Cost Floor And Demand Ceiling: PVC Trapped In A Squeeze

The PVC market has recently shown a rather contradictory situation: the cost trends of the two production processes, calcium carbide method and ethylene method, are moving in opposite directions, coupled with the continued downturn in the real estate market, leaving PVC in an awkward "squeeze for survival" situation.

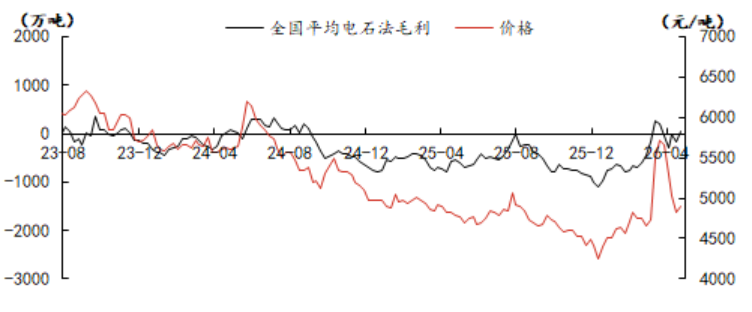

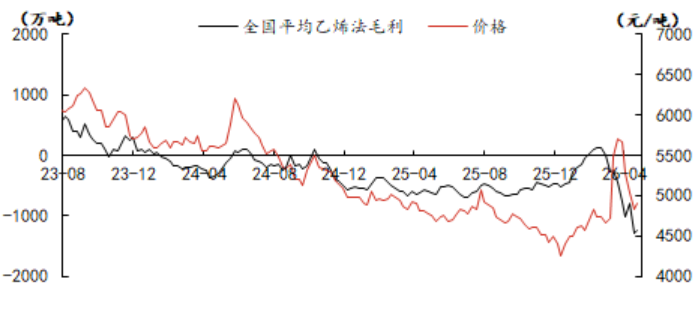

From the cost perspective, the calcium carbide-based PVC production method has witnessed a long-awaited bottom support. As of April 27, the mainstream trading price of calcium carbide in Wuhai rose by RMB 100 per ton to RMB 2,250 per ton, primarily due to prolonged losses forcing calcium carbide producers to cut output; industry operating rates have consequently declined to approximately 60%, a historically low level. This has lifted production costs for calcium carbide-based PVC by roughly RMB 150–200 per ton. In stark contrast, ethylene-based PVC faces a completely different situation. Influenced by the geopolitical situation in the Middle East, domestic ethylene prices have surged nearly 88% since late February and remain at elevated levels, pushing ethylene-based producers into severe losses; industry operating rates have dropped from over 80% post-Spring Festival to about 65% currently. This cost divergence between the two production routes has led to a marginal tightening in overall PVC supply.

Gross Profit Margin and Market Price Trend Chart for Calcium Carbide-based PVC Production

Profit Margin and Market Price Trend Chart for Ethylene-based PVC Production

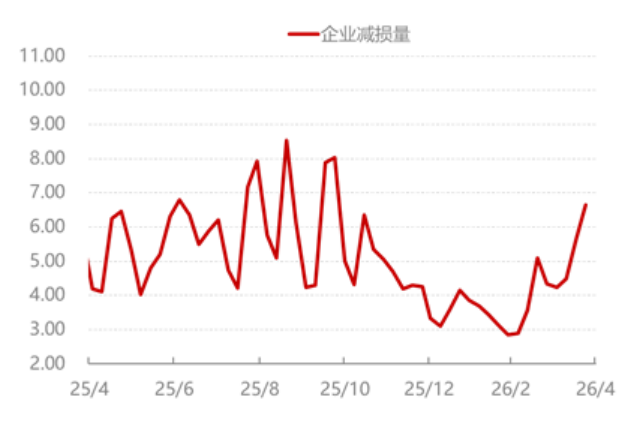

At the same time, the spring maintenance is proceeding as scheduled. As of the fourth week of April, the overall operating rate of the PVC industry is about 74.5%, a decrease of about 5 percentage points from the peak in March. The loss of production due to maintenance continues to increase, and the supply is marginally tightening. Although the social inventory has been decreasing slightly, with the sample inventory in East China and South China decreasing by 1.65% month-on-month, the total inventory has increased by 38.28% year-on-year, and the absolute inventory remains at a high level. The pressure to reduce inventory has not been substantially relieved, and the market still faces a high burden of digesting existing stock.

PVC production enterprise maintenance loss volume

A more fundamental issue lies on the demand side. In the first three months of 2026, nationwide real estate development investment fell by 11.2%, and the area of newly started residential buildings dropped sharply by 20.3%. As the largest downstream consumer of PVC, the deep adjustment in the real estate sector has directly suppressed orders for mainstream products such as pipes and profiles. The overall operating rate of downstream product manufacturers remained between 45% and 50%, and the willingness to stock up before the May Day holiday was low, with most companies focusing on essential procurement. Even though overseas suppliers such as Japan's Shin-Etsu have continuously raised their export prices, the impact of these increases remains limited in the face of weak domestic demand.

Currently, PVC is caught between cost support and demand ceiling. The rebound in calcium carbide prices and supply contraction due to spring maintenance provide short-term support to the market, limiting the downward price trend. However, high inventory levels and a double-digit year-over-year decline in real estate investment form an insurmountable ceiling for price increases. Whether the market can break out of this stalemate depends on whether the overseas supply contraction can continue to intensify, and whether the macro policy support for the real estate sector can gradually be transmitted to the PVC consumption end. Before that, PVC is likely to continue struggling in this difficult situation.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Continental Plans to Begin Sale of ContiTech in Early 2026

-

$4 Billion! Medtronic Makes Another Acquisition

-

Profit and Revenue Growth Struggle to Conceal Debt Repayment Pressure; Success of Kingfa Sci & Tech's High-End Strategy Yet to Be Seen

-

BASF Delivers First Batch of Innovative Cathode Materials for Semi-Solid-State Batteries to Weilan New Energy

-

Why did a century-old european dental instrument giant relocate its manufacturing hub to china?