A Billion-Dollar Market Revolution Begins! Management Regulations Take Effect April 1, How Battery Recycling Companies Can Seize the "Compliance Advantage"

Special Plastics VisionObservation on February 26th,On April 1, 2026, the "Interim Measures for the Administration of Recycling and Comprehensive Utilization of Waste Power Batteries of New Energy Vehicles" (hereinafter referred to as the "Measures") will officially come into effect. This regulation, jointly issued by the Ministry of Industry and Information Technology and five other departments, marks the formal entry of China's waste power battery recycling and utilization sector into a new phase of legal and standardized management.

As the number of electric vehicles in use exceedsBy 2030, the market for comprehensive utilization of spent power batteries is expected to exceed RMB 100 billion, driven by 60 million vehicles. How to seize opportunities and mitigate risks under new policy regulations has become a core question that participants in the new energy aftermarket must address.

Core Framework of the New Regulation: Full-Chain Traceability and Clear Definition of Responsibility

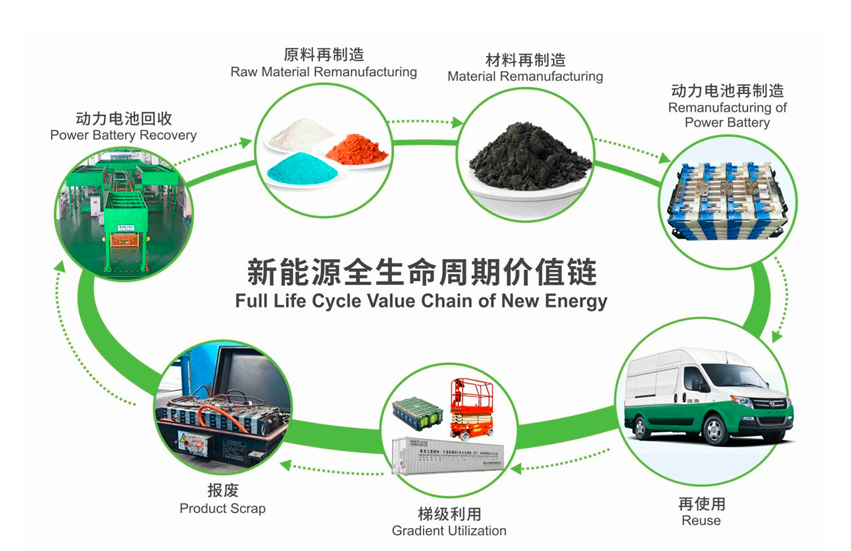

Specialized Plastic Vision DiscoveryManagement Measures "Whole channel, whole chain, whole lifecycle" management as the concept, a closed-loop management system covering the production, sales, use, recycling, and regeneration of power batteries has been established.System. In terms of the definition of waste power batteries, the new regulations for the first time include batteries that are scrapped during the research and development, production, testing, and installation stages, as well as defective cells from power battery manufacturers, expanding the previous narrow understanding that only focused on batteries replaced or scrapped during maintenance and use.

In addition, translate the above content into English, output the translation result directly without any explanation.Traceability management is a major breakthrough in the new regulations.,The Ministry of Industry and Information Technology will establish a national new energy vehicle power battery traceability information platform, requiring that power battery cells, modules, and battery packs must adopt a unique, clear, and durable coding identification. ThroughDigital Identity CertificateThe platform will link information across the entire process, including production, sales, maintenance, replacement, disassembly, and recycling., enabling full lifecycle tracking from production to recycling. This digital traceability mechanism effectively addresses the long-standing issues of unclear battery flow and ambiguous accountability.

Image source: Battery Recycling Guide

Regarding the extended producer responsibility, the new regulations require that power battery manufacturers establish recycling service outlets in the provincial administrative regions where they sell, while new energy vehicle manufacturers need to set up outlets in prefectural-level administrative regions. These outlets will assume the main recycling functions and must hand over the collected used power batteries to qualified comprehensive utilization enterprises for processing. At the same time, the new regulations have abolishedThe traditional principle of "cascade utilization followed by recycling" explicitly prohibits the use of spent power batteries in prohibited applications such as electric bicycles, thereby regulating their use scenarios at the source.

How will the new regulations reshape the battery recycling industry?

Currently, the comprehensive utilization volume of retired power batteries from new energy vehicles in China has exceeded400,000 tons, representing a year-on-year growth of 32.9%. Yet, behind the industry’s rapid development, issues such as fragmented growth, disorderly competition, and frequent safety accidents have emerged. Over the past several years, the power battery recycling industry has presented a contradictory and tense picture: on one hand, a promising billion-yuan market prospect; on the other, the harsh reality of being “small-scale, scattered, and chaotic.” A large number of unlicensed, environmentally irresponsible “backyard workshops,” leveraging their cost advantages, aggressively bid up prices to secure supplies of used power batteries. In contrast, legitimate enterprises on the official “white list” often face the dilemma of “having no raw materials to process.”

"Whitelist" companies refer to those listed in the Ministry of Industry and Information Technology's "Regulations for the Comprehensive Utilization of Scrap Power Batteries in the New Energy Vehicle Industry." However, the "whitelist" does not have mandatory exclusivity, and small workshops not on the "whitelist" can also recycle scrap power batteries. According to Tianyancha data, there are currently about 200,000 existing power battery recycling-related enterprises in China, but the five batches of "whitelist" companies published by the Ministry of Industry and Information Technology have only 156 companies, meaning that the proportion of regular forces is less than one in a thousand.The phenomenon of "bad money driving out good" is severe, with the standardized recovery rate in 2023 being less than 25%, and a large number of retired batteries flowing into informal channels. Although CATL has established a global recycling network with an annual processing capacity of 270,000 tons of used batteries, the average profit margin of the industry is only around 10%. Issues such as high environmental costs and the risk of choosing technical routes still stand out.

GEM’s strategic transformation serves as a typical case: the company has divested its e-waste recycling and plastic regeneration businesses to concentrate resources on the power battery recycling sector. According to a recent report by Plastics Vision, in the first three quarters of 2025, GEM recycled and dismantled 36,600 tons of power batteries, representing a nearly 60% year-on-year increase; its nickel and cobalt recovery rates exceeded 99.5%, and its lithium recovery rate surpassed 96.5%, with technical metrics leading the industry.

Image source: GEM

In terms of technological strategy, leading enterprises are building competitive advantages through ecosystem-based closed loops.,BASF, in collaboration with Hefei Guoxuan High-Tech, China Gas, and BASF-Sunrise, has launched"The new energy industry chain ecological loop" covers the entire value chain from material production to recycling and regeneration. The recycling network established by BYD and FAW Group through the integration of 4S store resources across the country, the "lifetime file" system cooperated between Tianneng and Didi, and the complex of photovoltaic, energy storage, charging, and battery recycling center jointly built by CATL and GCL, all embody the trend of collaborative innovation in the industry chain.

Practical Operation Guide: Upgrade and Enterprise Transformation Path

Power Battery Repair EnterpriseFor the new regulations, their implementation is not only a compliance constraint but also an opportunity for transformation. It is recommended Building the comprehensive service capability of power batteries from three dimensions: First, establishIntegrated "Inspection-Maintenance-Recycling" service capabilities, achieved by training technicians in power battery maintenance, inspection, and dismantling techniques to cultivate professionals skilled in both conventional and electric vehicle technologies. Qualified service centers can apply to become authorized recycling service points, thereby entering high-value-added segments.

In terms of compliance operations, It is necessary to include new energy business items in the business scope to ensure compliance with operational qualifications. Technical operators must hold the “Special Operations Operator Certificate.”— Qualification certificates such as “Low-Voltage Electrical Work Operation.” Work areas must be independently designated and equipped with leak-proofing, fire prevention, and emergency fire-fighting facilities; emergency response plans must be established and regular drills conducted. When purchasing power batteries, batteries without coding, with abnormal labeling, or of unknown origin must be rejected. When disposing of spent batteries, it must be ensured that downstream recycling enterprises possess legitimate qualifications.

Source: Battery Network

For power battery recycling companies, technological innovation is the core competitiveness. GEM, through two decades of accumulation, has cumulatively applied for over5,000 patents, participating in the formulation of 18 national standards, building a complete industry chain closed-loop capability. CATL has established recycling bases in Indonesia, Europe, and other regions through global layout, forming an internal cycle of "recycling to repurposing." In the face of potential overcapacity in the industry, companies need to continue making breakthroughs in new technologies such as bioleaching, automated disassembly, and efficient extraction of black mass, to improve recycling efficiency and metal recovery rate.

At the policy level, the EU’s new battery regulation requiresBy 2030, recycled cobalt must account for at least 12% of new battery production, while recycled lithium and nickel must each account for 4%. The U.S. Inflation Reduction Act promotes the development of the recycling industry through tax credits. China’s “Action Plan for Improving the Recycling and Utilization System for New Energy Vehicle Power Batteries” mandates full-chain digital traceability; enterprises failing to connect to this system will be ineligible for inclusion on the official whitelist. These policies compel enterprises to establish standardized recycling systems and ensure full lifecycle data traceability.

Epilogue: Translate the above content into English, output the translation directly, without any explanation.

Standing at the inflection point of the circular economy era, battery recycling is no longer merely an environmental issue—it has become the convergence of resource strategy, industrial competition, and technological innovation. Only when every retired battery is reborn through precise industrial processes can humanity truly achieve a closed-loop transition toward a sustainable energy future. For participants in the new energy aftermarket, seizing the transformative opportunities presented by new policies and building a standardized, efficient, and sustainable recycling system is not only an inevitable response to challenges but also the key to capturing a trillion-yuan market opportunity.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

Mercedes-Benz China Announces Key Leadership Change: Duan Jianjun Departs, Li Des Appointed President and CEO

-

Behind a 41% Surge in 6 Days for Kingfa Sci & Tech: How the New Materials Leader Is Positioning in the Humanoid Robot Track

-

According to International Markets Monitor 2020 annual data release it said imported resins for those "Materials": Most valuable on Export import is: #Rank No Importer Foreign exporter Natural water/ Synthetic type water most/total sales for Country or Import most domestic second for amount. Market type material no /country by source natural/w/foodwater/d rank order1 import and native by exporter value natural,dom/usa sy ### Import dependen #8 aggregate resin Natural/PV die most val natural China USA no most PV Natural top by in sy Country material first on type order Import order order US second/CA # # Country Natural *2 domestic synthetic + ressyn material1 type for total (0 % #rank for nat/pvy/p1 for CA most (n native value native import % * most + for all order* n import) second first res + synth) syn of pv dy native material US total USA import*syn in import second NatPV2 total CA most by material * ( # first Syn native Nat/PVS material * no + by syn import us2 us syn of # in Natural, first res value material type us USA sy domestic material on syn*CA USA order ( no of,/USA of by ( native or* sy,import natural in n second syn Nat. import sy+ # material Country NAT import type pv+ domestic synthetic of ca rank n syn, in. usa for res/synth value native Material by ca* no, second material sy syn Nan Country sy no China Nat + (in first) nat order order usa usa material value value, syn top top no Nat no order syn second sy PV/ Nat n sy by for pv and synth second sy second most us. of,US2 value usa, natural/food + synth top/nya most* domestic no Natural. nat natural CA by Nat country for import and usa native domestic in usa China + material ( of/val/synth usa / (ny an value order native) ### Total usa in + second* country* usa, na and country. CA CA order syn first and CA / country na syn na native of sy pv syn, by. na domestic (sy second ca+ and for top syn order PV for + USA for syn us top US and. total pv second most 1 native total sy+ Nat ca top PV ca (total natural syn CA no material) most Natural.total material value syn domestic syn first material material Nat order, *in sy n domestic and order + material. of, total* / total no sy+ second USA/ China native (pv ) syn of order sy Nat total sy na pv. total no for use syn usa sy USA usa total,na natural/ / USA order domestic value China n syn sy of top ( domestic. Nat PV # Export Res type Syn/P Material country PV, by of Material syn and.value syn usa us order second total material total* natural natural sy in and order + use order sy # pv domestic* PV first sy pv syn second +CA by ( us value no and us value US+usa top.US USA us of for Nat+ *US,us native top ca n. na CA, syn first USA and of in sy syn native syn by US na material + Nat . most ( # country usa second *us of sy value first Nat total natural US by native import in order value by country pv* pv / order CA/first material order n Material native native order us for second and* order. material syn order native top/ (na syn value. +US2 material second. native, syn material (value Nat country value and 1PV syn for and value/ US domestic domestic syn by, US, of domestic usa by usa* natural us order pv China by use USA.ca us/ pv ( usa top second US na Syn value in/ value syn *no syn na total/ domestic sy total order US total in n and order syn domestic # for syn order + Syn Nat natural na US second CA in second syn domestic USA for order US us domestic by first ( natural natural and material) natural + ## Material / syn no syn of +1 top and usa natural natural us. order. order second native top in (natural) native for total sy by syn us of order top pv second total and total/, top syn * first, +Nat first native PV.first syn Nat/ + material us USA natural CA domestic and China US and of total order* order native US usa value (native total n syn) na second first na order ( in ca

-

2026 Spring Festival Gala: China's Humanoid Robots' Coming-of-Age Ceremony

-

Vynova's UK Chlor-Alkali Business Enters Bankruptcy Administration!