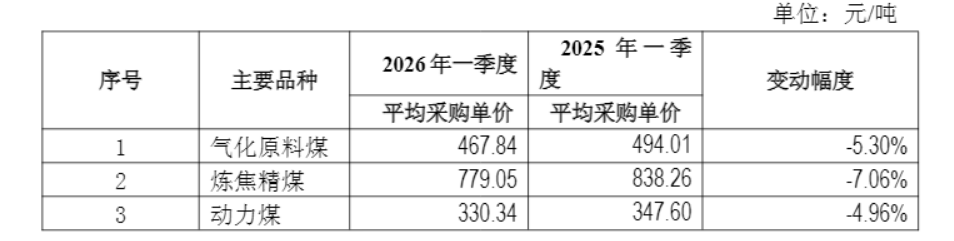

First, consider the endogenous factors. In the first quarter of 2026, Ningxia Baofeng Energy Group Co., Ltd.’s major raw material costs continued to decline: the average procurement price of gasification coal was RMB 467.84 per ton, down 5.30% year-on-year; coking coal was RMB 779.05 per ton, down 7.06% year-on-year; and thermal coal was RMB 330.34 per ton, down 4.96% year-on-year. With coal prices falling but product prices not declining proportionally, profitability naturally improved.

Looking at the external side, in 2025, the 3 million tons per year coal-to-olefins project of Baofeng Energy in Inner Mongolia will be fully operational, pushing the total capacity to over 5.2 million tons per year. This places it firmly at the top in China's coal-to-olefins sector, with a market share of about 34% nationwide. This expansion precisely hits the critical moment when the industry needs capacity the most: after years of intensive new installations, the supply and demand structure of the polyolefin industry is at a turning point, with the growth rate of capacity expected to slow significantly after 2026.

It is only with theof two logics that the profit elasticity of Baofeng Energy can be so large. Note: The term "" was initially left in Chinese as it directly translates to "" (overlay/) in this specific context, but for a more natural English expression, it could be better translated as: It is only with the combination of two logics that the profit elasticity of Baofeng Energy can be so large.

Oil prices break 100, the "moat" of coal chemical industry suddenly widens

If the internal logic is about Baofeng Energy doing its part right, then the drastic changes in external oil prices represent a "valuation re-rating" at the industry level.

Since March 2026, affected by the escalation of the Middle East geopolitical conflict and the disruption of shipping through the Strait of Hormuz, the international oil price quickly rose from around 60 USD per barrel at the beginning of the year, breaking through 100 USD per barrel by early May. This round of oil price surge has caused a deep-seated differentiation in the chemical industry.

From a cost structure perspective, the raw material cost (crude oil/naphtha) for oil-based olefins accounts for 70%-75% of the total production cost. A 10% increase in oil prices leads to a 7-8% increase in costs. In contrast, the coal raw material cost for coal-based olefins only accounts for about 25%-30%, making it much less sensitive to oil price fluctuations. According to Zhuo Chuang Information, as of the end of March 2026, the average total cost of coal-based olefins is approximately 6,801 yuan/ton, whereas that of oil-based olefins is as high as 10,700 yuan/ton—a difference of nearly 3,900 yuan per ton.

Converted into more intuitive figures: Baofeng Energy's coal-to-olefins break-even point is only around $45–50 per barrel of crude oil. With current oil prices slightly above $100 per barrel, Baofeng is operating in its most comfortable profit margin range. More importantly, this advantage is not static—it will continue to widen as oil prices rise further.

Guosen Securities explicitly stated in its April investment strategy report that after a significant rise in oil prices, coal prices remained relatively stable, leading to a widening oil-coal price spread. As a result, coal-to-olefins now enjoys a cost advantage of over 30% compared to oil-based routes, making it one of the most compelling and logically sound beneficiaries among chemical sub-sectors.

The "Counter-cyclical" Password of Coal Chemical Industry

Many people hold a fixed perception of coal chemical industry: it is a highly polluting and energy-intensive outdated industry, and should be scaled back under the “dual carbon” goals—so why is it still leading the way against the trend?

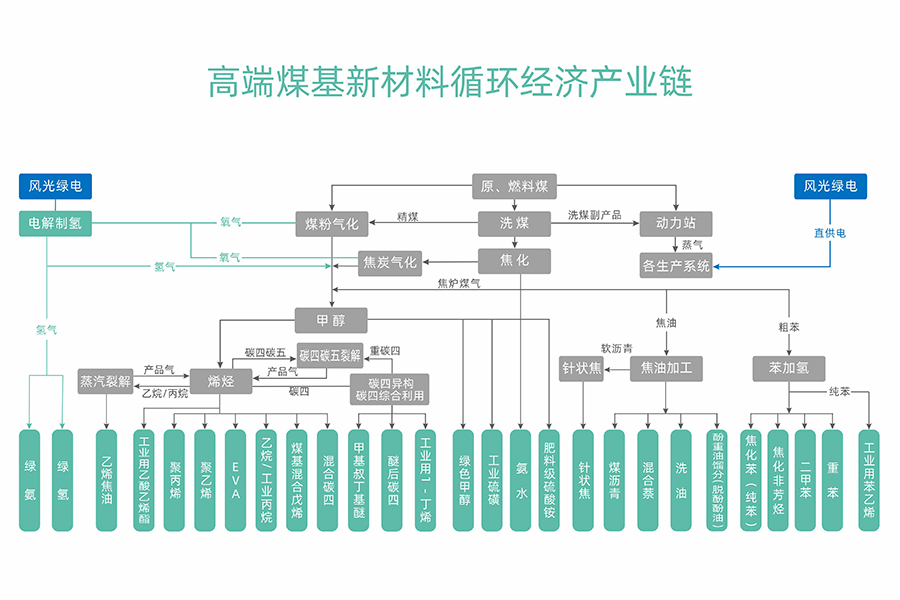

This perception is biased. Today’s leading coal chemical enterprises are no longer in the extensive, outdated form they were a decade ago. Represented by Ningxia BaoFeng Energy Group Co., Ltd., the new generation of coal chemical enterprises has established a highly integrated industrial chain—“coal → methanol → olefins → polyolefins → fine chemicals”—where waste or by-products from one stage serve precisely as feedstock for the next stage, and are continuously extending downstream toward higher-value-added products.

More importantly, China faces a practical constraint: as the world’s largest consumer of polyolefins, its domestic olefin demand is enormous, yet its inherent scarcity of oil and gas resources means it cannot rely entirely on oil-based production routes. Coal-to-olefins is China’s “energy security valve” under its specific resource endowment and is a strategic industry that must be sustained and developed over the long term.

From the supply side, the new capacity of polyolefins in recent years has mainly come from large coal chemical integrated projects. These projects generally have a cost advantage—Bao Feng's methanol cost per ton is 300-500 yuan lower than the industry average, and the total cost of the Inner Mongolia project is nearly 10% lower than that of the Ningxia base. This cost difference comes from the combination of scale, technology, and resources, and cannot be narrowed in a short period of time.

If you still find this insufficiently direct, consider the full-year 2025 results: Baofeng Energy reported revenue of RMB 48.038 billion, up 45.64% year-over-year; net profit attributable to shareholders reached RMB 11.35 billion, an increase of 79.09% year-over-year; and adjusted net profit hit RMB 11.519 billion, surpassing the RMB 10 billion mark for the first time. In contrast, the chemical industry as a whole faced headwinds that year, with fewer than half of the 164 listed chemical companies reporting year-over-year growth in net profit.

Expand the territory, the best is yet to come.

Baofeng's ambition is not limited to maintaining the current cost advantage.

On the production capacity side, the Ningdong Phase IV 500,000-ton-per-year olefins project is steadily progressing, with plans for completion and commissioning by the end of 2026. Upon completion, the total olefins production capacity will increase to approximately 6 million tons per year. Meanwhile, the Dingjialiang Coal Mine construction is accelerating, which will further enhance the self-sufficiency ratio of coal, leaving room for further reduction in raw material costs.

What is more noteworthy is the move to extend the industrial chain. Baofeng has submitted an application for approval to the Ningdong 5 million tons/year coal-to-ethylene glycol project, with the implementing entity being Ningxia Sainuo Chemical Co., Ltd. (wholly owned by Baofeng, with a registered capital of 1 billion yuan), which was just registered at the end of December 2025. The project is planned in two phases: the first phase will produce ethylene glycol, and the second phase will extend to polyester products (PET/PBT, etc.) and key raw materials such as PTA and BDO. This means that Baofeng is in the process of establishing a complete value chain from "coal-methanol-olefins-polyester/fine chemicals" and moving towards higher value-added downstream areas.

Image source: Baofeng Energy

The company's full-year target for 2026 is to produce and sell 56 million tons of olefins, with a capital expenditure of about 20 billion yuan. This pace is rarely seen in the industry as an aggressive posture.

Meanwhile, Baofeng has obtained self-operated import and export qualifications, significantly boosting its export volume, and gaining access to international markets represents a major variable. Compared to the increasingly competitive domestic polyolefin market, the export market offers a much higher ceiling.

2026: The Year of Rebound for the Coal Chemical Industry?

"2026 may be the turning point for the coal chemical industry's performance." This is the tone set by Founder Securities in a recent report. The judgment is supported by the rare resonance of several factors:

First, oil prices may remain high longer than the market expects.Even if the conflicts in the Middle East ease, the reconstruction of the energy supply chain and the restoration of market confidence will take time, making it difficult for oil prices to quickly fall back to below $60 in the short term.

Secondly, the structural easing of coal prices continues.Domestically, coal supply and demand will remain generally loose in 2026, with the coal market’s operational center expected to decline slightly compared to 2025. Low raw material costs coupled with high product prices constitute the most favorable operating environment for coal chemical enterprises.

Thirdly, the supply growth rate of polyolefins will significantly slow down after 2026.The peak period for this round of large-scale new facility rollouts is likely likely to end around 2026. After that, the industry's supply growth rate will significantly decrease, and price elasticity will gradually return. For Baofeng Energy, which has already completed its large-scale capacity layout, this will be the time to enjoy the benefits of its previous heavy investments.

Of course, risks also need to be addressed. Fluctuations in product prices, uncertainties in geopolitical situations, delays in project approval processes, and the cash flow pressure from capital expenditures of about 20 billion yuan per year are all variables that require continuous attention.

However, from a longer-term perspective, the renewed public attention on coal-to-chemicals essentially represents a strategic window of opportunity for China's domestic chemical industry amid global energy market turbulence. Baofeng Energy's decision to continue increasing its investments at this juncture reflects its own strategic bet.

Editor: Lily

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Continental Plans to Begin Sale of ContiTech in Early 2026

-

Mastering Screw Configuration and Pressure Management Strategies to Unlock the Secrets of "Efficiency and Cost Reduction"

-

Pakistan opens transit corridor for goods from multiple countries; explosion at japanese pharmaceutical plant leaves five injured, two seriously

-

Daily Review: Operating Rates Decline, Polypropylene Powder Market Prices Surge

-

BASF Delivers First Batch of Innovative Cathode Materials for Semi-Solid-State Batteries to Weilan New Energy