Jiangsu Eastern Shenghong Surges 320%, Rongsheng Petrochemical Jumps 378%: Polyester and Refining Giants Rally from Darkest Hour

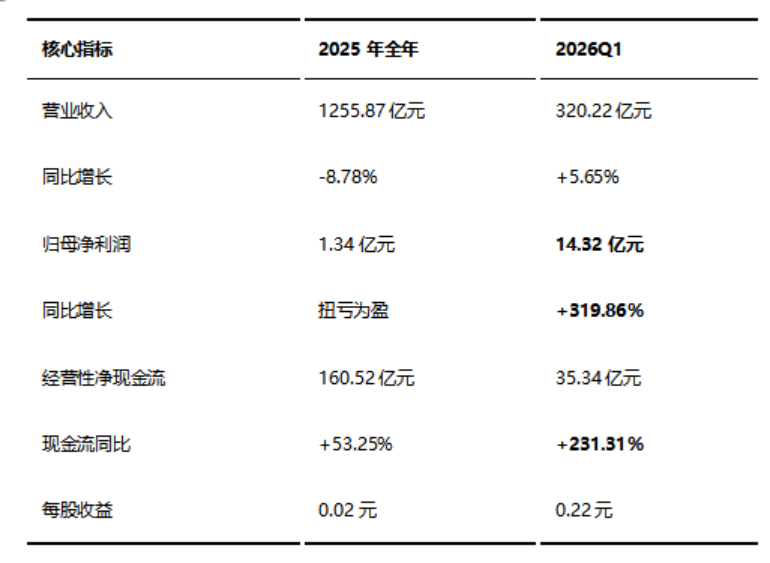

On the evening of April 28, Dongfang Shenghong simultaneously released its 2025 annual report and its Q1 2026 report. The two sets of data show a stark contrast: for the full year of 2025, the company reported a net profit attributable to shareholders of RMB 134 million, while in Q1 2026 alone, net profit attributable to shareholders surged to RMB 14.32 billion, a year-over-year increase of 319.86%.

In the first quarter of 2026, Sinochem's net profit was 2.815 billion yuan, up 378% year-on-year. The leading polyester and refining companies have all "soared" collectively.

Same company, drastic difference in performance within half a year. Is this a short-term rebound or an industry turning point?

Plastics Insight has compiled the latest financial reports of industry leaders such as Eastern Shenghong, Rongsheng Petrochemical, and Xin Fengming, aiming to uncover the true drivers behind this round of explosive earnings growth.

From "the Darkest Hour" to "Collective Outbreak" for the Refining and Polyester Industry

Check the 2025 performance of Dongfang Shenghong.

The annual revenue was 125.87 billion yuan, a decrease of 8.78% year-on-year. The net profit attributable to the parent company was 134 million yuan, although it turned a profit compared to the previous year, the non-recurring profit after deduction was still a loss of 543 million yuan. This data "doesn't look good," but it's not an isolated case. 2025 is a typical cyclical bottom year for the polyester refining industry.

There are three core reasons. First, the high costs upstream are oppressive. The average annual price of Brent crude oil fluctuates between $70-80 per barrel, and the price of PX remains high due to fluctuations in overseas facilities. The cost of raw materials upstream continuously squeezes refining and petrochemical enterprises.

Second, downstream demand remains weak. The PTA and polyester sectors have been affected by slowing textile and apparel exports and slower-than-expected domestic consumption recovery, leading to persistently low operating rates and downward pressure on product prices, squeezing margins to their limits amid "squeezing from both ends."

Third, the release of production capacity coincides with an industry downturn. Oriental Fusheng's 16 million tons per year integrated refining and petrochemical project is in the phase of capacity ramp-up, with high fixed costs, but product prices are low, making it difficult to fully realize the integrated advantages in a narrow pricing environment.

Compared with peers, the industry shows significant differentiation. Sinopec Energy's 2025 net profit attributable to shareholders is 848 million yuan, an increase of 17.09%, demonstrating stronger cycle resistance due to larger scale effects and more mature plant operations. In contrast, Dongfang Shenghong's non-GAAP net profit remains negative, indicating that its core business profitability has not been fully restored.

Entering the first quarter of 2026, the style suddenly changed.

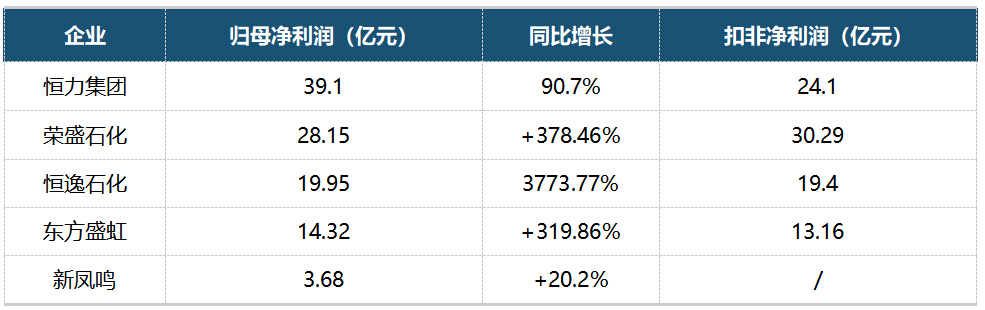

The five leading polyester refining and chemical companies saw explosive first-quarter performance across the board.

More importantly, the net profit of Dongfang Shenghong in the first quarter of 2026, 1.432 billion yuan, is 10.7 times that of its full-year 2025 net profit of 134 million yuan. Rongsheng Petrochemical's Q1 net profit reached 2.815 billion yuan, also setting a new high for quarterly profits in the past four years.

This is not an individual case for one company, but a clear signal that the entire upstream raw material sector is entering a period of comprehensive profitability.

II. Why did the upstream suddenly "make a fortune"?

The core drivers come from three aspects, with the first being the comprehensive recovery of price spreads, which is the primary driver behind the surge in earnings this round.

Starting from the fourth quarter of 2025, the price spreads in the polyester industry began to systematically recover. The PX-crude oil spread increased from a low of about 170 USD/ton in April 2025 to 352 USD/ton in December, rising by more than 180 USD/ton. The PTA-PX spread expanded from 200 RMB/ton to 335 RMB/ton.

Polyester end profit also improved, with processing fees for both filament and staple fiber rising simultaneously. For companies like Dongfang Shenghong with 16 million tons of refining and petrochemical capacity, and Rongsheng Petrochemical with 40 million tons, the profit elasticity from margin recovery is significant.

Finally, integrated industry leaders’ cost advantages amplify earnings elasticity. During price-up cycles, who benefits the most? The answer is integrated industry leaders. Thanks to economies of scale and full-chain integration, these leading companies enjoy per-ton product costs 10%–15% lower than smaller and medium-sized producers. When product prices rise, with relatively fixed costs, nearly all the price increase flows directly into earnings. For instance, Hengli Petrochemical’s global-scale integrated refining and petrochemical operations and Orient Yuhong’s strategic across oil, coal, and gas see their advantages magnified exponentially in an environment of widening price spreads.

From Dongfang Shenghong's 134 million to 1.432 billion, and from Rongsheng Petrochemical's 848 million for the whole year to 2.815 billion in a single quarter, the turning point of the polyester refining industry cycle has been confirmed. The competitive landscape of the industry is accelerating towards the concentration of integrated leaders. Small and medium-sized factories are being rapidly phased out in the high-cost, narrow-margin environment, while the leaders are building increasingly wider moats with their scale, cost, and depth of the industrial chain.

Editor: Carrie

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Continental Plans to Begin Sale of ContiTech in Early 2026

-

$4 Billion! Medtronic Makes Another Acquisition

-

Profit and Revenue Growth Struggle to Conceal Debt Repayment Pressure; Success of Kingfa Sci & Tech's High-End Strategy Yet to Be Seen

-

BASF Delivers First Batch of Innovative Cathode Materials for Semi-Solid-State Batteries to Weilan New Energy

-

Why did a century-old european dental instrument giant relocate its manufacturing hub to china?