PS Monthly Review: High Raw Material Prices and Inventory Draw Support April PS Market’s High-Range Volatility

I. PS Market Review for This Month

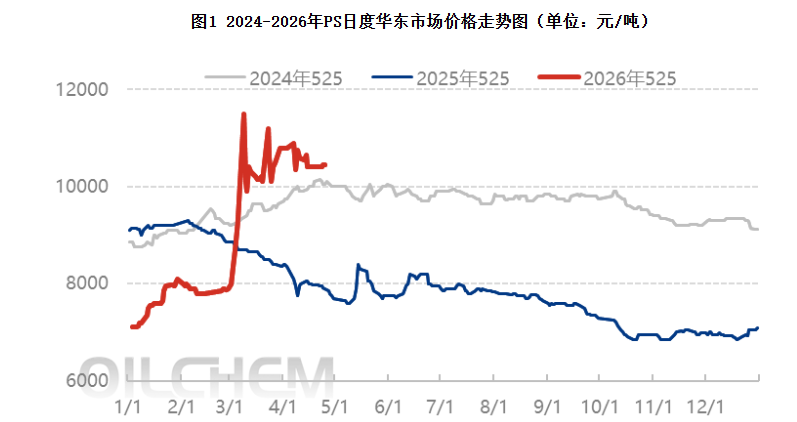

In April, the domestic PS market showed a high-level fluctuation, with the average price of the 525 grade in East China reaching 10,553 yuan/ton at the end of the month, up 5% month-on-month. The market trend was mainly supported by high raw material prices and a rapid decline in industry inventories. On the cost side, crude oil and benzene prices remained in a high-level fluctuation, while the supply and demand for styrene were tight, jointly pushing the cost base of PS to a high level. On the supply and demand side, high costs and negative production profits led to unplanned supply reductions in the PS industry, with production capacity utilization dropping to around 47%. The supply contraction kept finished product inventories at low levels, but inventories slightly rebounded in the latter part of the month due to a decline in market transaction enthusiasm.

II. Key Data Trends

In terms of production, China's PS output in April is expected to be 343,000 tons, a decrease of 31,000 tons from the previous month, a reduction of 9.04%, and a year-on-year decrease of 12.9%; the cumulative output from January to April is 1.472 million tons, a year-on-year decrease of 7.2%.

In terms of inventory, the average domestic PS finished goods inventory in April was 78,000 tons, down 4,000 tons from the previous month, a decrease of 4.9%.

III. Outlook for the Future

It is expected that the PS market price will remain at a high level in May. On the cost side, the continuous destocking expectation of pure benzene provides strong support for styrene, and styrene itself also has a destocking expectation, but the downstream has a production reduction plan, and high costs and weak demand form a game, making it difficult for the price to form a one-sided trend. In terms of supply and demand, Henan Network Plastic has a new plant commissioning plan in May, and the specific progress still needs to be observed; the current industry is in a loss state, and some PS plants still have production reduction expectations, but the overall inventory level of the industry is not high, and the space for further production reduction is limited. Overall, the supply and demand pressure in the PS market in May is not great, and prices are likely to fluctuate at high levels following the raw material prices.

【Copyright and Disclaimer】This article is the property of PlastMatch. For business cooperation, media interviews, article reprints, or suggestions, please call the PlastMatch customer service hotline at +86-18030158354 or via email at service@zhuansushijie.com. The information and data provided by PlastMatch are for reference only and do not constitute direct advice for client decision-making. Any decisions made by clients based on such information and data, and all resulting direct or indirect losses and legal consequences, shall be borne by the clients themselves and are unrelated to PlastMatch. Unauthorized reprinting is strictly prohibited.

Most Popular

-

Continental Plans to Begin Sale of ContiTech in Early 2026

-

BASF Delivers First Batch of Innovative Cathode Materials for Semi-Solid-State Batteries to Weilan New Energy

-

First Time Surpassing $3 Billion! First Time Surpassing 100,000 Tons! Cathay Biotech’s 2025 Performance: Chemical Production Fully Phased Out, Biological Method Wins

-

Recycled PE/PP Morning Outlook: Market Expected to Remain Weak Within Range

-

Completion And Commissioning! Evonik’s Four Major Projects Officially Launched