Polypropylene: Why the Peak Season Hasn't Arrived and When the Price Turning Point Will Come

As we enter 2025, the domestic PP market has been on a downward trend, and by August, the market did not experience the anticipated rebound, instead declining further. With the "Golden September" approaching, the question remains whether market demand will improve and when the market turning point will arrive.

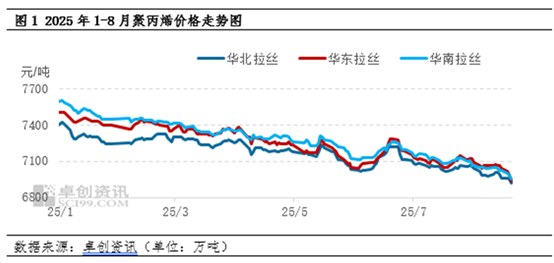

The price continues to decline, reaching a new low for the year.

In 2025, the domestic PP market showed a one-sided trend, with the focus continuously shifting downward. Especially by August, the market still lacked support, and the focus dropped further. According to data from Zhuocang Information, taking East China PP raffia as an example, the average price in August was 7,035 yuan/ton, down 0.92% month-on-month, marking a new low for the year. Analysis indicates that although there was some macroeconomic news support released near the end of August, the supply and demand fundamentals remained weak. In particular, downstream new orders showed no improvement, coupled with slow destocking of finished product inventories, which hindered downstream purchasing enthusiasm. This increased the resistance to market rallies, causing the focus to decline once again.

Supply-side pressure intensifies again

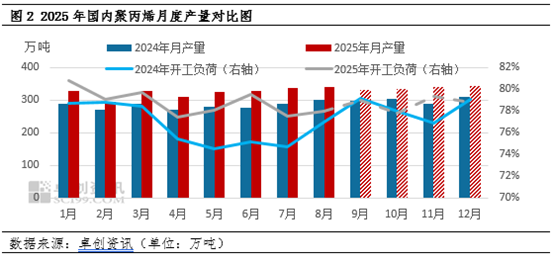

The supply side is expected to increase in the later period, adding upward pressure to the market. On one hand, new production capacity is about to be commissioned. According to data from SCI99, the 450,000-ton Line 2 of the second phase of Ningbo Daxie has already produced qualified products, while the 450,000-ton Line 1 of the same phase is planned to be launched in mid-September. In addition, the 400,000-ton Phase II unit of Guangxi Petrochemical is scheduled to release capacity in mid-October. The anticipated addition of new capacity is expected to have a strong impact on the market in the future.

In terms of equipment maintenance, PP maintenance was concentrated in the first half of the year, but currently, the intensity of maintenance on existing equipment has somewhat weakened, and there is a decreasing trend in the number of newly planned maintenance units. Especially after most companies complete their major maintenance plans in the first half of the year, they tend to operate steadily in the second half, and as the winter weather turns colder, maintenance units decrease even further. Therefore, the overall maintenance intensity of equipment is expected to weaken in the future. Overall, considering the impact of new capacity additions and the anticipated weakening of maintenance intensity, supply is expected to be relatively abundant, exerting downward pressure on prices.

Differences have emerged between domestic demand and external demand.

Domestic demand is expected to improve in the later period, providing support for market expectations in September and October. Holidays and the back-to-school season are anticipated to drive increased demand for PP daily necessities and packaging. Additionally, holiday promotions for home appliances will further boost PP demand. Moreover, due to the earlier impact of high temperatures, downstream operating rates declined; as the high-temperature weather gradually subsides, there is an expectation for increased downstream operations.

From the perspective of external demand, the expected improvement is likely to be limited. On one hand, overall overseas demand remains uncertain. On the other hand, due to fluctuations in Sino-US tariffs in the first half of the year, some domestic export-oriented enterprises have adjusted their export directions, resulting in a reduction in export volumes. In addition, the practice of "front-loading" exports has already consumed part of the demand in the first half of the year, so exports of finished products are expected to decline year-on-year. However, overall, domestic demand is expected to increase to some extent, providing strong support to the market.

Overall, the market is still expected to stop falling and rebound in September, with the market focus likely to rise. Although supply is expected to increase, domestic demand is anticipated to improve, which may strengthen the market’s fundamental support. At the same time, on the macro front, further announcements regarding the renovation of old domestic facilities may be released, and there is a strong expectation of a Federal Reserve rate cut in September. Both factors are likely to boost the PP market to some extent. However, considering the pressure from ample supply and the fact that consumer spending remains cautious, these may pose resistance to market growth. As a result, the market is expected to rise moderately.

【Copyright and Disclaimer】The above information is collected and organized by PlastMatch. The copyright belongs to the original author. This article is reprinted for the purpose of providing more information, and it does not imply that PlastMatch endorses the views expressed in the article or guarantees its accuracy. If there are any errors in the source attribution or if your legitimate rights have been infringed, please contact us, and we will promptly correct or remove the content. If other media, websites, or individuals use the aforementioned content, they must clearly indicate the original source and origin of the work and assume legal responsibility on their own.

Most Popular

-

AI Computing Power Demand Ignites Electronic Fabrics! China Jushi Hits Limit Up! Domestic Substitution Welcomes Golden Window

-

Focus on going global! kingfa sci. leads, huitong, preter, and kumho nire follow, china’s modified plastics frenziedly expanding worldwide

-

Back-to-back major joker moves! covestro’s 1.32 million ton mdi dual-line expansion and hdi acquisition reshape global polyurethane landscape

-

Evonik Parts Ways With The Polyester Business! A Strategic Retreat By A Germany Chemical Giant And The Global Industry Shift

-

PA66 Cost and Profit: Broad-Based Weakness in the Feedstock Market Continues to Erode Cost Support for PA66 (202606)