MDI’s Four Major Producers All Raise Prices! Multiple Units Shut Down!

Recently, the global chemical industry has welcomed an unprecedented wave of price increases. As the "pillar of stability" in the polyurethane industry chain, the MDI market has suddenly undergone a dramatic change: domestic leader Wanhua Chemical took the lead by raising the MDI quotation by 4,000 yuan per ton.

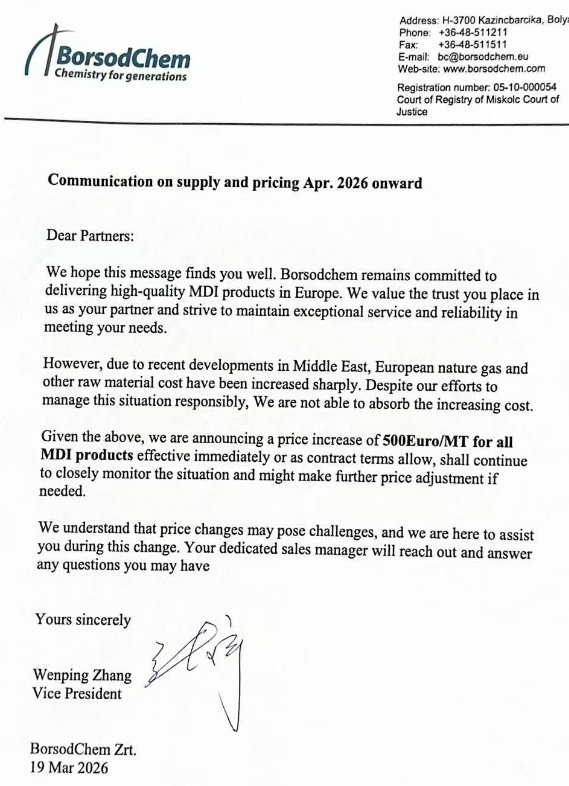

On March 19, 2026, BorsodChem, a subsidiary of Wanhua Chemical in Hungary, announced that the price of all its MDI products will be increased by €500 per ton (equivalent to RMB 3,982 per ton), effective immediately or as permitted by contract terms, for all supplies starting from April.

Bosid Company clearly stated in the price increase notice that the price adjustment is due to the recent developments in the Middle East, leading to a sharp increase in the cost of European natural gas and other raw materials.

International giants BASF, Dow, and Huntsman closely followed, simultaneously announcing price hikes across Europe, the Americas, and Asia-Pacific markets, with increases ranging from €200 to €500 per ton.

Scroll up and down to read more content

BASF: On March 23, BASF announced that starting today or when contract terms allow, it will increase the prices of Lupranate MDI and Lupranate TDI in East Asia (excluding mainland China) by 500 USD/ton.

Dow announced on March 5 a price increase of €200 per ton for MDI products in Europe and $300 per ton in India, the Middle East, and Africa.

Huntsman: On March 5, Huntsman became the first to impose a €200/ton natural gas surcharge on all MDI products in Europe, the Middle East, Africa, and India (EMEI), and explicitly stated that this surcharge will be dynamically adjusted in response to geopolitical developments.

As a core raw material in the polyurethane industry chain, fluctuations in the price of MDI directly affect numerous downstream industries such as coatings, home appliances, automobiles, and construction. The current global MDI price hike is not coincidental but the result of a combination of factors including geopolitical conflicts, energy crises, and high industry concentration, serving as a clear testament to the global chemical industry entering a "war premium" mode.

According to estimates, the profit margin of MDI/TDI fell by 15%-25% in March compared to the end of February, and the industrial chain's profit structure is undergoing reconstruction.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

Deadly Impact: Hormuz Strait Blockade Sparks Shortage of Plastic Raw Materials, Threatening Shutdowns at Japanese and Korean Chemical Plants

-

BASF's $8.7 Billion Zhanjiang Site Fully Operational, Covestro, SABIC, Arkema and Other Plastics Giants Double Down on China

-

Massive Loss of $960 Million! Wansheng Co., Ltd. Sees Rising Revenue But Declining Profits—Why Did the Phosphorus-Based Flame Retardant Leader Falter?

-

SABIC Declares Force Majeure on Styrene Monomer and Methanol Production; Middle East Chemical Operations Halted

-

BASF Delivers First Batch of Innovative Cathode Materials for Semi-Solid-State Batteries to Weilan New Energy