[PVC Monthly Review] Supply and Demand Weakness Dominates, April PVC Prices Fall from Highs

Monthly Market Analysis

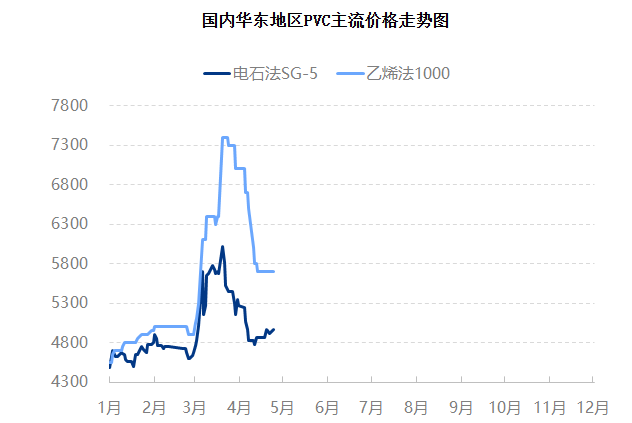

In April, China's domestic PVC market continued its weak downward trend. The earlier sentiment-driven price rally faded, and prices steadily declined from their highs as market dynamics shifted from strength to weakness, entering a phase dominated by weak fundamentals. At the beginning of the month, prices remained relatively high, supported by previous optimistic expectations. However, downstream demand failed to keep pace, leading to persistently weak actual transactions. From mid-month onward, both futures and spot prices weakened in tandem, prompting a more cautious market sentiment and prompting sellers to proactively lower their quotations. Compounded by declining costs that offered little support, price declines further accelerated.

From a specific price perspective, taking Changzhou SG-5 as an example, as of April 27, the mainstream price for Changzhou SG-5 was reported at RMB 4,970 per ton, down RMB 180 per ton from RMB 5,150 per ton at the beginning of the month, representing a decline of 3.50%.

II. Key Focus Areas for the Next Period

PVC spring plant maintenance intensity and downstream enterprises' order fulfillment situation;

Fluctuations in upstream raw material prices and supply changes

International crude oil supply stability and circulation smoothness.

III. Next Month Market Forecast

PVC industry maintenance activities are expected to expand in May, leading to supply contraction that coincides with a modest demand recovery. This convergence will strengthen expectations for inventory drawdowns, gradually alleviating the high social inventory levels and reducing inventory pressure, thereby providing significant support for price recovery. However, the overall lackluster growth in both domestic and export demand remains unchanged, limiting PVC's upside potential.

Overall, the price center of PVC in May may slightly shift upwards compared to April, but the overall increase will be limited. Subsequent attention should be paid to the progress of maintenance in May, changes in downstream operations, and the production status of ethylene-based PVC companies. The current social inventory of over 1.35 million tons remains the biggest restraining factor in the market. It is expected that the price center of PVC in May will be 5,050 yuan/ton, an increase of 74 yuan/ton month-on-month, with a growth rate of 1.49%.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Continental Plans to Begin Sale of ContiTech in Early 2026

-

BASF Delivers First Batch of Innovative Cathode Materials for Semi-Solid-State Batteries to Weilan New Energy

-

First Time Surpassing $3 Billion! First Time Surpassing 100,000 Tons! Cathay Biotech’s 2025 Performance: Chemical Production Fully Phased Out, Biological Method Wins

-

Recycled PE/PP Morning Outlook: Market Expected to Remain Weak Within Range

-

Completion And Commissioning! Evonik’s Four Major Projects Officially Launched