May Embodied Intelligence Financing: Noise Subsides, Mass Production Accelerates

In the past May, the embodied intelligence sector delivered a rather contradictory report card.

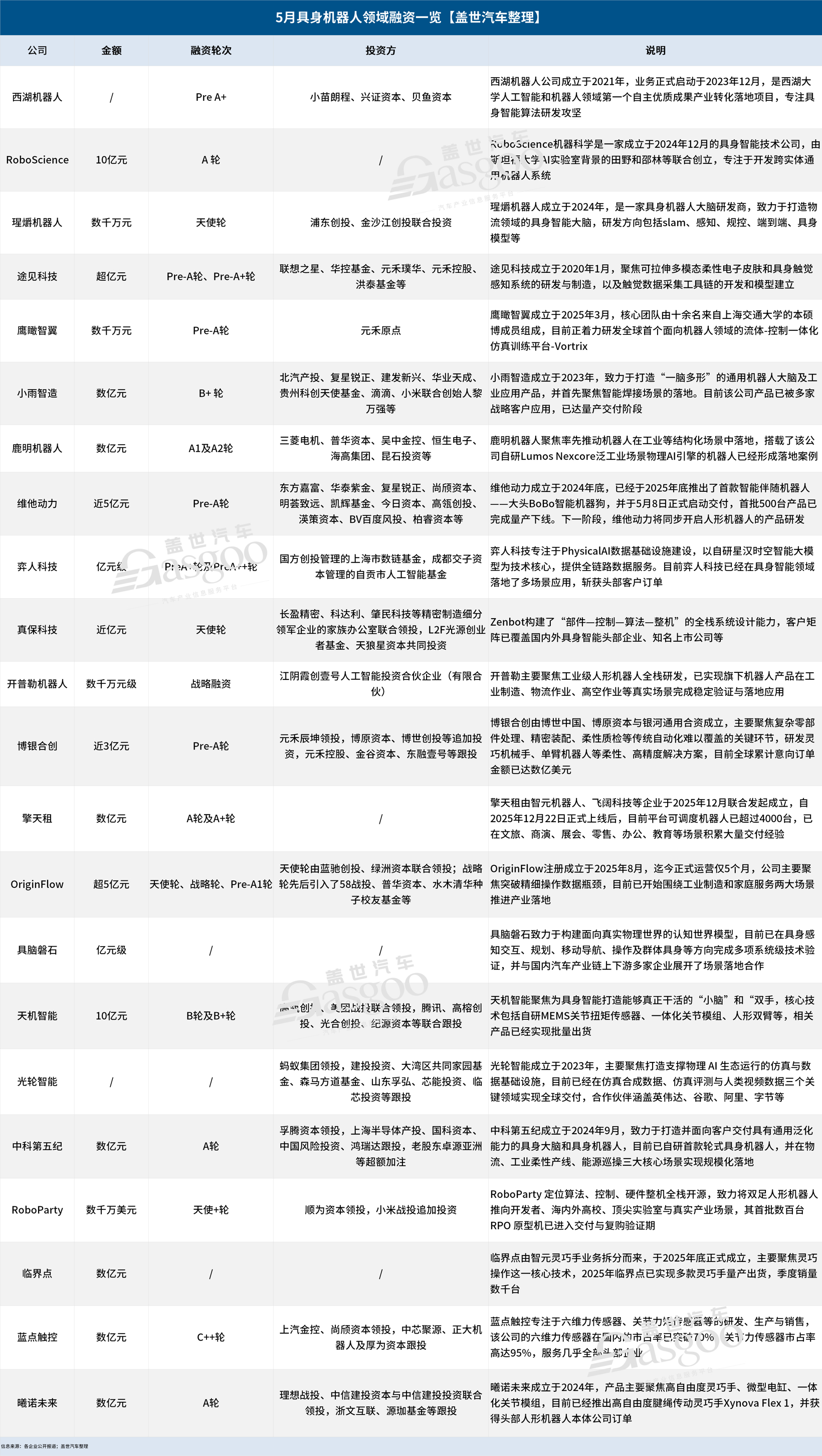

On the one hand, RoboScience secured 1 billion yuan in Series A funding, while early-stage projects such as LimX Dynamics, Vita Dynamics, and the Fifth Epoch of the Chinese Academy of Sciences also successively landed financing rounds worth hundreds of millions of yuan, showing that large amounts of capital continue to concentrate in the leading players. On the other hand, both the total number of financing events and the number of mega-round financings of 1 billion yuan or more in May saw a marked decline compared with the previous few months.

Behind this is a brutal shift in the entire industry from "telling stories" to "getting things done."

The financing list for May, like a prism, reflects the multiple pulls between capital logic, industrial structure, and the implementation of technology.

“ ”,But the "water seller" is quietly making money.

According to incomplete statistics from Gasgoo, 22 financing deals were publicly disclosed in May in China’s embodied robotics and related core components sectors. By comparison, there were 35 and 31 such deals in March and April, respectively, indicating a clear downward trend.

However, the cooling in May was in fact highly aligned with the shift in sentiment across the primary market: in May 2026, China’s domestic primary market recorded 339 investment deals, down 153 from the previous month, with total investment amounting to RMB 89.722 billion, down 28.1% month-on-month.

In other words, the entire primary market hit the brakes in May.

In the embodied intelligence sector specifically, the largest financing round in May came from RoboScience, which secured 1 billion yuan in its Series A round.

Founded at the end of 2024, RoboScience is dedicated to building a general-purpose embodied large model and has independently developed the VLOA large model. Building on this foundation, RoboScience has further developed its own robotic embodiment, providing a physical carrier for the large-scale real-world deployment of the VLOA large model.

RoboScience’s latest major funding round also, to some extent, reflects capital’s endorsement of its technical approach and commercialization potential amid the investment boom in “embodied AI brains.”

It is worth noting that this is RoboScience’s second round of financing this year. Earlier in February, the company had already completed a Pre-A financing round worth hundreds of millions of yuan. Since 2025, RoboScience has completed four rounds of financing in total, clearly demonstrating the high level of recognition it has received from investors.

Another 1 billion yuan in financing came from Tianji Intelligent.

Image source: Tianji Intelligence

However, Tianji Intelligence has already entered its Series B stage, so in a landscape where Series A rounds worth over RMB 1 billion are becoming increasingly common, this scale is not particularly surprising. Moreover, the RMB 1 billion refers to the combined total of its Series B and Series B+ financing.

In addition, companies such as Luming Robotics, Weita Power, Boyin Hechuang, Qingtian Rental, Zhongke Fifth Era, and Xinuo Future have also secured hundreds of millions in financing at the A round or Pre-A round stage.

Overall, capital remains highly enthusiastic about placing bets on early-stage projects. From another perspective, however, this also indicates that the embodied intelligence sector is still in the early stages of technological exploration and product commercialization.

From the perspective of sector distribution, unlike the early-stage focus of capital on foundation model companies, nowadays every core link in the embodied intelligence industry chain has the potential to attract funding.

For example, Boyin Hechuang focuses on core components for industrial scenarios such as precision assembly and flexible quality inspection; Xinuo Future specializes in dexterous hands; CAS Epoch V develops embodied intelligence “brains”; and BluePoint Tactile produces six-axis force sensors. None of these are whole-robot manufacturers, but rather key upstream players supporting the real-world deployment of embodied robots.

The shift in capital flows reflects a deep transformation in the industry: the autonomy and control of the industrial chain is replacing "whole machine manufacturing" as the new investment focus.

The logic behind this is not complicated.

On the one hand, after intensive financing from 2025 through the first quarter of this year, leading ontology vendors are basically not short of money.

Moreover, players such as Galaxy General, Qianxun Intelligence, Songyan Power, Xinghaitu, Jiajia Vision, and Independent Variable have each secured at least one round of financing exceeding 1 billion yuan this year, with valuations all surpassing 10 billion yuan, and some even exceeding 20 billion yuan. For new capital entrants, the threshold for these targets is already too high—either they cannot afford to invest or there is no equity share available.

On the other hand, compared to manufacturers of complete systems, betting on the determinism of core components is clearly higher. After all, regardless of who the eventual market winner is—be it bipedal or wheeled, industrial or domestic—robots will always need joints, chips, dexterous hands, and sensors.

Image source: Xino Future

This logic is akin to Huawei's choice to become a "supplier of incremental components for smart cars" rather than entering the market to manufacture complete vehicles—making money as a "water seller" and betting on the rise of the entire industry rather than the success or failure of a single company.

Looking deeper, the shift in capital from “investing in complete machines” to “investing in core components” also indicates that a change is underway: the division of labor in the embodied intelligence industry chain is beginning to take shape.

When the industry no longer requires every company to build an entire robot from scratch, but instead has some specializing in joints, others in sensors, and still others in dexterous hands, it means the industry is moving from the “workshop” stage into a stage of “specialized collaboration.”

From this perspective, the current shift in capital flows is merely the “shadow” cast by this trend on the financing side.

Demo is no longer valuable, and investment logic is being rewritten.

The cooling in financing in May, on the surface, was highly in sync with the marginal tightening of overall macro liquidity and the broader pullback in the primary market. Therefore, this does not mean that the embodied intelligence sector has entered a downward trend.

As of now, entering June, financing activity in the embodied intelligence sector has been rapidly picking up.

According to Gaishi Automotive Observations, in just the past few days, several companies including Jianzhi Robotics, Heiman Technology, Xingyuan Intelligence, Shouyi Technology, Qianxun Intelligent, and Xingchen Intelligence have disclosed new financing. Among them, Qianxun Intelligent and Xingchen Intelligence secured 1.5 billion yuan and 1 billion yuan in their latest rounds, respectively.

From this perspective, the pullback in May looks more like a brief “breather” than a trend reversal.

But the return of popularity does not mean the revival of the old logic. What is truly changing is the investment logic itself.

Since the outbreak of embodied intelligence, the early-stage valuations of companies have been primarily driven by "technology narratives." Whose humanoid robot can do a backflip, whose dexterous hand has higher degrees of freedom, and whose large model has a greater number of parameters—these metrics are directly linked to high fundraising amounts and elevated valuation levels.

But now, this logic is becoming ineffective.

A senior executive at a leading humanoid robotics company summarized investors’ current screening criteria in three dimensions: commercialization capability, deployment capability, and technical foundation. Put in plain language: can it be sold, can it be put to use, and can it keep evolving? If any one of the three is missing, it’s just a “story.”

Recently, the intensive entry of industrial capital has provided the most direct evidence for this judgment.

Image source: Boyin Hechuang

Industry giants such as Xiaomi, Li Auto, BYD, Geely, CATL, and Bosch are continuously increasing their investments in the field of embodied intelligence, leveraging their own advantages in industrial chains, scenarios, and funding to deeply layout the complete machines and core components sectors.

It should be noted that industrial capital may be less sensitive to valuation than financial VCs, but it has extremely high requirements for business logic and industrial synergy. In particular, what industrial capital brings is not just money, but also real order scenarios and supply chain resources.

From this perspective, a company that secures industrial capital is effectively obtaining, at the same time, investment funding, seed customers, manufacturing partners, application scenarios, and other forms of support.

Conversely, companies that lack the ability to implement industrial projects and are without the support of industrial capital may gradually fall behind in the processes of financing and mass production, ultimately being phased out by the market.

This means that this shift in the logic of industrial investment is, in fact, also a process of natural selection.

Even in the view of Matrix Super Intelligence founder and CEO Zhang Haixing, a shakeout in the humanoid robotics industry could come as soon as within 18 months. By this estimate, by around the end of 2027, most of the dozens of humanoid robotics startups currently in the market will face elimination.

Chen Tongqing, co-founder of TStone Zhihang, also provided a similar judgment. He believes that the process of convergence in the embodied intelligence industry is very similar to that of autonomous driving. Initially, there are many players, but in the end, it will concentrate on a few leading companies, while the remaining players will either transform, be merged, or be dissolved.

The subtext of this statement is clear: not all companies currently riding the wave will be able to wait for the wind to truly blow in their favor. When the money is no longer "flooding in," it will become evident who has been "swimming naked."

After mass production of tens of thousands of units.,The Real Showdown Just getting started

Although financing activity briefly cooled in May, the pace of mass production on the industrial side did not slow down. On the contrary, several leading companies are now rapidly crossing the same threshold.

Production scale of 100,000 units is becoming the new benchmark for leading players.

Zhiyuan Robot is the one that runs the fastest.

Image source: Zhiyuan

At the end of March, Zhiyuan announced the official rollout of its 10,000th general-purpose embodied robot. Just by the end of 2025, Zhiyuan had only just surpassed the production milestone of 5,000 units. This means that it took Zhiyuan only 3 months to go from 5,000 to 10,000 units, setting a new record for the production ramp-up speed of general-purpose embodied robots in the country.

Close on its heels, Zhishen Technology also crossed the 10,000-unit mass production threshold at the end of May, taking about five months to go from 5,000 to 10,000 units.

In early June, Unitree also announced that the cumulative production of a single model of its bipedal humanoid robot had reached approximately 11,000 units, a figure that does not yet include other models or wheeled chassis products.

In just three short months, three companies successively joined the “10,000-unit club,” something that would have been hard to imagine just a year ago.

Behind the continued expansion of mass production at leading companies, the industry’s overall pace of mass production is also accelerating.

At the end of March, the country’s first automated production line for humanoid robots with an annual capacity of over 10,000 units, jointly developed by Dongfang Precision and Leju Robotics, officially began operation, rolling one robot off the line every 30 minutes. In May, Zhongqing Robotics’ Honghualing base in Shenzhen was put into operation, further shortening the production cycle to one robot every 15 minutes.

Embodied intelligence is moving beyond the exploratory stage of small-batch trial production and truly entering the stage of standardized manufacturing.

But new problems also arise: when large numbers of robots roll off the production line, where will they be headed?

The answer is not optimistic.

Due to the wide variety and complexity of real-world application scenarios, which include numerous edge cases and unconventional situations, the large-scale application market for high-performance general-purpose robots is far from mature. Currently, commercial applications are mainly concentrated in limited scenarios such as quadruped robot inspection, scientific research and education, and consumer entertainment.

Moreover, even in the consumer market, the high price and limited functionality still pose significant challenges to large-scale commercial adoption.

Not to mention that, in broader industry scenarios, a complete commercial closed loop has yet to be formed.

Image source: Unitree

The shipment volume of Yushu has completely exposed this gap—by 2025, Yushu's humanoid robots will ship over 5,500 units, ranking first in the world, but 70% of the revenue comes from research and education, while industrial applications account for only 9%.

Subsequently, Wu Binghao, the technical director of Yushu Technology, pointed out that embodied intelligence needs to overcome three major challenges to surpass the "ChatGPT moment": first, to improve the model's ability to express tasks and break through the generalization bottleneck; second, to enhance the model's utilization of diverse data and strengthen knowledge transfer; third, to improve the scale effect of reinforcement learning and achieve optimal capabilities for multiple tasks.

These three hurdles cannot be overcome simply through financing and capacity expansion.

The contradiction between the mass production of tens of thousands of units and the 9% industrial orders is essentially not a technical issue, but a mismatch in rhythm. After all, production lines can be quickly established with capital, while trust in industrial scenarios can only be gradually built over time.

This is also the biggest hidden risk in the current industry: capacity utilization is more important than capacity scale.

Therefore, amid the drumbeat of mass production in the tens of thousands, a sharper question has been thrust into the spotlight: how far away is the “ChatGPT moment” for embodied intelligence?

In this regard, Yang Zhongkai, the head of product technology at Xingzhi Power, believes that the next five years may be a window period for the landing of consumer-end embodied intelligence, as the current maturity of the supply chain and model capabilities are converging. In this process, production capacity will be key: if market demand surges, the ability of companies to quickly match production capacity will directly determine who can seize the opportunity.

Vice President of Product Ecosystem at Tiangong Robot, Chen Wei, has a more optimistic view. "I believe that in five years, robots will be everywhere—largely speaking, robots will be commonly used for inspection, care, and sales functions in parks, shopping malls, and small shops. Some companies have already begun to implement related applications in bulk. In areas such as dangerous zones, industrial parks, and community inspections, as well as maintenance of power grid equipment in industrial parks, there will be noticeable changes in the next two to three years, and by five years, the application scenarios for robots will be even more extensive."

Moreover, in his view, robots may become as commonplace as computers are today within the next five years. “At present, it is still relatively difficult for an individual to own a robot of their own, but I believe that in the future, owning a robot will be about as easy as assembling a computer online: you will simply choose the corresponding controller, battery manufacturer, joint manufacturer, sensing component supplier, and casing manufacturer, and so on, and then customize a robot exclusively for yourself.”

But beyond the optimistic expectations, one basic fact must be faced squarely: the prerequisite for a market boom is that robots can truly “do the work.”

The matter of "being able to do the work" is still the most difficult hurdle for the entire industry to overcome.

According to Morgan Stanley's forecast, by 2036, the global adoption of humanoid robots will reach 24.4 million units; by 2050, the global stock of humanoid robots will reach 1 billion units, while the annual revenue of the global humanoid robot market will reach as high as $7.5 trillion.

This figure is enticing enough, but the road to that goal is bound to be a long elimination contest. The cooling of financing in May can be seen as the prelude to this contest.

When capital no longer floods in, when demos are no longer the core competitive advantage, and when mass production of thousands of units forces the industry into the test of delivery capability—those companies stuck in the demo stage, those that can produce products but cannot enter the market, and those that have secured funding yet cannot achieve repeat purchases are seeing their survival time window rapidly shrink.

From "telling stories" to "submitting assignments," from "comparing financing" to "comparing delivery," embodied intelligence is undergoing a rite of passage.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

A Look at the Material Suppliers Behind SpaceX

-

Breaking news! formosa petrochemical olefins division lifts force majeure! asia olefins supply and demand dynamics face another reversal

-

Ethylene: Production Capacity Accelerates Expansion, Global Industry Landscape Is Being Reshaped

-

Breaking News! Suzhou Fuyang Chemical Explosion! Exclusive Analysis By Plastics World Of 4 Major Impacts On The Chlor-Alkali Industry Chain

-

Target To Reduce Plastic By 30%! South Korea Enters Plastic Recycling Controversy, Involving National Interests