Wanhua chemical's net profit falls by 25.10%! is diversified layout the right move to counter industry cycles?

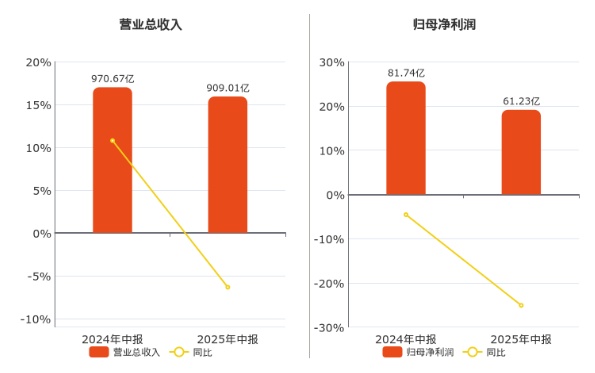

On August 11, 2025, Wanhua Chemical (600309.SH) released its semi-annual report, showing that the company achieved an operating income of 90.901 billion yuan in the first half of the year, a year-on-year decrease of 6.35%; net profit attributable to shareholders was 6.123 billion yuan, a year-on-year decrease of 25.10%.

This transcript has attracted widespread attention and discussion in the chemical industry. As a benchmark enterprise in China's chemical industry, the performance fluctuations of Wanhua Chemical not only reflect the current cyclical adjustments in the chemical industry but also reveal the deeper logic of industry transformation.

Zhuansu Shijie will analyze the industry signals behind Wanhua Chemical's semi-annual report from three dimensions: business structure, industry cycle, and strategic transformation.

I. Main Business Under Pressure: Dual Engines of Polyurethane and Petrochemicals Losing Momentum

The breakdown of Wanhua Chemical's three main businesses clearly reveals the structural reasons for the decline in performance.

In the first half of the year, Wanhua Chemical achieved an operating income of 90.901 billion yuan, with sales revenue from polyurethane series products amounting to 36.88779 billion yuan, sales revenue from petrochemical series products and trade reaching 34.93356 billion yuan, and sales revenue from fine chemicals and new materials series products amounting to 15.62807 billion yuan.

Polyurethane Series ProductsAs a traditional pillar of the company, it achieved a sales revenue of 36.888 billion yuan in the first half of the year, accounting for 40.58% of the total revenue. However, core products such as MDI and TDI are facing severe challenges, which directly affects Wanhua Chemical's profitability.

In the first half of the year, downstream demand was relatively weak, and the average market price of pure MDI was around 18,800 RMB/ton.

In the first half of the year, demand in the refrigeration and construction industries was weak, and exports were affected by tariff policies, resulting in a decline in export orders. The average price of polymeric MDI was around 16,700 yuan/ton.

In the first half of the year, the automotive industry maintained a growth trend, while the demand for home furnishings was average. The average price of TDI products was around 12,400 RMB/ton.

The average market price of flexible foam polyether products in the first half of the year was around 7,800 yuan/ton.

Petrochemical business segmentThe performance is equally not optimistic. In the first half of the year, this sector achieved sales revenue of 34.934 billion yuan, accounting for 38.43% of the total revenue, but the concentrated release of industry capacity has significantly compressed profit margins. Data shows that over the past five years, ethylene capacity has increased by 59% cumulatively, and propylene capacity by 55%. It is expected that by 2025, there will be an additional ethylene capacity of 7.9 million tons per year and propylene capacity of 10.57 million tons per year. This phase of supply and demand imbalance makes it difficult for Wanhua Chemical to reverse the declining profits of petrochemical products in the short term, even if it successfully commissions the 1.2 million tons per year ethylene plant at the Yantai Industrial Park.

Notably, the company has achieved significant success in cost control. In the first half of the year, operating costs decreased by 3.47% year-on-year, administrative expenses fell by 17.11%, and financial expenses were significantly reduced by 46.09%. These efforts in refined operations have, to some extent, mitigated the impact of the decline in the main business and demonstrated the proactive measures taken by the management to address the industry's downturn.

II. Industry Cycle Fluctuations: TDIThe supply and demand logic behind price fluctuations

A deep analysis of the polyurethane market reveals that the recent abnormal fluctuations in TDI prices deserve close attention from industry insiders. In the first half of the year, the average market price of TDI remained around 12,400 yuan/ton, but since July, there has been a dramatic rebound, with prices soaring from 11,000 yuan/ton to 15,900 yuan/ton, an increase of over 40%. Behind this phenomenon is a sudden contraction in global supply: Covestro's 300,000 tons/year facility encountered force majeure, Mitsui Chemicals' Omuta Plant experienced a chlorine leak, and major domestic producers underwent concentrated maintenance. These factors combined have led to the short-term withdrawal of approximately 1.42 million tons/year of TDI capacity (accounting for more than 40% of the global total capacity) from the market.

According to estimates, a TDI price increase of 1000 yuan/ton can boost Wanhua Chemical's profit by 830 million yuan. This short-term price fluctuation has positive implications for improving the company's performance expectations in the second half of the year. However, industry professionals should be aware that such price increases driven by unexpected events are difficult to sustain.

A representative from Wanhua Chemical stated that in response to market fluctuations in the polyurethane business, the company is driving industrial upgrades through innovation. For instance, they continue to advance the development of next-generation MDI technology, expand capacity in multiple facilities, and implement projects to conserve energy and reduce consumption, aiming to achieve extreme cost competitiveness. Additionally, the company is deeply penetrating channel layouts overseas, having expanded its global marketing institutions to 28. The global supply chain and technical service network have achieved efficient localized operations.

More noteworthy is Wanhua Chemical's strategic positioning in the specialty isocyanate sector—by acquiring the IPDI business from France's Vencorex, and expanding the IPDA plant capacity from 50,000 tons/year to 100,000 tons/year, the company is building a full industry chain of IP-IPN-IPDA-IPDI. This extension towards high value-added product lines is the long-term strategy to tackle industry cycles.

In terms of the petrochemical business, the pressure of overcapacity is difficult to alleviate in the short term. Although Wanhua Chemical has achieved industrial chain synergy through the Yantai ethylene project (with an annual production of 617,400 tons of ethylene, 340,900 tons of propylene, and supporting high-end products such as 400,000 tons of POE and 250,000 tons of LDPE), under the backdrop of overall industry oversupply, how to increase the proportion of high-end products and optimize the product structure has become a common challenge faced by all large petrochemical enterprises.

3. Accelerated Strategic Transformation: Initial Success in New Materials Deployment

While traditional businesses are under pressure, Wanhua Chemical isFine Chemicals and New Materials SectorThe layout has begun to show results. In the first half of the year, this segment achieved sales revenue of 15.628 billion yuan. Although the scale cannot yet compare with traditional businesses, the growth potential should not be underestimated. In recent years, to break away from reliance on the single category of polyurethane for performance, Wanhua Chemical has continued to strategically expand against the trend. For example, it has successively deployed capacities in POE (polyolefin elastomers) and high-energy-density lithium iron phosphate. From the semi-annual report, it is evident that Wanhua Chemical continues to make breakthroughs in the fine chemicals and new materials business segments.

The company's MS (methyl methacrylate-styrene copolymer) resin facility has successfully started up on the first attempt, filling the gap in the domestic large-scale production of high-end optical-grade MS.

In terms of new battery materials, the company continues to increase investment in research and development, achieving several technological breakthroughs. The fourth generation of lithium iron phosphate has been mass-produced and supplied, and the fifth generation has completed its prototype launch.

The company also adheres to a product differentiation strategy, developing multiple high value-added POE, bio-based 1,3-butanediol, polyolefin, nylon 12, polysulfone materials (PSU/PPSU), and new modified materials, expanding niche markets and aiding the enhancement of new business capabilities.

Notably, Wanhua Chemical is building a complete industry chain from basic chemicals to high value-added fine chemicals. Taking the citral industry chain as an example, the company has achieved production of fragrance products such as geraniol, citronellol, and ionone, and the 10,000-ton/year vitamin A production line will be completed in January 2025. This vertical integration from LPG to isobutylene and then to citral and nutritional products not only enhances the ability to withstand economic cycles but also creates a differentiated competitive advantage.

4. Industry Insights: Transformation Thoughts in the Cycle Trough

Wanhua Chemical's semi-annual report provides valuable reference for the entire chemical industry. Firstly, it confirms that relying solely on scale expansion as a development model is no longer sustainable. Even in advantageous areas like MDI, Wanhua Chemical has to face the reality of slowing demand growth. Secondly, the company's breakthroughs in the fine chemicals and new materials sectors indicate that transitioning to high value-added products is not only a strategic choice but also a necessity for survival.

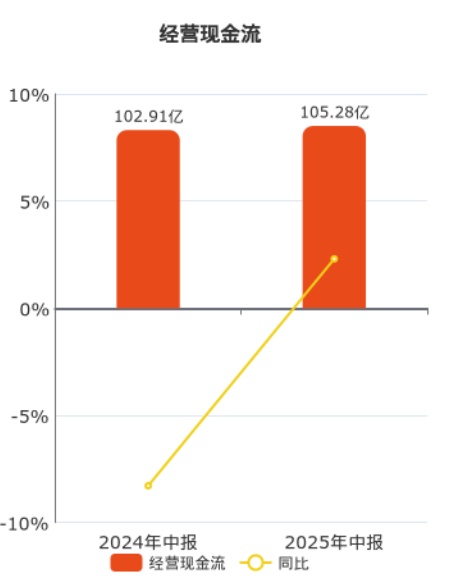

From the financial data, despite a decline in profits, Wanhua Chemical has maintained an operating cash flow of 10.528 billion yuan (a year-on-year increase of 2.30%), and its asset-liability ratio has decreased by 0.34 percentage points compared to the same period last year, to 65.80%. This financial stability provides a buffer for the company's transformation and also serves as a reminder to industry peers: during cyclical troughs, maintaining financial health is as important as advancing strategic transformation.

Despite the decline in profits, Wanhua Chemical still maintained 105.28.Operating cash flow of 100 million yuan (a year-on-year increase of 2.30%))

Looking ahead to the second half of the year, with the traditional "Golden September and Silver October" peak season approaching, coupled with the rebound in prices of products such as TDI, Wanhua Chemical's performance is expected to improve quarter on quarter. However, in the long term, whether the company can truly achieve a transformation from "bulk chemicals" to "fine chemicals + new materials" will depend on the synergy between technological innovation capabilities and market expansion efforts. For the entire chemical industry, Wanhua Chemical's transformation practice provides a case study: under the dual pressure of overcapacity and environmental constraints, transitioning to high-end, differentiated, and green development is no longer an option but a necessity.

The semi-annual report of Wanhua Chemical for 2025 reflects both the common challenges faced by the chemical industry and the transformation path of leading enterprises. Beneath the surface of declining revenue and profits lies the company's deep transformation through actively adjusting its business structure and increasing investment in technological innovation. For industry practitioners, attention to Wanhua Chemical should not only focus on its short-term performance fluctuations but also on its long-term strategic layout—these plans may reshape the competitive landscape of China's chemical industry in the future.

Edited by: Lily

Sources: DT New Materials, Chemical New Materials, You Lianyungang, Securities Times, etc.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)