ABS Force Majeure Leads to Decline in Plant Output

Lead: The Middle East situation has persisted for a month, and during the fourth trading week of March, production cuts at ABS plants have gradually become evident due to force majeure disruptions in raw material supply and the inability to pass on cost pressures.

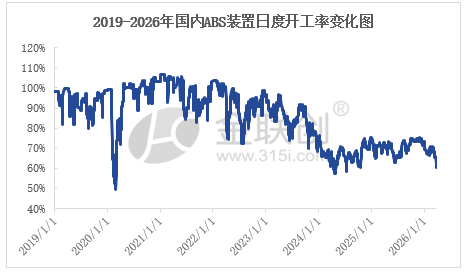

ABS production is continuously declining

Data Source: JLC

Entering the fourth trading week of March, the ABS industry is increasingly feeling the impact of raw material supply force majeure triggered by the Middle East situation and high cost pressures, as Shandong Lihua Yi and Zhejiang Petrochemical ABS units progressively curtail production. Coupled with scheduled maintenance at Guangxi Changke and Sinopec Ineos Ningbo ABS facilities, the ABS operating rate has continued to decline throughout March.

ABS production drops to historical low

Data Source: JLC

As of March 2026, according to Jinliancai's rough estimate, the ABS plant utilization rate has dropped to around 60%, which is at historically low levels, and there is still potential for further decline. Looking back at the previous two instances when the daily ABS utilization rate fell below 60%, one occurred in 2020 due to the public health event, which caused uncontrollable circumstances and halted logistics and transportation. This led to increased inventory pressure for ABS petrochemical manufacturers, forcing them to cut production intensively, and the daily utilization rate dropped below 50%. The second instance occurred after the intensive capacity expansion in 2023, which significantly increased the supply pressure in the ABS market. Since the fourth quarter of 2023, losses have intensified, and in 2024, the willingness of petrochemical companies to operate at full capacity has clearly declined, causing the daily utilization rate to fall below 60% twice.

ABS start-up still expected to decline

Looking ahead to April, some domestic ABS units are still expected to see slight production cuts, with daily operating rates undoubtedly falling below 60%. However, the ABS market shows no immediate signs of shortage in the short term. On one hand, there are still outstanding orders from earlier periods yet to be delivered, and some low-priced inventory has not been fully absorbed. On the other hand, petrochemical producers currently maintain high inventory levels. Moreover, downstream buyers continue to resist high prices and will need more time to accept higher-priced material. Nevertheless, as ABS production cuts take effect—reducing supply—and downstream consumers gradually digest existing inventory and incrementally increase purchases of higher-priced material, a tight supply situation for certain ABS grades could emerge around mid-April.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

Breakthrough! 13.6-million-ton new giant emerges as world’s fourth-largest polyolefin producer, reshaping industry landscape

-

Domestic PBE Breakthrough, Polyolefin Modification Industry to Break the Impasse

-

BASF Delivers First Batch of Innovative Cathode Materials for Semi-Solid-State Batteries to Weilan New Energy

-

Auto Market Sees Significant Recovery in March: BYD No Longer Dominant, Changan Chery Geely Strive to Catch Up

-

Deadly Impact: Hormuz Strait Blockade Sparks Shortage of Plastic Raw Materials, Threatening Shutdowns at Japanese and Korean Chemical Plants